Dual MA Momentum Breakout Strategy

Overview

The Dual MA Momentum Breakout Strategy is a quantitative trading strategy that combines dual moving average lines and RSI indicators. It calculates fast moving average, slow moving average and RSI to set overbought/oversold thresholds for the momentum indicator RSI. It goes long when the dual MAs have golden crosses and goes short when there are death crosses, in order to capture the trending moves in the market.

Logic

The Dual MA Momentum Breakout Strategy is mainly based on dual moving averages and RSI indicator. It first calculates one fast and one slow moving average line, with the fast MA being the 10-day weighted moving average and the slow MA being the 100-day linear adaptive moving average. Then it calculates the 14-day RSI and sets overbought/oversold thresholds. When the fast MA crosses above the slow MA, it signals an uptrend, and when the fast MA crosses below the slow MA, it signals a downtrend. In addition to determining the trend direction, the strategy also requires the RSI to be above the overbought threshold or below the oversold threshold to effectively filter out fake breakouts.

Specifically, when an uptrend is identified, if the RSI is above the overbought threshold at this time, a long position will be opened. When a downtrend is identified and the RSI is below the oversold threshold, a short position will be opened. After opening a position, the opposite position will be opened when the trading signal is reversed.

Advantage

The Dual MA Momentum Breakout Strategy combines dual MAs and RSI to effectively identify market trends and uses the RSI to filter out fake breakouts, thereby improving the reliability of trading signals. Compared to a single MA system, this strategy can greatly reduce the occurrence of ineffective trades. In addition, the parameter optimization of the RSI also provides flexibility for the strategy.

Risk

The Dual MA Momentum Breakout Strategy also carries some risks. The dual MA system is very sensitive to parameters and different parameter combinations need to be carefully tested for different markets. In addition, improperly set thresholds for RSI may also lead to missing trading opportunities. Finally, aggressive trailing stops may be penetrated in certain market conditions, so stop loss points should be adjusted based on backtesting results.

Optimization

The Dual MA Momentum Breakout Strategy can be optimized in the following aspects:

- Optimize fast and slow MA parameters to find the best parameter combination;

- Optimize RSI parameters and adjust overbought/oversold thresholds;

- Add adaptive trailing stop mechanisms to control risks;

- Add position sizing optimization module to improve capital use efficiency.

Conclusion

The Dual MA Momentum Breakout Strategy determines trend direction through the dual MA system and uses RSI to filter signals, which can effectively improve the shortcomings of a single MA system. This strategy has large optimization space for parameters and can achieve adaptive adjustment. It is an excellent trend following strategy.

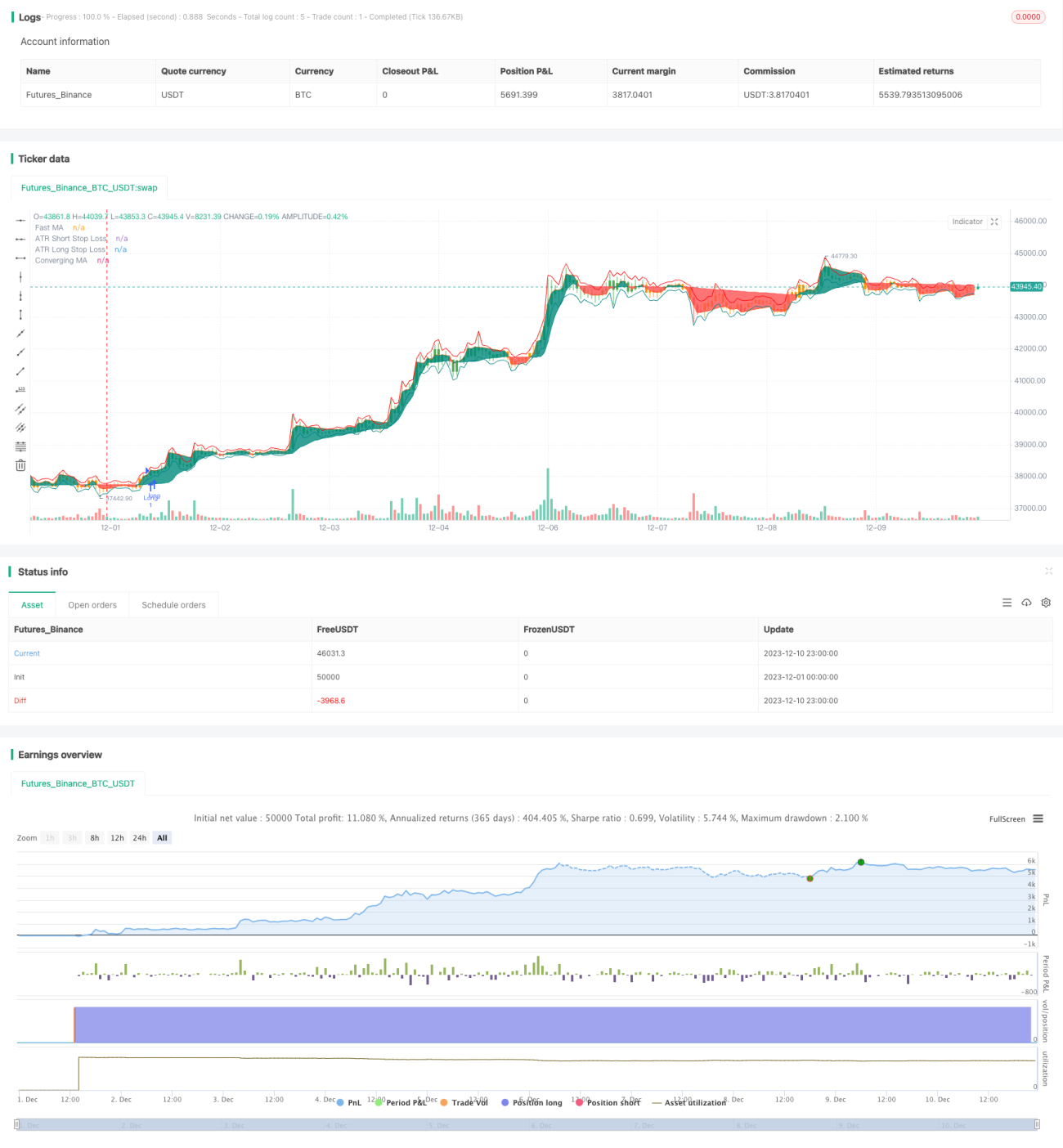

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1