Multi Timeframe MACD Trading Strategy

Overview

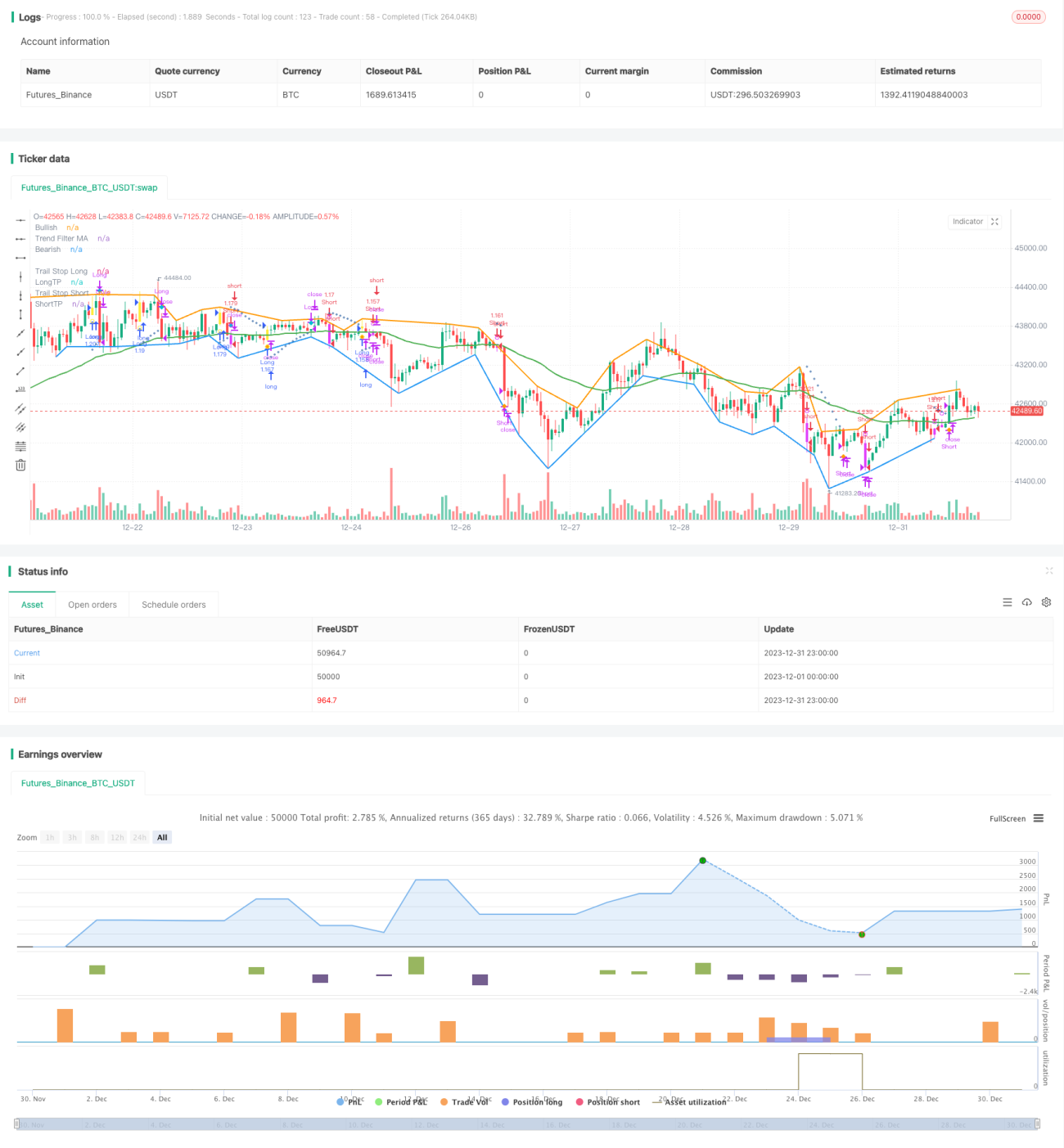

This strategy is based on the classic MACD indicator, combined with trend judgment indicators, stop loss methods and take profit methods to form a relatively complete trend tracking trading strategy. It can be used for both cryptocurrency, forex and stock trading.

Trading Logic

-

MACD Indicator

- The difference between FASTLENGTH period EMA and SLOWLENGTH period EMA forms the MACD histogram

- MACDLENGTH period EMA smooths the MACD histogram to form the MACD line

- MACD histogram crossing 0 axis forms trading signals

-

Trend Filter

- ADX: Average Directional Index, to judge if a trend exists

- MA: Moving Average, price above and below MA forms a trend

- SAR: Parabolic SAR, SAR moving above and below price indicates trend

-

Stop Loss

- ATR Trailing Stop: Set stop loss based on ATR percentage

- SAR Stop Loss: Use SAR as trailing stop loss

-

Take Profit

- ATR Fixed Take Profit Distance: Set fixed take profit distance based on ATR

- Percentage Take Profit: Set percentage take profit distance

-

Timed Exit

- Can set exit after specified number of bars

Advantage Analysis

-

Multiple Auxiliary Judgement

- Trend, support and resistance judgment avoids false signals

- ATR/SAR stop loss better controls risk

-

Flexible Configuration

- Choose whether to use trend filter

- Choose ATR or SAR stop loss

- Choose ATR or standard take profit

- Parameters are configurable

-

Divergence Analysis Provided

- Displays historical regular/hidden divergences

- Provide text notifications

-

Easy to Optimize

- Many built-in configurable parameters

- Easy to test different parameter combinations

Risk Analysis

-

Improper Parameters May Increase Losses

- Improper ATR, SAR parameters may premature stop loss

- Excessive take profit ratio may premature take profit

-

Trend Failure Risk

- Improper trend indicator parameters may cause misjudgement

- Black swan events may cause trend failure

-

Timed Exit Risks

- Fixed timed exit risks losses

Optimization Directions

- Adjust ATR, SAR parameters for smoother stops

- Test different MA periods to optimize trend judgement

- Test adjusted take profit ratios to increase profit rate

- Incorporate volatility indicators to optimize configurations

Conclusion

This strategy comprehensively considers trend, stop loss, take profit, pullback identification to form a relatively complete cryptocurrency trading strategy. It combines the advantages of MACD indicators, adds trend filtering to avoid false trading; adds ATR/SAR stop loss for better risk control; pullback identification provides extra reference. The multiple configurable parameters can be easily tested and optimized. Overall, this strategy can serve as a great example for cryptocurrency strategy research.

- 1