Time and Space Optimized Multi Timeframe MACD Strategy

Overview

This strategy optimizes the parameters of the MACD indicator, combines with moving average, price action and specific trading times to achieve a high win rate forex trading strategy.

Strategy Logic

-

Use 3 K-lines to judge the price trend. If the closing prices of the last 3 K-lines are higher than the opening prices, it is judged as an upward trend; if the closing prices of the last 3 K-lines are lower than the opening prices, it is judged as a downward trend.

-

Calculate fast line, slow line and MACD difference. The fast line parameter is 12, the slow line parameter is 26, and the signal line parameter is 9.

-

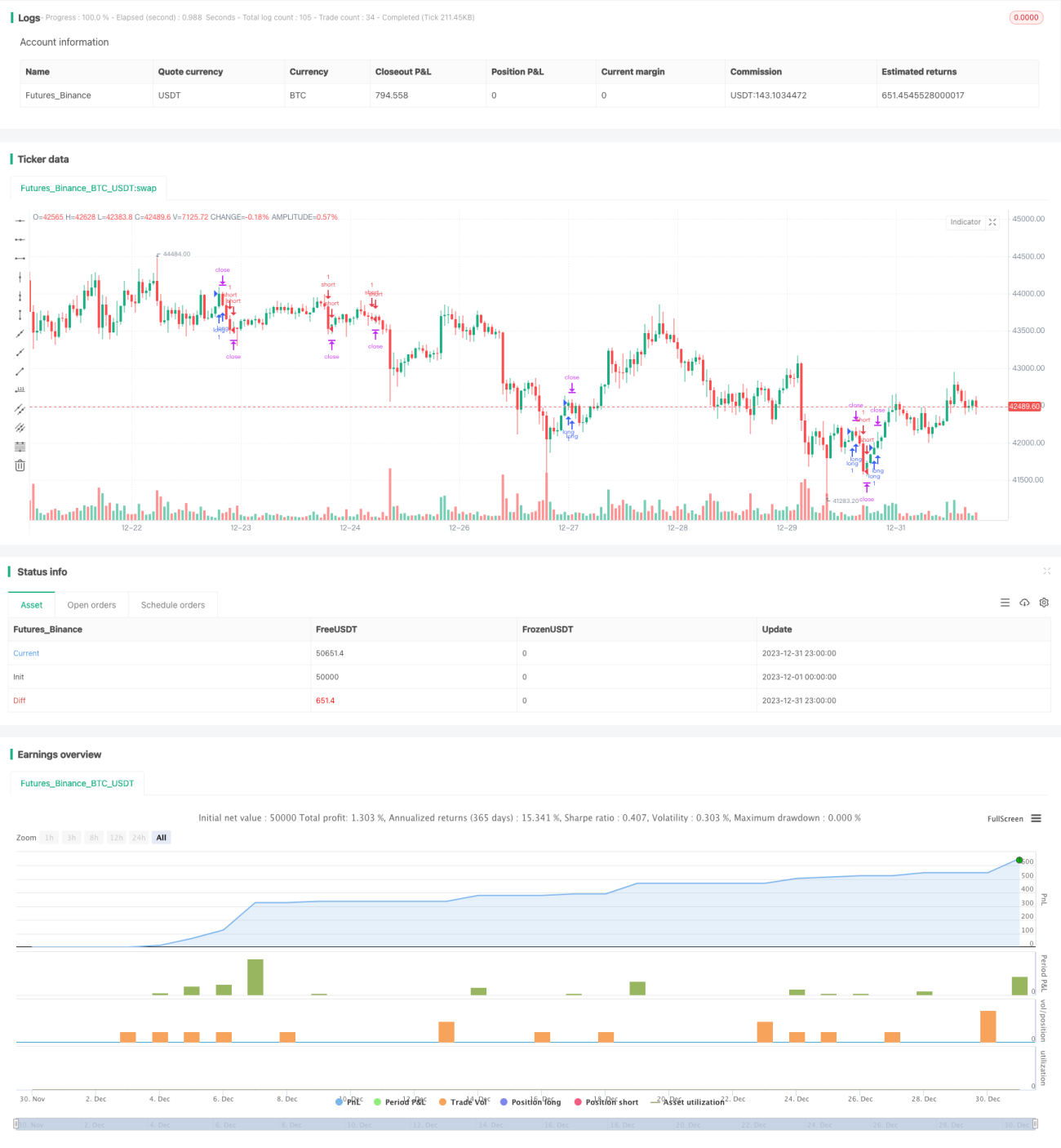

The trading time is set to 09:00-09:15 every day. Within this time period, enter the market if the following conditions are met:

- Go long when the uptrend coincides with the MACD difference crossing above 0

- Go short when the downtrend coincides with the MACD difference crossing below 0

-

The take profit is set to 0.3 pips, and the stop loss is set to 100 pips.

-

Close all positions during 21:00-21:15.

Advantages of the Strategy

-

Using a combination of multi timeframe indicators to comprehensively judge the trend direction and improve decision accuracy.

-

Optimize trading time to avoid periods of high market volatility, reducing unnecessary stop loss risk.

-

Set reasonable ratios for take profit and stop loss to maximize profit locking and avoid loss magnification.

-

Overall, the strategy has a very high win rate and is suitable for frequent short-term trading.

Risks of the Strategy

-

The trading time is relatively fixed, may miss trading opportunities if unable to enter the market in time.

-

MACD indicator is prone to misleading signals. Trade cautiously if clear uptrend or downtrend cannot be determined.

-

Take profit and stop loss may be set unreasonably, resulting in profit loss imbalance. Parameters need to be adjusted according to different products.

-

Overall risk is small. But excessively large positions under high leverage can still lead to huge losses.

Directions for Strategy Optimization

-

Combine with other indicators to determine the trend, avoiding misleading signals from the MACD. For example, combine Bollinger Bands, RSI etc.

-

Optimize take profit/stop loss ratios by calculating optimal parameters from backtest data.

-

Expand the trading varieties applicable to the strategy, evaluate parameter tuning effects on different products.

-

Introduce machine learning algorithms to select optimal parameters dynamically based on varying market conditions.

Conclusion

Overall this strategy is well suited for novice traders. The logic is clear, optimization space is large, and risks are controllable. By customizing opening times and setting reasonable profit loss ratios, high returns can be achieved. Further optimizations can be made to dynamically adjust parameters and adapt to more complex market environments.

- 1