Flawless Victory Quantitative Trading Strategy Based on Double BB Indicators and RSI

Overview

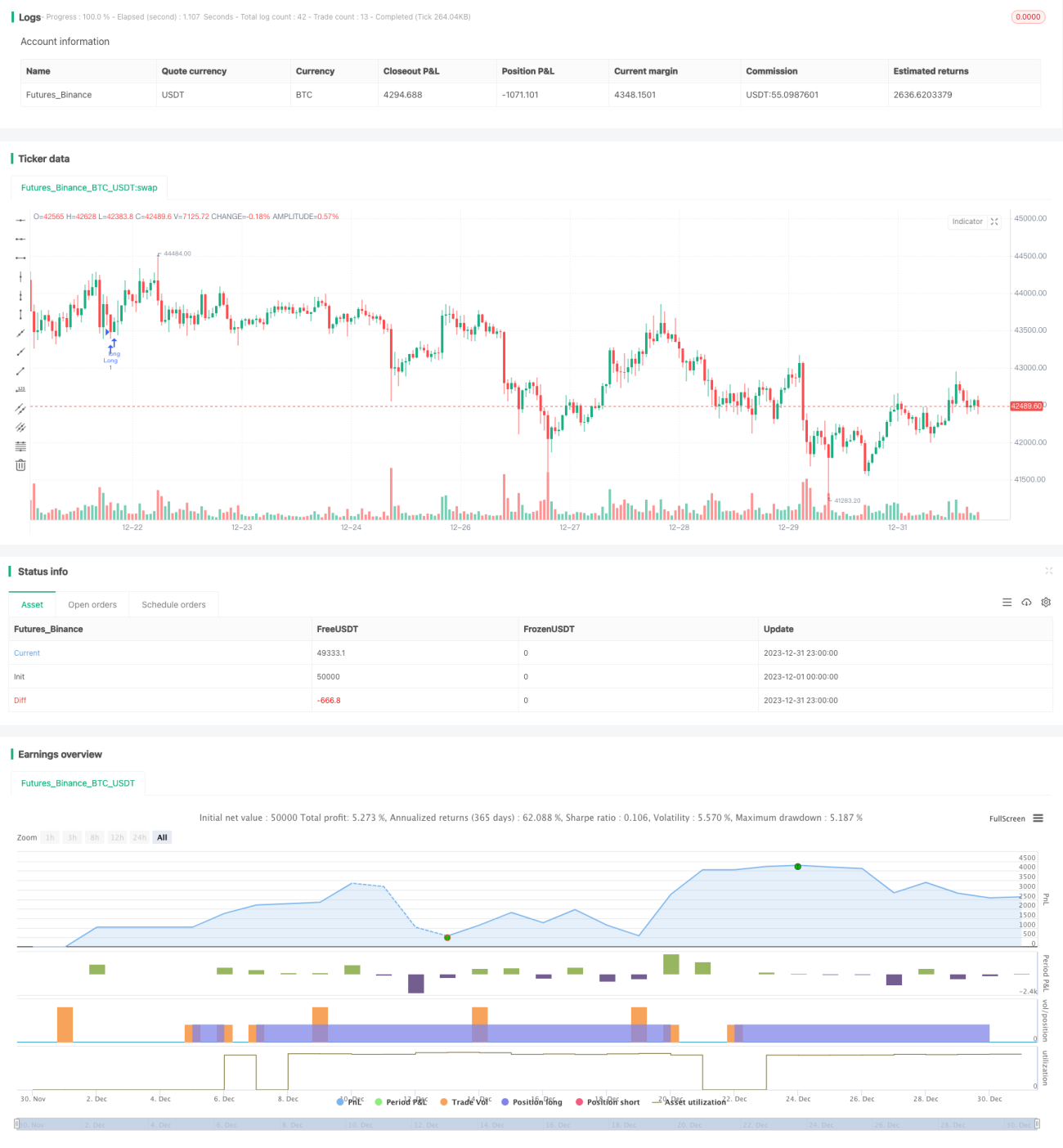

This strategy is a quantitative trading strategy based on the Bollinger Bands indicator and the Relative Strength Index (RSI) indicator. This strategy uses machine learning methods to backtest and optimize parameters over nearly 1 year of historical data using Python language, finding the optimal parameter combination.

Strategy Principles

The trading signals of this strategy come from the combined judgement of double Bollinger Bands and RSI indicators. Among them, the Bollinger Bands indicator is the volatility channel calculated based on the price standard deviation. It generates trading signals when the price approaches or touches the channel. The RSI indicator judges the overbought and oversold situation of the price.

Specifically, a buy signal is generated when the closing price is below the lower rail of 1.0 standard deviations and RSI is greater than 42 at the same time. A sell signal is generated when the closing price is above the upper rail of 1.0 standard deviations and RSI is greater than 70 at the same time. In addition, this strategy also sets two sets of BB and RSI parameters, which are used for entry and stop loss closing positions respectively. These parameters are optimal values obtained through extensive backtesting and machine learning.

Advantage Analysis

The biggest advantage of this strategy is the accuracy of parameters. Through machine learning methods, each parameter is obtained through comprehensive backtesting to achieve the best Sharpe ratio. This ensures both the return rate of the strategy and controls risks. In addition, the combination of double indicators also improves the accuracy and win rate of signals.

Risk Analysis

The main risk of this strategy comes from the setting of stop loss points. If the stop loss point is set too large, it will not effectively control losses. In addition, if the stop loss point does not properly calculate other trading costs such as commissions and slippage, it will also increase risks. To reduce risks, it is recommended to adjust the stop loss magnitude parameter to reduce trading frequency, while calculating a reasonable stop loss position.

Optimization Directions

There is still room for further optimization of this strategy. For example, you can try to change the length parameters of Bollinger Bands, or adjust the overbought and oversold thresholds of RSI. You can also try to introduce other indicators to build a multi-indicator combination. This may increase the profit space and stability of the strategy.

Summary

This strategy combines double BB indicators and RSI indicators, and obtains optimal parameters through machine learning methods to achieve high returns and controllable risk levels. It has the advantages of combined indicator judgement and parameter optimization. With continuous improvement, this strategy has the potential to become an excellent quantitative trading strategy.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Bunghole 2020

strategy(overlay=true, shorttitle="Flawless Victory Strategy" )- 1