P-Signal Reversal Strategy

Overview

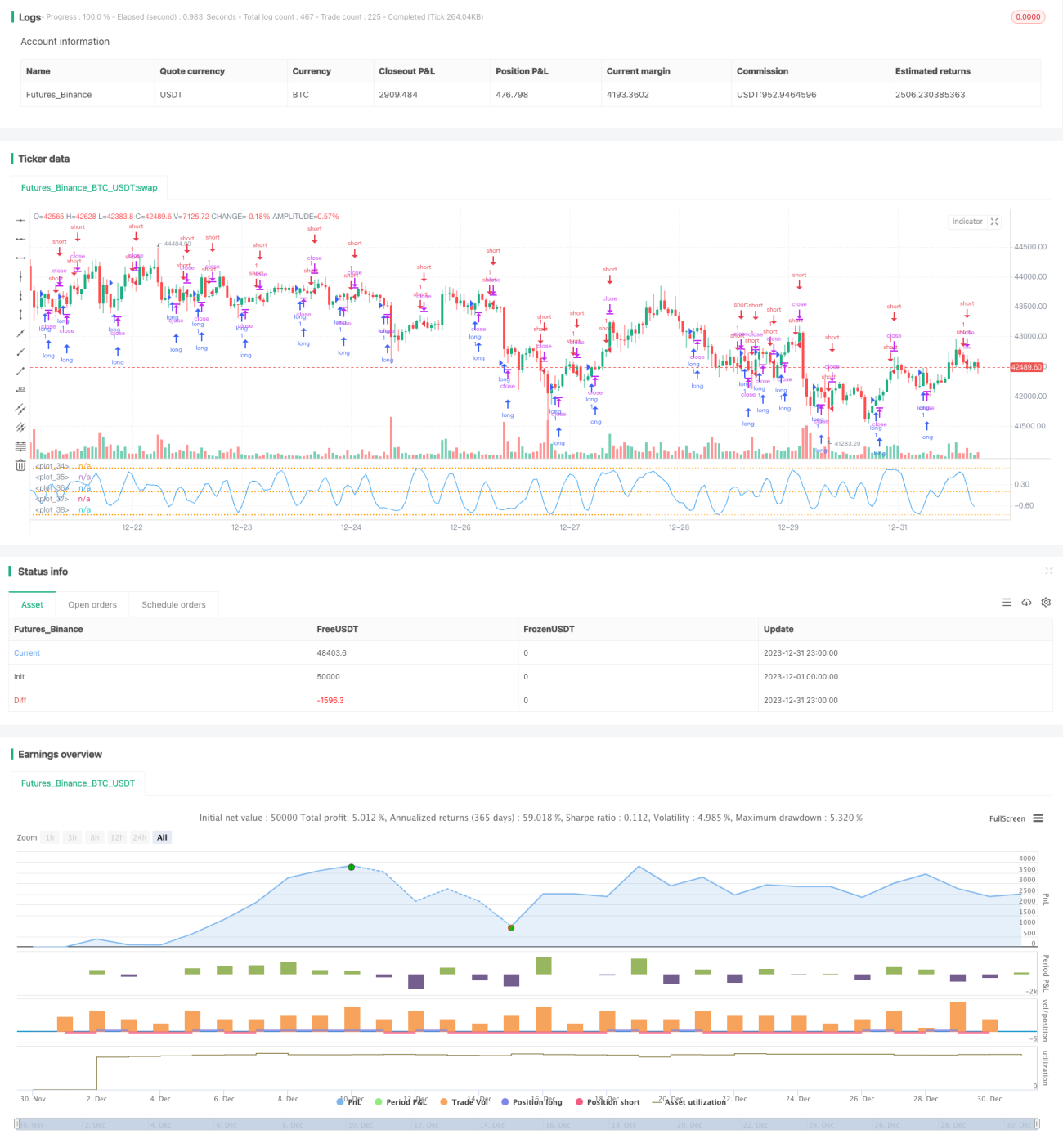

The P-Signal reversal strategy is a quantitative trading strategy built based on statistical parameters and error functions to construct a probabilistic signal space. It dynamically acquires trading signals by tracking the extreme value distributions of a series of K-lines to capture market reversal points.

Strategy Principles

The core indicator of this strategy is the P-signal, which combines the statistical parameters of moving averages and standard deviations and maps them to the range of -1 to 1 through the Gaussian error function to form a quantified judgment indicator. It goes short when the P-signal reverses from positive to negative, and goes long when it reverses from negative to positive, forming a reversal strategy logic.

Strategy parameters include Cardinality, ΔErf and Observation Time. Cardinality controls the sample size, ΔErf controls the dead band of the error function to reduce trading frequency. Observation time controls the start time of the strategy.

Advantage Analysis

The biggest advantage of the P-signal reversal strategy is that it is built on the probability distributions of statistical parameters, which can effectively judge the characteristic points of the market and capture reversal opportunities. Compared with a single technical indicator, it incorporates more market information and makes more comprehensive and reliable judgements.

In addition, the parameterized design of the strategy is well regulated, allowing users to adjust the parameter space according to their own needs to find the optimal combination. This ensures the adaptability and flexibility of the strategy.

Risk Analysis

The main risk of the P-signal reversal strategy is that it relies too much on the parameters of the probability distribution, which is easily affected by abnormal data resulting in misjudgements. In addition, the risk-reward ratio of reversal strategies is generally low, with limited single profit.

Increasing the Cardinality parameter to increase the sample size can reduce the impact of data anomalies. Appropriately expanding the ΔErf range to reduce trading frequency helps control risks.

Optimization Directions

The P-signal reversal strategy can be optimized in the following aspects:

-

Incorporate other indicators to filter out abnormal signals, such as sharp increases in volume.

-

Validate signals across multiple timeframes to enhance judgment stability.

-

Increase stop loss strategies to reduce single losses.

-

Optimize parameters to find the best combination and improve profitability.

-

Incorporate machine learning for dynamic parameter adjustment.

Summary

The P-signal reversal strategy establishes a quantitative trading framework based on probability distributions with flexible parameter designs and user friendliness. It effectively judges the statistical characteristics of markets and captures reversal opportunities. The strategy can be further enhanced in stability and profitability through multi-indicator validation, stop loss optimization and other means. It provides an efficient and reliable paradigm for algorithmic trading using quantitative techniques.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// **********************************************************************************************************

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// P-Signal Strategy RVS © Kharevsky- 1