Dual Breakthrough Strategy

Overview

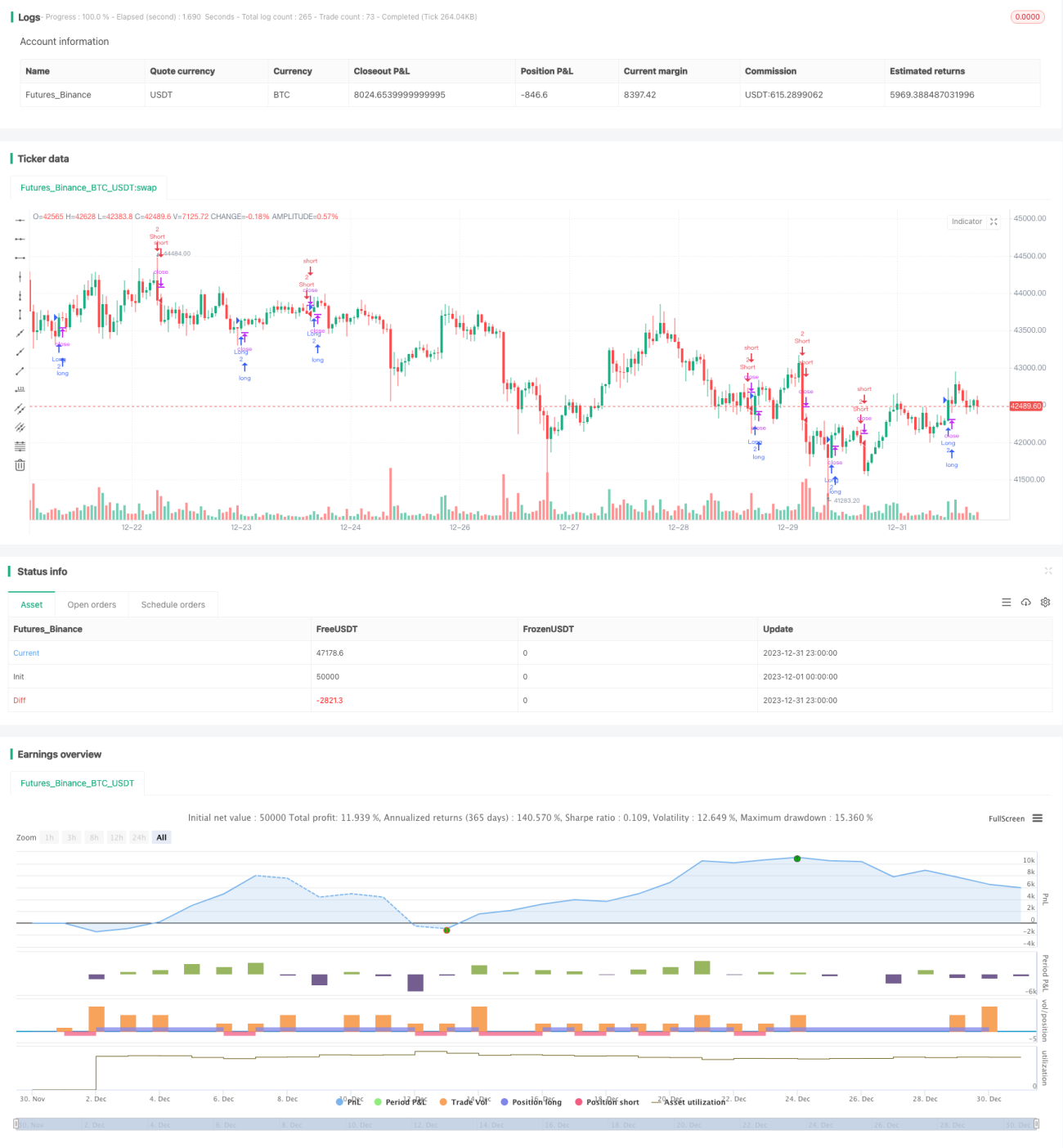

This is a dual breakthrough trading strategy based on K-line. It will generate trading signals when the closing price of the current K-line has a breakthrough relative to the highest and lowest prices of the previous two K-lines.

Strategy Principle

The basic logic of the strategy is:

-

Define bull signal:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]. That is, the closing price of the current K-line is greater than the opening price, and greater than the highest price of the previous two K-lines, while the lowest price of the current K-line is lower than the lowest price of the previous K-line. -

Define bear signal:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]. That is, the closing price of the current K-line is less than the opening price, and less than the lowest price of the previous two K-lines, while the highest price of the current K-line is higher than the highest price of the previous K-line. -

When a bull signal is triggered, go long; when a bear signal is triggered, go short.

-

Stop loss and take profit can be set.

The strategy utilizes the characteristics of dual breakthroughs to judge changes in trends through breakthroughs of key price zones, thereby generating trading signals.

Advantage Analysis

This is a relatively simple and intuitive breakout strategy with the following advantages:

-

The logic is clear and easy to understand and implement, with a low barrier to entry.

-

Breakthroughs are common trading signals that tend to form trends easily.

-

Going both long and short allows for dual directional trading, increasing profit opportunities.

-

Flexible stop loss and take profit settings help control risk.

Risk Analysis

The strategy also carries some risks:

-

Dual directional trading carries higher risks and requires close monitoring.

-

Breakouts can be vulnerable to traps, potentially forming false signals.

-

Improper parameter settings may lead to overtrading.

-

Improper stop loss and take profit settings can also affect profit potential.

Risks can be reduced by optimizing parameters and appropriately filtering products.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Optimize parameters like breakout cycle, stop loss/take profit range etc.

-

Add filtering conditions to avoid errors from arbitrage, sideways movements etc.

-

Incorporate trend indicators to avoid consolidation ranges.

-

Optimize capital management, improve position algorithms.

-

Different parameters for different products, test and optimize separately.

Summary

This is a simple strategy based on the dual breakout concept. It has the advantage of clear logic and easy implementation, but also carries certain monitoring risks. Better strategy results can be expected through parameter and condition optimization.

- 1