RSI Alligator Trend Strategy

Overview

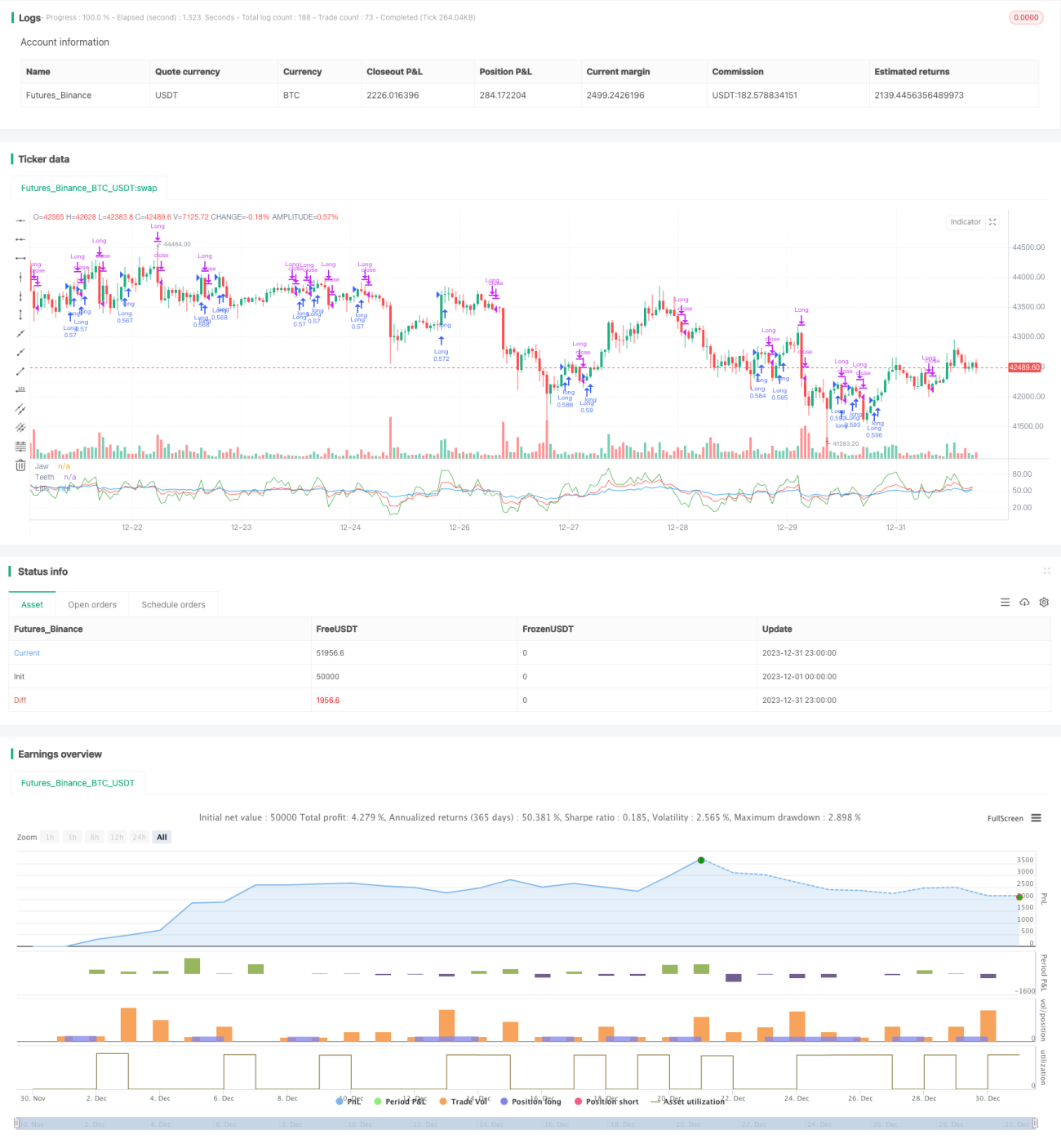

The RSI Alligator Trend strategy is based on the combination of RSI indicator and Alligator indicator to determine the entry and exit of trends. It uses three moving average lines - the alligator's jaw line, tooth line and lip line, constructed by RSI of different periods. It goes long when the tooth line crosses above the lip line and the RSI jaw line is higher than the tooth line; it goes short when the tooth line crosses below the lip line and the RSI jaw line is lower than the tooth line. The strategy also sets stop loss and take profit conditions.

Strategy Logic

The RSI Alligator Trend strategy builds the three lines of the Alligator indicator using RSI indicator. The specific settings are:

- Jaw line: 5-period RSI line

- Tooth line: 13-period RSI line

- Lip line: 34-period RSI line

The entry signal logic is:

Long signal: when the tooth line crosses above the lip line and the jaw line is higher than the tooth line, go long.

Short signal: when the tooth line crosses below the lip line and the jaw line is lower than the tooth line, go short.

The strategy also sets stop loss and take profit conditions:

- Stop loss is set at 10% below the entry price

- Take profit is set at 90% above the entry price

Strength Analysis

The RSI Alligator Trend strategy has the following strengths:

- Using the Alligator lines to determine the trend can effectively filter out market noise and lock in the major trend

- Combining multiple-period RSI avoids false breakouts and improves signal reliability

- Setting reasonable stop loss and take profit conditions helps stabilize strategy operations

- The strategy idea is clear and easy to understand, the parameter settings are simple, and it is easy to implement for live trading

- It can go both long and short, taking into account both directions of the trend, and has strong flexibility

Risk Analysis

The RSI Alligator Trend strategy also has the following risks:

-

There may be false breakouts at the crossover between the tooth line and the lip line, leading to unnecessary losses. The cycle parameters can be adjusted to reduce the probability of false breakouts.

-

The stop loss setting may be too aggressive, with a high probability of unnecessary stop loss. The stop loss range can be appropriately relaxed, or other conditions can be added as prerequisites for activating the stop loss.

-

If the market moves violently, the stop loss may fail to play its proper role of protecting the margin. In this case, manual intervention is required to stop the loss in time.

-

When long and short positions switch frequently, the trading cost pressure is greater. The entry conditions can be appropriately relaxed to reduce unnecessary round trips.

Optimization Directions

The RSI Alligator Trend strategy can be optimized in the following aspects:

-

Optimize the Alligator line parameter settings to find the best parameter combination

-

Optimize the entry condition logic, such as adding indicators like trading volume to filter signals

-

Optimize the take profit and stop loss strategies to make them more adaptive to market conditions and margin levels

-

Add mechanisms to deal with extreme events and avoid exposure to abnormal market conditions

-

Add open position algorithms to control the proportion of capital invested in a single trade to mitigate risks

Conclusion

In general, the RSI Alligator Trend strategy is a reliable and easy-to-use trend following strategy. It uses the Alligator indicator to determine the trend direction, combined with the RSI indicator to set reference thresholds, which can effectively lock in the trend and set reasonable exit points. At the same time, the strategy itself also has strong flexibility and extensibility, making it worthwhile for live trading and further optimization.

- 1