Dual Breakout Volatility Channel Strategy

Overview

The dual breakout volatility channel strategy calculates the middle, upper and lower bands of the channel and uses trend and volume indicators to determine market direction and momentum. It sets breakout signals on both sides of the channel to achieve the goal of buying low and selling high.

Strategy Logic

The core indicator of this strategy is the statistically-based volatility channel of candlestick lines. The middle band adopts the moving average algorithm and the upper and lower bands adopt the average true range method to dynamically capture the boundaries of price fluctuations. At the same time, the strategy incorporates DMI and volume criteria to avoid false breakouts.

Specifically, when the price breaks out of the lower rail into the channel, the +DI line of the DMI exceeds the -DI line and the set ADX benchmark, and the trading volume increases, a buy signal is generated. Conversely, when the price breaks through the channel downward from the upper rail, the judgment rules are opposite to the above, generating a sell signal.

Advantage Analysis

The biggest advantage of this strategy is capturing the major breakthrough direction of prices. The dual breakout judgment can effectively avoid sideways and shock markets and reduce the number of stop losses. Compared with simple moving average strategies, the volatility channel breakout judgment is more adaptive to price fluctuations.

In addition, the introduction of auxiliary indicators DMI and volume also plays a good filtering role, avoiding false signals. So from the win rate and profit-loss ratio point of view, the strategy has some advantages.

Risk Analysis

The biggest risk of the dual breakout strategy is that it cannot judge market reversals. If a V-shaped reversal occurs in the market, the stop loss point may be easily triggered. In addition, improper parameter settings can also negatively impact the trading system.

To address the risks, we can further optimize parameter settings and narrow down stop losses to reduce risks. Of course, trading systems can never completely avoid losses, the key is to control risks.

Optimization Directions

The strategy also has great potential for optimization, which can be improved in the following aspects:

-

Parameter optimization, such as fine tuning of DMI’s DI and ADX lengths, period and multiplier settings of volatility channels, etc.

-

Increase filtering conditions, such as combining MACD and other indicators to avoid false breakouts

-

Implement automatic tracking of take profit and stop loss to further control risks

-

Optimize parameter settings and filtering rules for different products

Summary

In general, the dual breakout volatility channel strategy is an effective breakout system. It can effectively determine the main trend direction and momentum, and has great potential in optimization and risk control. If improved and optimized systematically, the strategy can profit steadily in the long run.

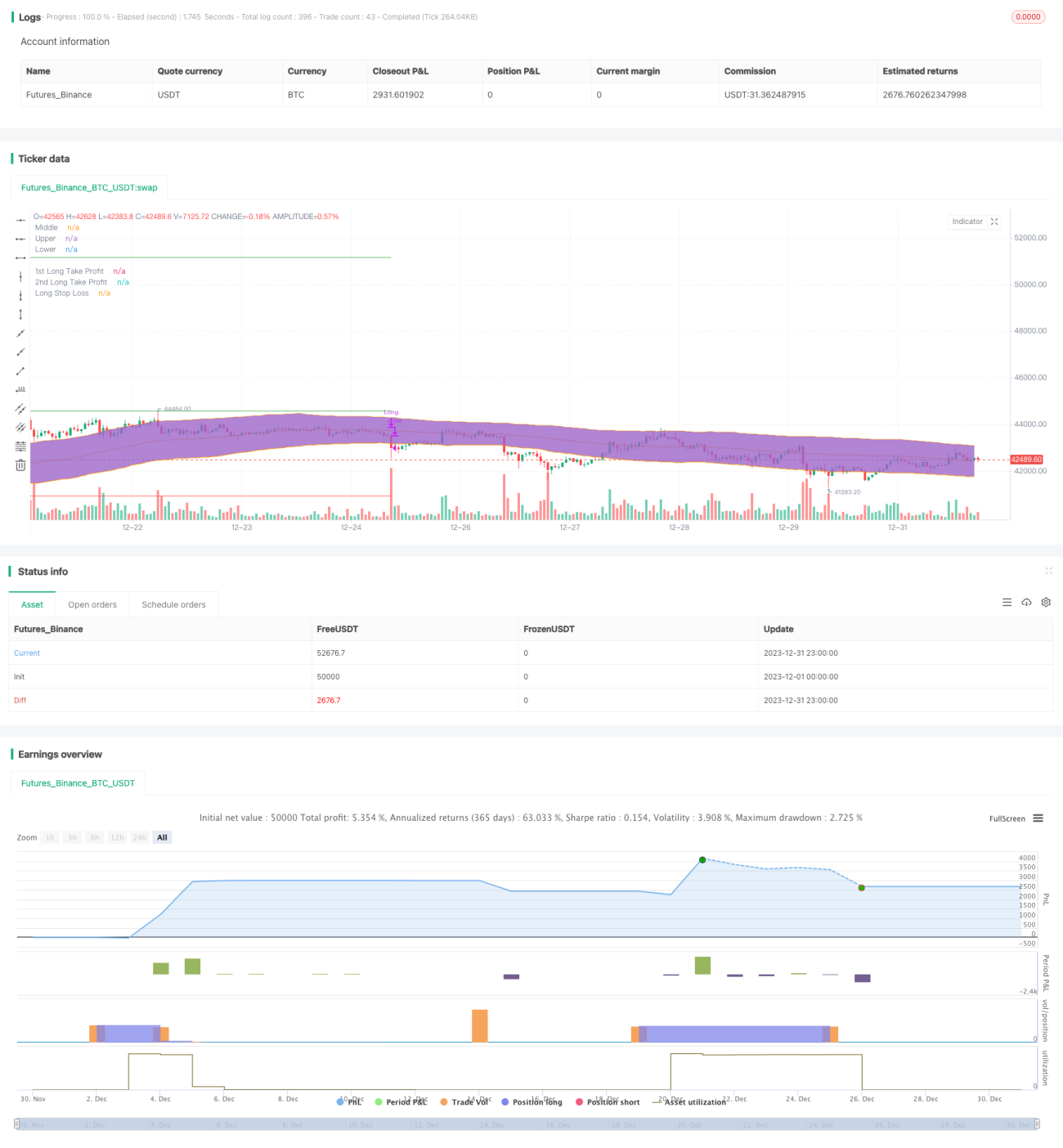

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Original Idea by: Wunderbit Trading

//@version=5

strategy('Keltner Channel ETH/USDT 1H', overlay=true, initial_capital=1000, pyramiding=0, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.07)- 1