Cross-Border Short-Term Breakthrough Reversal 5EMA Strategy

This article will introduce a short-term reversal trading strategy based on the 5EMA indicator. The strategy mainly uses the 5EMA indicator to judge the price trend and reverse trades when the price breaks through the EMA.

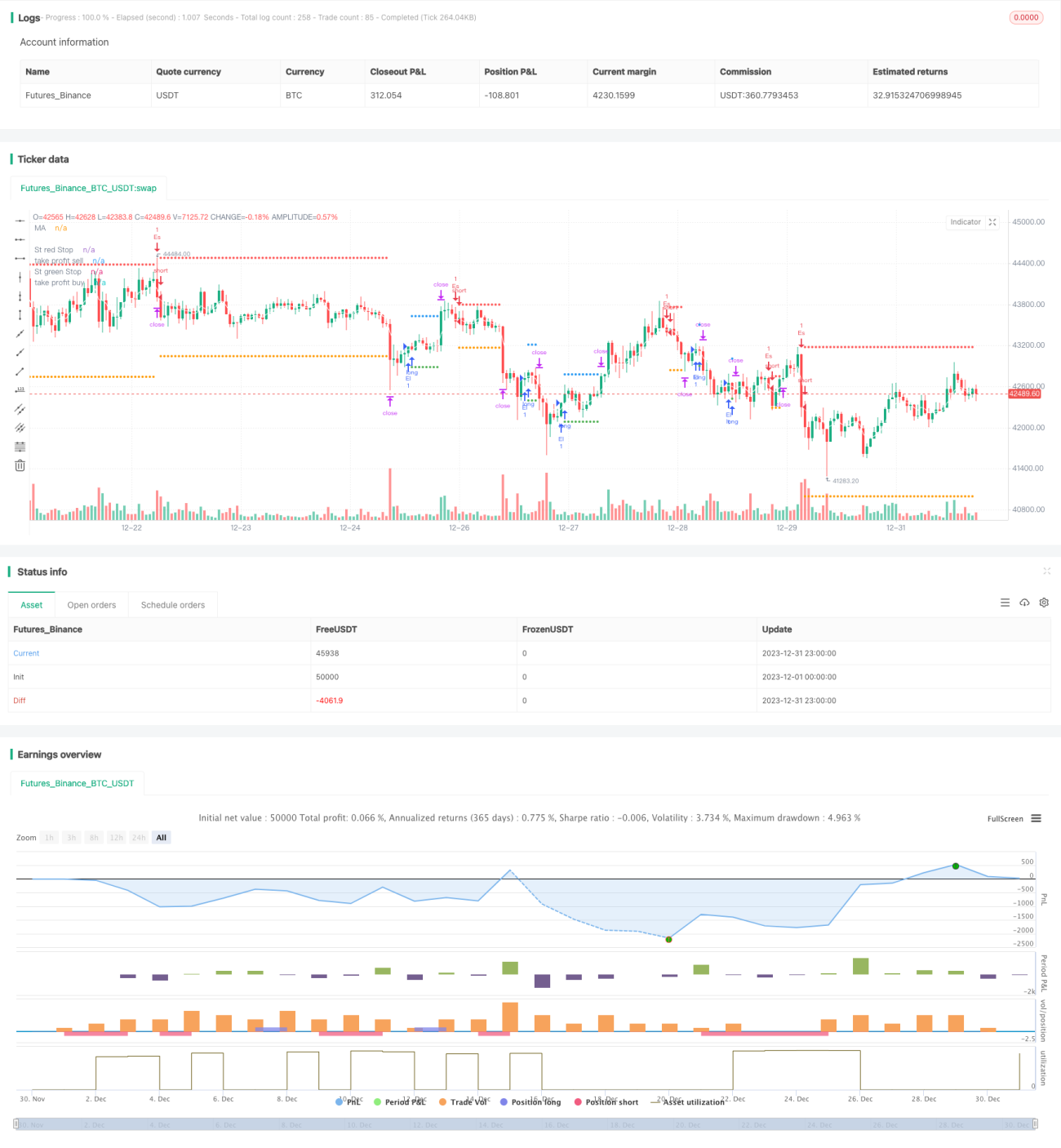

Strategy Overview

This is a short-term quantitative strategy, mainly used for high-frequency trading. The strategy will simultaneously judge bullish and bearish signals and can trade in both directions. Trading signals are generated when prices break through the 5EMA indicator, and long or short positions are entered according to the direction of the breakthrough.

The advantage of the strategy is to capture short-term price reversal opportunities and quickly enter the market. The main risk comes from losses caused by false breakouts. Risk can be reduced by optimizing parameters.

Strategy Principle

-

Use 5-period EMA indicator to determine short-term price trend

-

Judge whether the price breaks through the EMA indicator

-

When the price breaks through the EMA from top to bottom, a sell signal is generated.

-

When the price breaks through the EMA from bottom to top, a buy signal is generated.

-

Set stop loss and take profit to limit single loss

Since the EMA indicator can effectively determine short-term trends, it can quickly capture trading opportunities when prices show significant reversals. The 5EMA parameter is relatively flexible and responds quickly to the market, making it suitable for high-frequency trading.

Advantages of the Strategy

- Fast response, suitable for high-frequency capturing of short-term trading opportunities

- Two-way trading, can be long and short at the same time

- Reasonable stop loss and take profit settings, single loss limited

- Simple parameter settings, easy to optimize strategies

Risks and Solutions of Strategies

- Unnecessary losses caused by false breakout risks

- Optimize EMA cycle parameters to ensure indicator stability

- Excessive trading frequency can easily chase highs and kill lows

- Limit maximum number of trades per day

Optimization Direction of Strategies

- Optimize EMA indicator parameters to find the best cycle portfolio

- Increase filter to reduce false breakout probability

- Limit maximum number of trades per day

- Combine other indicators to determine trend direction

Summary

In general, this is a very practical short-term breakout strategy. Using EMA indicators to determine price reversals is very simple and effective, and an important tool for quantitative trading. Through parameter optimization and risk control settings, the win rate of strategies can be greatly improved, which is highly recommended.

- 1