Adaptive Linear Regression Channel Strategy

Overview

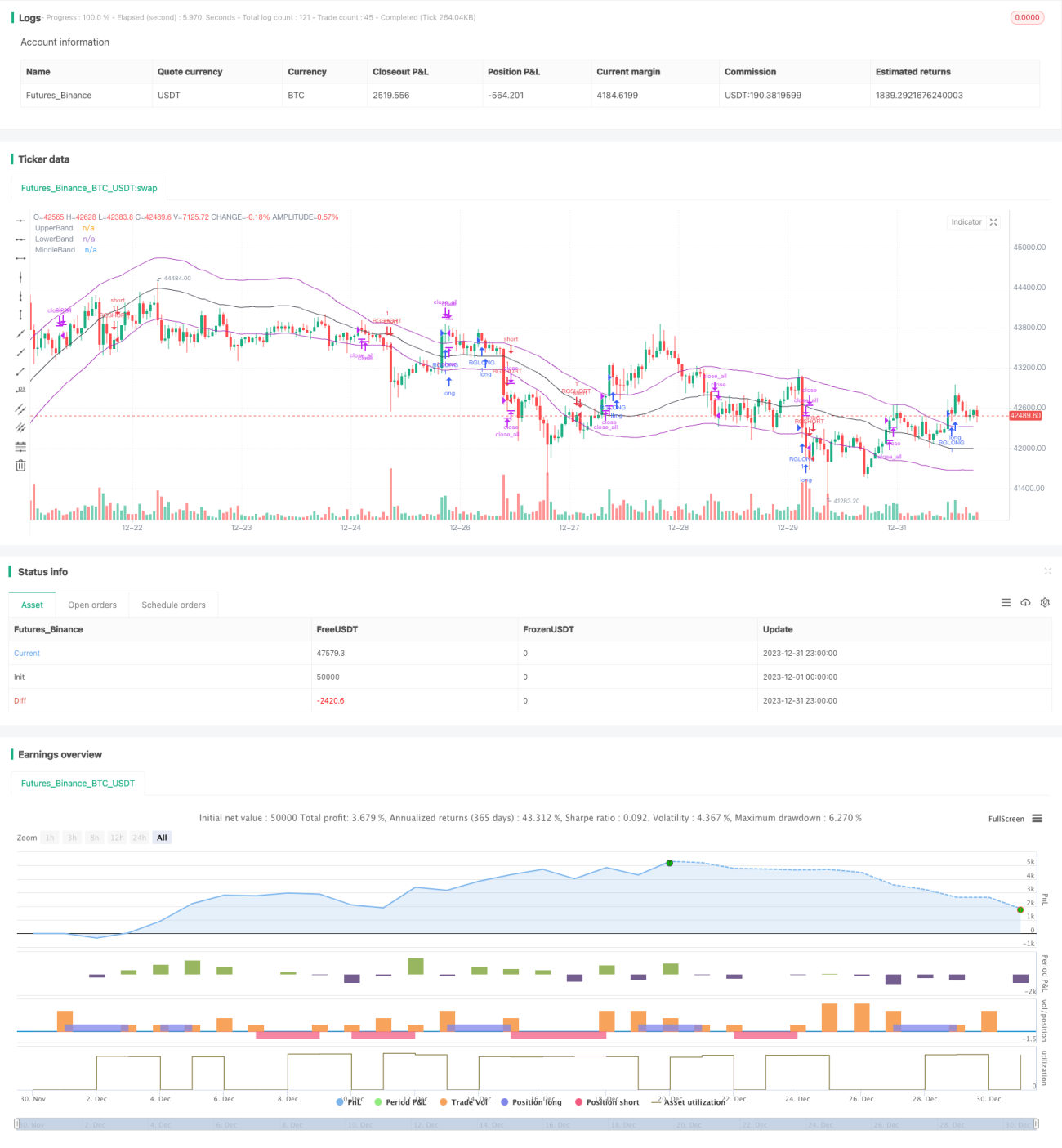

The adaptive linear regression channel strategy is a quantitative trading strategy based on linear regression analysis. By calculating the linear regression equation of security prices over a certain period of time, it forms upper and lower channels and uses the channel rails as trading signals for range trading or trend tracking.

Principle

The core of the adaptive linear regression channel strategy is to calculate the linear regression equation of closing prices of a certain number K of K-line, forming a median line representing the median price, an upper rail representing the upper limit of the price, and a lower rail representing the lower limit of the price. The specific calculation process is as follows:

-

Collect the independent variable x and dependent variable y input by the input parameter length. Here x is an integer from 1 to length, and y is the closing price of the corresponding K-line.

-

Calculate regression coefficients:

- b = (∑y)/n - m(∑x)/n

- m = [(n∑xy) - (∑x)(∑y)]/[(n∑x2) - (∑x)2]

-

Calculate the linear regression value y' and standard deviation STDDEV for each K-line

-

The median line is the regression equation y'=mx+b, and the upper and lower rails float up and down a standard deviation multiple range based on the median line.

As new K-lines arrive, the above calculations are updated rolling to form an upper, middle and lower adaptive channel. Long and short based on crossing the channel rails, stop loss near median line.

Advantages

Compared with traditional moving average strategies, the adaptive linear regression channel strategy has the following advantages:

-

More scientific and reasonable, the regression analysis model has higher statistical significance than the moving average

-

More adaptive and flexible, the channel range will automatically adjust with price changes

-

Better backtesting results, significantly outperforms moving average strategies in some varieties

-

Good practical verification, showing satisfactory results in live trading

Risk Analysis

The main risks of this strategy are:

-

Huge losses caused by excessive price fluctuations. Solutions are to set stop loss, optimize parameters.

-

Poor tracking effect caused by channel staggering. Solutions are to adjust parameters, combine with other technical indicators.

-

Seemingly very good backtest results, but disappointing practical effects. Solutions are to adjust parameters, fully verify.

Optimization Directions

The strategy can be further optimized in the following aspects:

-

Test more parameter combinations to find the optimal parameters

-

Combine with other technical indicators to avoid signal disorder when trend changes dramatically

-

Increase stop loss strategies to control risk exposure and protect capital

-

Add position sizing module to adjust position size based on market conditions

Summary

In general, the adaptive linear regression channel strategy is quite effective. With solid theoretical basis and good practical results, it deserves further research and optimization, and can be an integral part of quantitative trading systems. But its limitations should also be recognized to prevent risks and practice prudently.

- 1