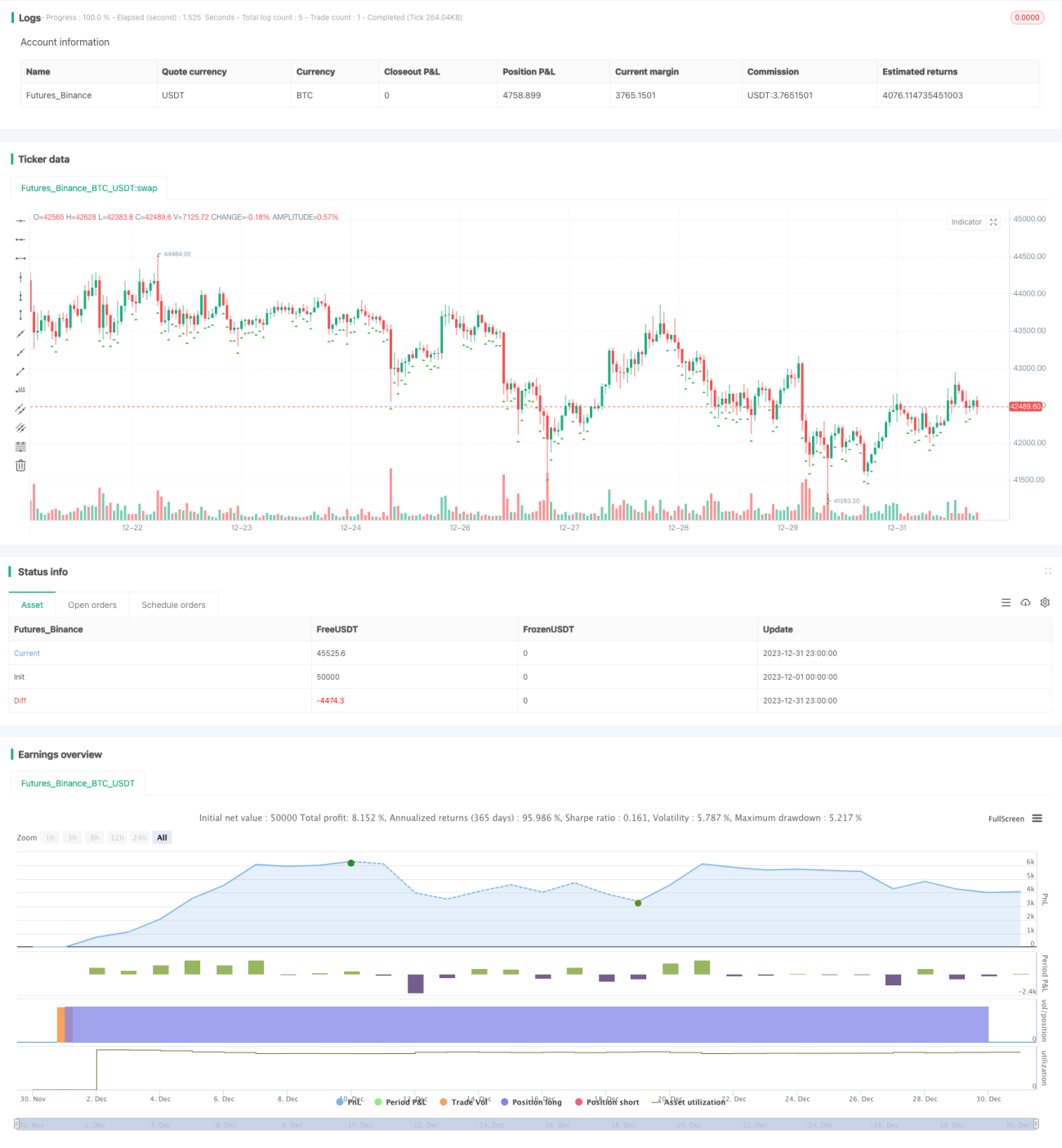

RSI Indicator Grid Trading Strategy

Overview

The RSI Indicator Grid Trading Strategy integrates the RSI and CCI technical indicators with a fixed grid trading approach. It uses the values of RSI and CCI indicators to determine entry signals, and sets take profit orders and additional grid orders based on a fixed profit ratio and number of grids. The strategy also incorporates a hedging mechanism against volatile price movements.

Strategy Logic

Entry Conditions

Long signals are generated when the 5-minute and 30-minute RSI are below threshold values, and the 1-hour CCI is below the threshold. The current close price is recorded as the entry price, and the size of the first order is calculated based on account equity and the number of grids.

Take Profit Conditions

The take profit price level is calculated using the entry price and the target profit ratio. Profit take orders are placed at this price level.

Grid Entry Conditions

After the first order, remaining fixed-size grid orders are placed one by one until the specified number of grids is reached.

Hedging Mechanism

If price increases beyond the set hedging threshold percentage from entry, all open positions are hedged by closing them.

Reversal Mechanism

If price drops beyond the set reversal threshold percentage from entry, all pending orders are cancelled to await new entry opportunities.

Advantage Analysis

- Combines RSI and CCI indicators to improve profitability

- Fixed grid targets profit locking to increase certainty

- Integrated hedging guards against volatile price swings

- Reversal mechanism cuts losses

Risk Analysis

- False signals from indicators

- Price spikes penetrate hedging thresholds

- Failure to re-enter on reversals

These can be mitigated by adjusting indicator parameters, expanding hedging range, reducing reversal range.

Enhancement Areas

- Test more indicator combinations

- Research adaptive profit taking

- Optimize grid logic

Conclusion

The RSI Grid Strategy determines entries with indicators, and locks in stable profits using fixed grid take profits and entries. It also incorporates volatility hedging and re-entry after reversals. The integration of multiple mechanisms helps reduce trading risks and increase profitability rates. Further optimizations of indicators and settings can improve live performance.

- 1