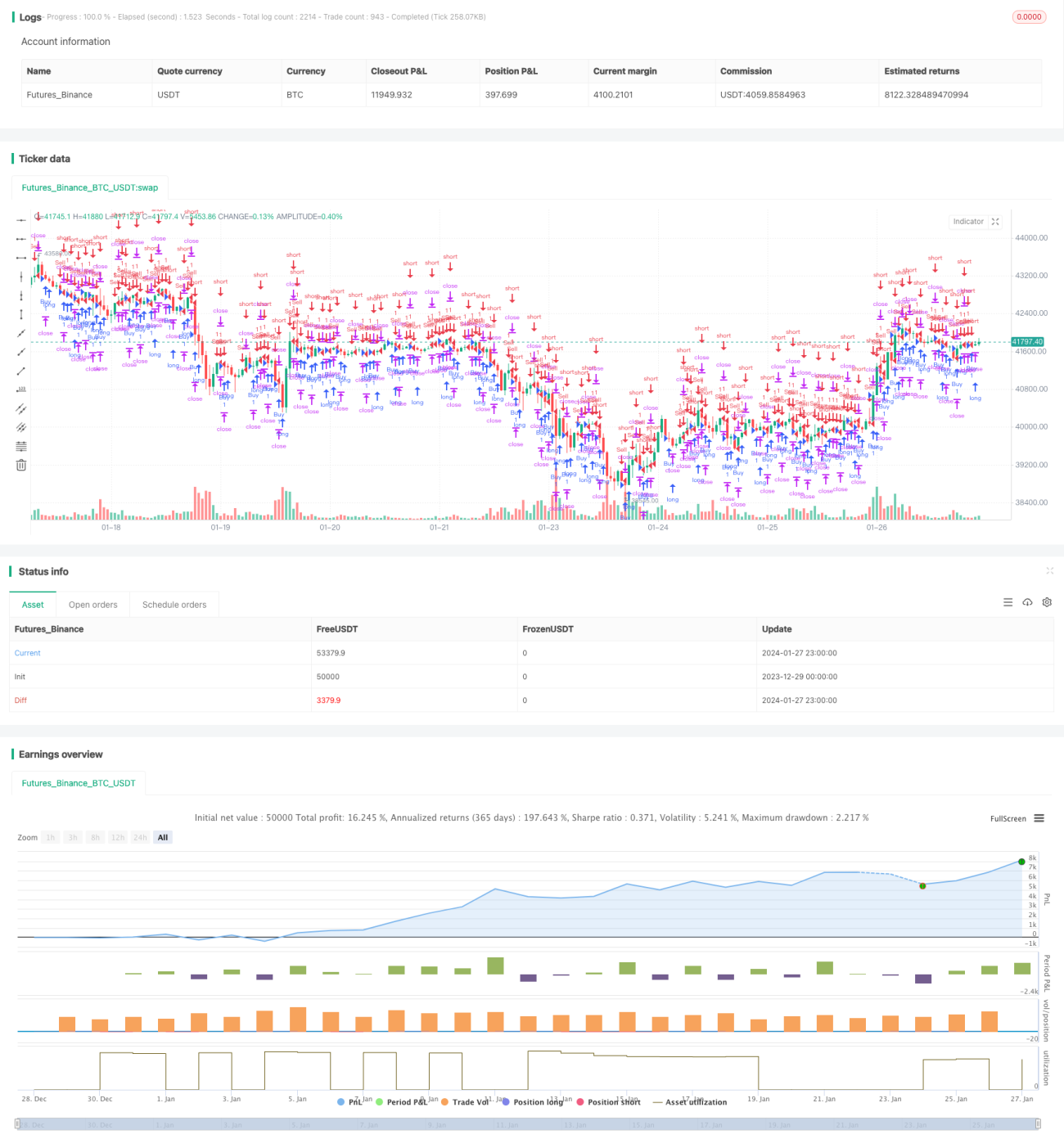

Fixed Time Breakback Testing Strategy

Overview

The main idea of this strategy is to judge whether the closing price of the 5-minute K-line after the market opens at a fixed time point (08:35 UTC+5 time zone here) is higher or lower than the opening price. If the closing price is higher than the opening price, go long. If the closing price is lower than the opening price, go short. And set profit targets for long and short positions.

Strategy Principle

The specific principle of this strategy is:

-

Set the desired trading time, which is 08:35 UTC+5 time zone here.

-

At this time point, judge whether the closing price of the current 5-minute K-line is higher than the opening price. If the closing price is higher than the opening price, it means that the 5-minute K-line closed with a yang line, go long.

-

If the closing price is lower than the opening price, it means the 5-minute K-line closed with a yin line, go short.

-

After going long, set the profit target to exit the long position at $1000. After going short, set the profit target to exit the short position at $500.

Advantage Analysis

The main advantages of this strategy are:

-

The strategy idea is simple and clear, easy to understand and implement.

-

The fixed trading time can avoid overnight risk.

-

Using 5-minute levels to judge trends accurately.

-

Setting profit targets can lock in profits.

Risk Analysis

There are also some risks to this strategy:

-

Fixed trading times may miss trading opportunities at other market times. Multiple trading times can be set.

-

5-minute judgments may not be accurate enough, judgments can be made in combination with multiple timeframes.

-

The fluctuation between closing price and opening price is too large. Setting a stop loss can reduce risks.

-

Profit target settings may be too aggressive. More optimized profit points can be set based on historical data testing.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Set multiple trading times to cover more trading opportunities.

-

Add stop loss logic to reduce loss risk.

-

Combine more cycle indicators to improve judgment accuracy.

-

Use historical data backtesting to test the optimal profit points.

-

Dynamically adjust position size to manage risks based on specific situations.

Summary

In general, the idea of this fixed time breakback testing strategy is simple and clear. By judging the trend direction at fixed time points and setting profit targets and stop losses to lock in profits and control risks, it is a basic and practical quantitative trading strategy. With more parameter optimization and risk control measures, it can become a reliable quantitative trading system.

- 1