概述

本策略结合使用均线、ATR指标和威廉指标,针对GBP/JPY这个外汇品种进行日线级别的交易。策略先通过均线判断价格趋势和可能的反转点,然后利用威廉指标进一步确认交易信号,同时用ATR指标计算止损位和交易量。

策略原理

- 使用20日线的均线(基线)判断价格整体趋势,价格从均线下方上扫为买入信号,从均线上方下破为卖出信号

- 威廉指标用来确认价格反转。指标上穿-35时为买入确认,下穿-70时为卖出确认

- ATR指标计算过去2天的平均波动范围。该数值乘以系数后设定为止损距离

- 按照账户权益的50%进行风险控制。交易量按照止损距离和风险比例计算

- 进入长仓后,止损点为价格低点减去止损距离。止盈点为入场点加100点。Exiting logic用于进一步确认退出信号

- 进入短仓后,止损和止盈同上。Exiting logic用于进一步确认退出信号

优势分析

- 综合使用均线判断趋势和指标确认进场,可以有效过滤假突破带来的损失

- ATR动态止损可以据市场波动幅度设定合理的止损距离

- 风险控制和动态交易量计算可以最大限度控制单笔损失

- Exiting logic结合均线判断能进一步确认退出时机,避免过早停利

风险分析

- 均线判断产生错误信号的概率较大,需要指标进一步确认

- 指标本身也会产生错误信号,无法完全避免亏损的发生

- 该策略更适合趋势品种,对于范围波动品种效果可能较差

- 风险控制的比例设置不当也可能影响策略收益

可以通过调整均线周期,组合更多指标,或人工干预交易等方法进一步优化和改进。

总结

该策略结合趋势判断和指标过滤,针对GBP/JPY日线级别交易进行方法设计。同时运用动态止损、风险控制等手段控制交易风险。优化空间还很大,通过参数调整和方法组合可以进一步改进策略效果。

策略源码

Pine

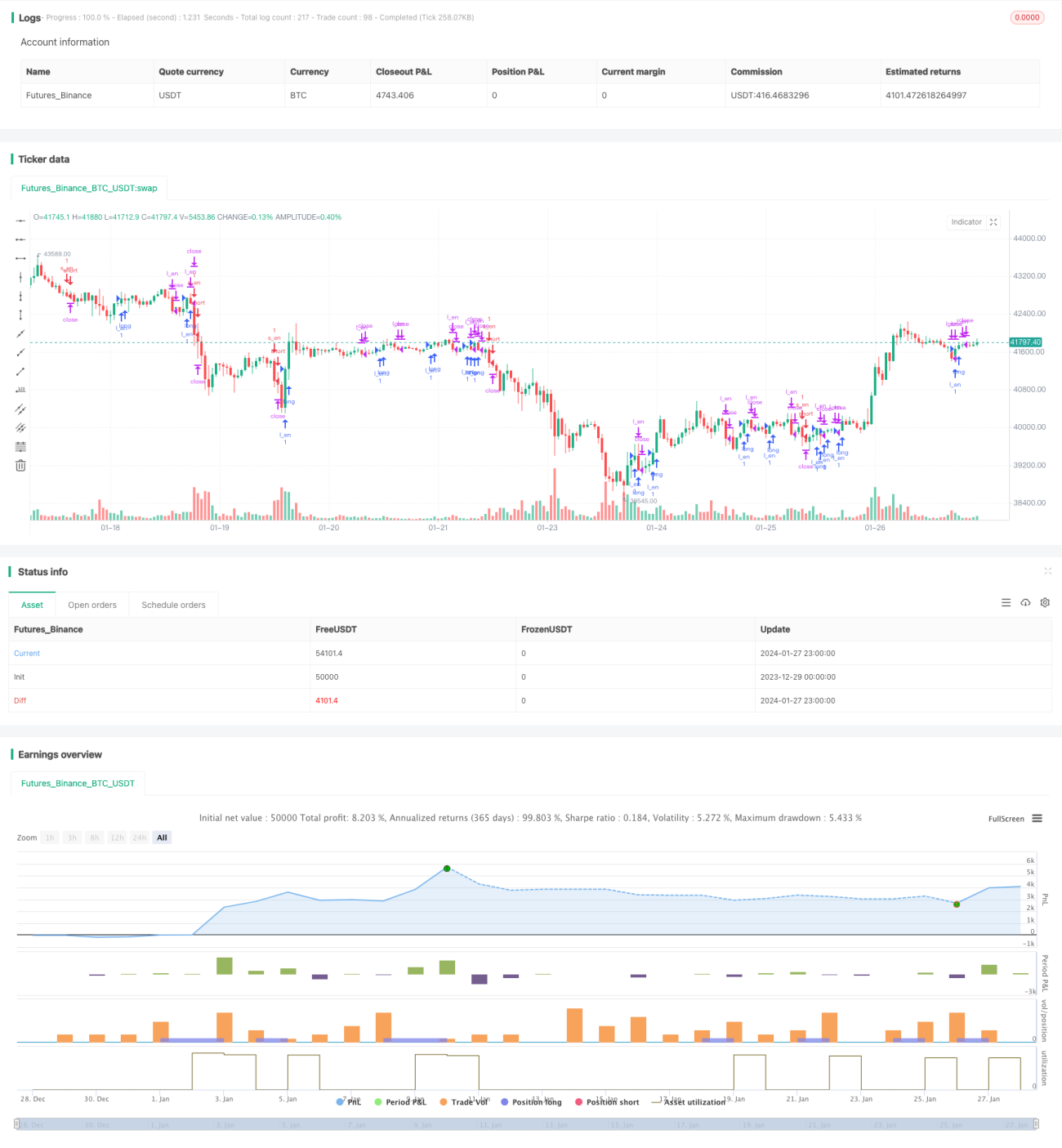

/*backtest

start: 2023-12-29 00:00:00

end: 2024-01-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("GBPJPY DAILY FX",initial_capital = 1000,currency="USD", overlay=true)

UseHAcandles = input(false, title="Use Heikin Ashi Candles in Algo Calculations")策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1