ADX, MA and EMA Long Only Trend Tracking Strategy

Overview

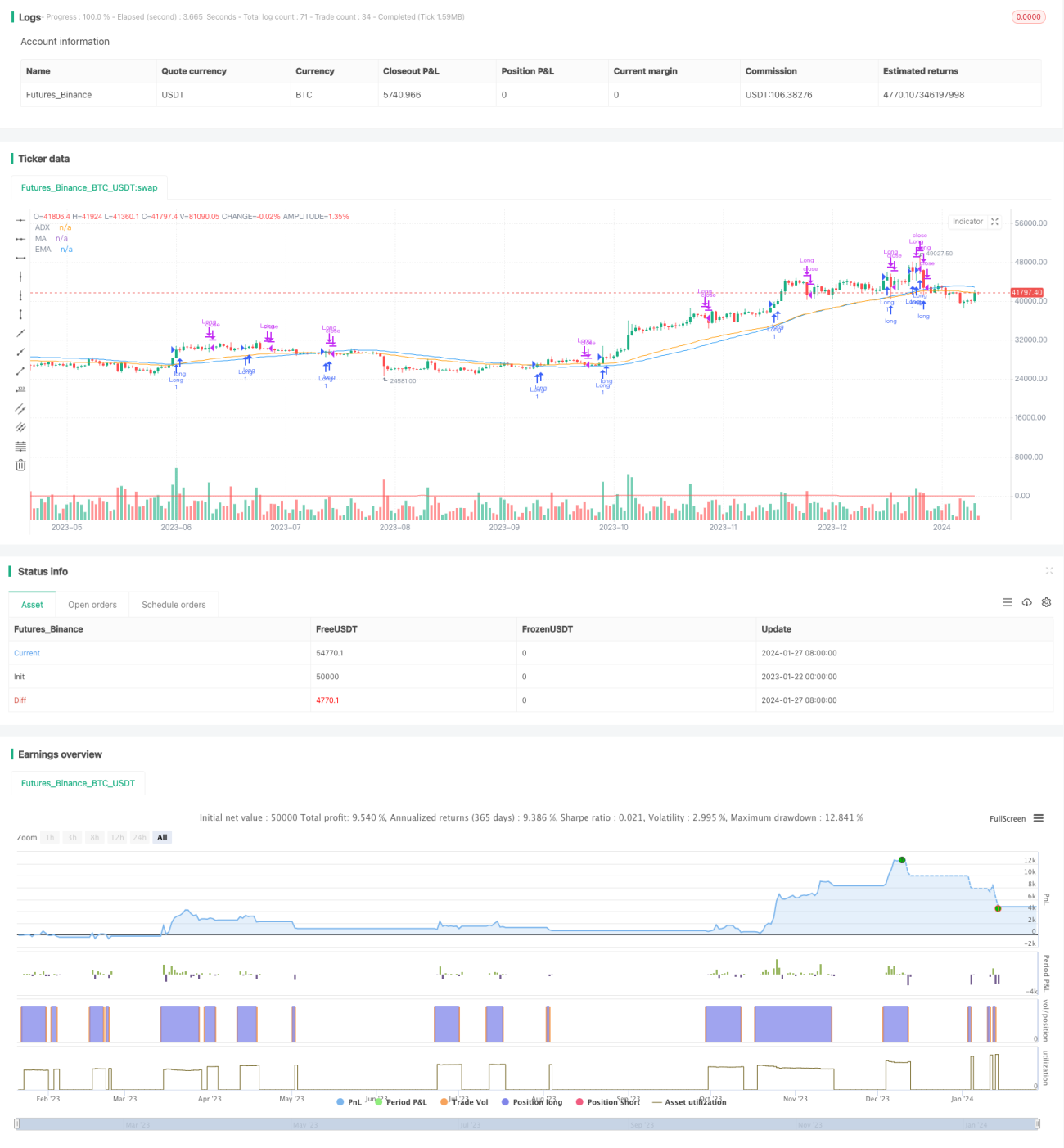

This strategy mainly uses the ADX indicator to judge the trend and combines the MA and EMA moving averages with different parameter settings to build a long-only trend tracking strategy. When ADX rises, it indicates a long direction. When the price breaks through the upward MA and EMA, open long positions. When ADX falls or the price falls below MA or EMA, close positions.

Strategy Principle

The strategy mainly uses ADX to judge market trend and strength. ADX calculates the degree and direction of price changes to determine the existence and strength of the trend. When ADX rises, it means that it is currently in an upward trend. When ADX falls, it means the trend is weakening.

The strategy also uses two moving averages, MA and EMA, with different parameter settings as auxiliary judgment. They can effectively filter the randomness of prices and show the main trend direction of prices. When prices rise and break through MA and EMA, it is a long signal. When prices fall and break through, it is a closing signal.

Combining the characteristics of ADX and moving averages, the strategy builds trading signals to judge the trend direction: go long when ADX rises and prices break through the upward MA and EMA, and close positions when ADX falls or prices break through MA/EMA. It implements a long-only trend tracking strategy.

Advantage Analysis

The main advantages of this strategy are:

- Use ADX to judge the trend strength, reduce invalid trades and track trends.

- Combining two moving averages with different parameter settings can effectively identify trends.

- Only long positions avoid frequent reverse operations and slippage loss.

- Strict entry conditions can effectively control risks.

- Implement a long-only trend tracking strategy.

Risk Analysis

There are also some risks:

- ADX indicator has lag, possibly missing the best entry point.

- Only long positions cannot profit from falling markets.

- There is a certain loss risk when trends change.

- Improper parameter settings also affect strategy performance.

Solutions:

- Adjust ADX parameters to reduce lag reasonably.

- Set stop loss to control single loss.

- Test and optimize parameters to select the best.

Optimization

The strategy can be optimized from the following aspects:

- Add a stop loss strategy to better control risks.

- Add position management to dynamically adjust positions based on market conditions.

- Test and optimize parameters to find the best combination.

- Add machine learning algorithms to dynamically optimize parameters.

- Build martingale strategies to reduce the impact of profit ratio.

Conclusion

In general, this is a long-only trend tracking strategy that uses ADX to judge the trend strength and two moving averages as auxiliary filters. It effectively controls the occurrence of invalid trades and achieves the effect of tracking trends. It is a relatively stable long-only strategy. With some optimizations, the strategy's stability and yield can be further enhanced.

/*backtest

start: 2023-01-22 00:00:00

end: 2024-01-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("ADX, MA, and EMA Long Strategy - ADX Trending Up", shorttitle="ADX_MA_EMA_Long_UpTrend", overlay=true)

adxlen = input(14, title="ADX Smoothing")

dilen = input(14, title="DI Length")- 1