Dual Moving Average Crossover Trading Strategy

Overview

The Dual Moving Average Crossover Trading Strategy is a quantitative trading strategy that uses moving average crossovers to determine entry and exit signals. This strategy combines moving averages from different timeframes to create multiple layers of filtering and reduce false signals for more reliable trade signals.

Strategy Logic

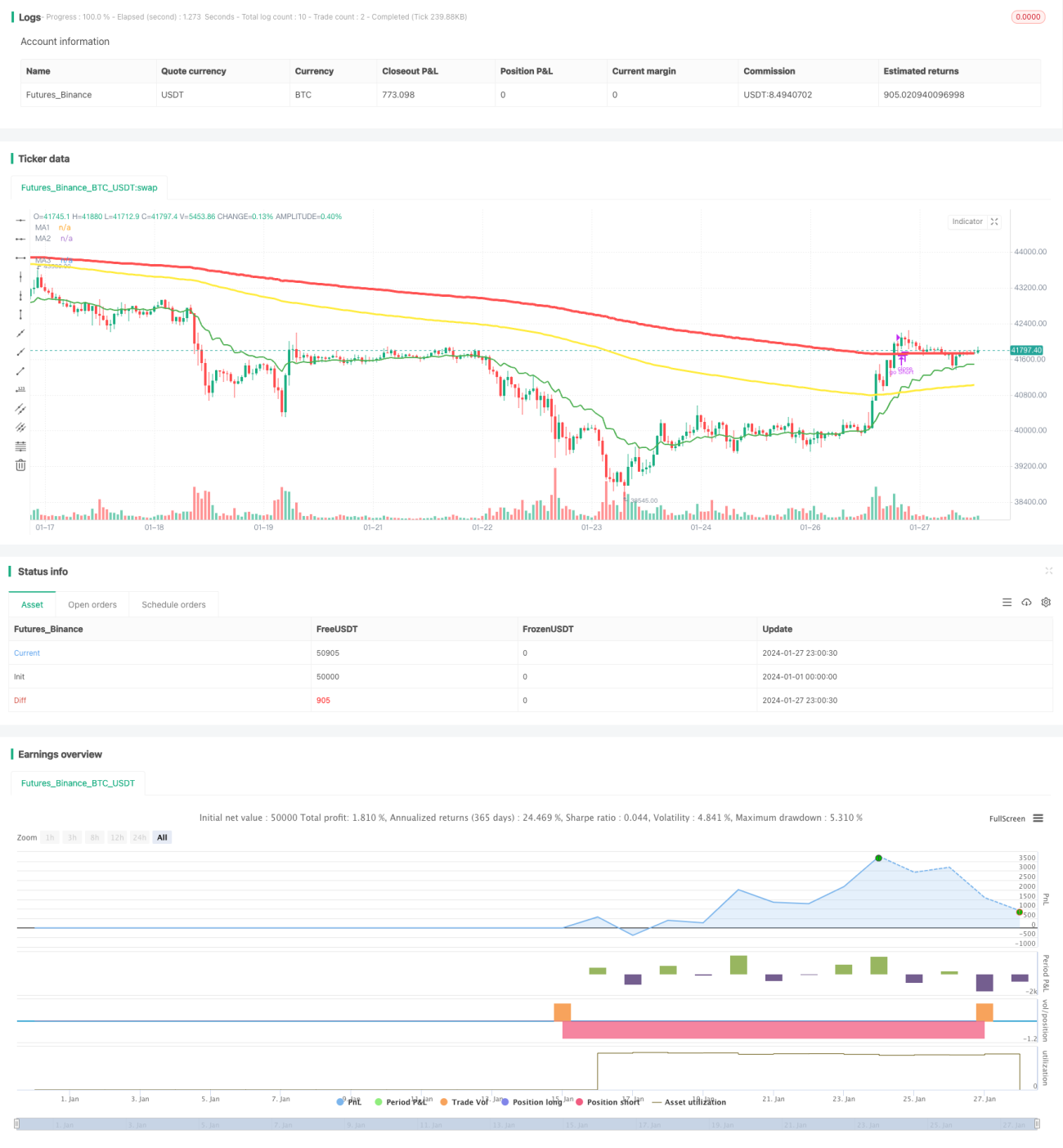

The core logic of this strategy is to track 2 moving averages (10-day and 200-day) across 3 timeframes (180 mins, 60 mins, 120 mins). When the faster moving average crosses above the slower moving average, a golden crossover is generated, indicating the instrument is in an uptrend. When the faster moving average crosses below the slower one, a death crossover is generated, indicating a downtrend.

First, the 10-day and 200-day moving averages are calculated separately for the 180 min and 60 min timeframes. When the 10-day MA on the 180 min timeframe crosses above the 200-day MA, a golden crossover signal is generated. When it crosses below, a death crossover signal is generated. This provides the fast-cycle trading signals.

Next, the strategy introduces the 200-day MA on the 120 min timeframe as a "controlling" moving average. Only when crossovers happen on the 180/60-min cycles, by checking if the 60-min 200-day MA is above or below the 120-min 200-day MA, will decide if trades should be placed to filter out false signals.

For example, when a golden crossover happens on the 180-min cycle, only if the 60-min 200-day MA is above the 120-min 200-day MA, the strategy will go long. The long position will only be opened when this condition is met. Conversely, if the 60-min 200-day MA is below the 120-min one, no long position will be taken.

In summary, by comparing moving average relationships across different timeframes, this strategy creates multiple layers of filtering to improve signal reliability, making it a common type of filter-based trading strategy.

Advantages

-

Improved accuracy via multi-timeframe confirmation. Compared to single-timeframe signals, using MAs from 180/60/120 mins drastically reduces false signals and improves trade signal quality.

-

Reasonable operation frequency. Unlike high-frequency strategies, this strategy trades less frequently, avoiding the need to monitor the market continuously. More suitable for manual trading.

-

Simple and easy to understand. By only using basic moving averages without complex logic, this strategy has a low barrier to entry and is easy to understand for beginners.

-

Optimizable across periods and parameters. The MA types and periods used are adjustable. Different parameter sets can be tested for different products and market regimes.

Risks

-

Lagging indication and slow reaction. The core moving averages have lag by design and often fail to capture quick trend reversals.

-

High whipsaw frequency in ranging markets. When the market is ranging, the MA relationships may cross over very frequently, causing excessive entries and stop loss triggers, heightening costs and loss risks.

-

Overfitting danger from parameter optimization. The alpha mainly comes from parameter tuning based on limited datasets. This likely leads to over-optimization and overfitting problems.

Solutions:

- Shorten MA periods for faster reaction

- Add filters to avoid excessive entries during market choppiness

- Test robustness across different products and time ranges

Optimization Directions

There is still room for further optimizations:

-

Try different combinations of timeframes and tune MA periods to find better parameters, through brute force optimization and machine learning techniques.

-

Incorporate volume and higher timeframe trend analysis for additional signal confirmation, e.g. avoid entries during low trading volumes.

-

Predict curve patterns ahead of time using deep learning models like RNNs to assist decision-making.

-

Introduce adaptive moving averages to improve filtering logic. Dynamically adjust MA periods to reduce entries during market uncertainty.

Conclusion

The Dual Moving Average Crossover Trading Strategy compares moving average relationships across multiple timeframes to filter out false signals, improving signal reliability. This type of filter-based algorithm strategy is common and easy to implement for beginners, while also allowing for extensive optimizations across multiple dimensions, making it worth researching and applying.

- 1