Dual-Mechanism Dynamic Trend Tracking Strategy

Overview

The Dual-Mechanism Dynamic Trend Tracking strategy combines signals from two different trading strategies to track trends. It first uses the 123 Reversal strategy to identify price reversal points, then uses the Detrended Synthetic Price (D_DSP) index to determine price trend direction, and finally generates trading signals by combining both signals.

This strategy is mainly used for medium-term trend tracking. By setting dynamic stop-loss points through dual mechanisms, it can effectively lock in profits and avoid losses from expanding. Meanwhile, combining trend and reversal indicators for dual confirmation helps reduce noisy trades.

Strategy Logic

123 Reversal Strategy

The 123 Reversal strategy originates from page 183 of Ulf Jensen's book "How I Tripled My Money in the Futures Market". It identifies price reversal patterns using two consecutive reversal bars.

Specifically, it generates a buy signal when the close price is higher than the previous close for two consecutive days and the 9-day Slow Stochastic Oscillator is below 50. It generates a sell signal when the close price is lower than the previous close for two consecutive days and the Fast Stochastic Oscillator is above 50.

Detrended Synthetic Price Index

The Detrended Synthetic Price (D_DSP) index indicates the price trend direction and is in phase with the dominant cycle of the actual price data. The D_DSP is calculated by subtracting a half-cycle exponential moving average (EMA) from the quarter-cycle EMA of price.

If D_DSP is positive, it indicates an upward price trend. If negative, it indicates a downward price trend.

Dual Mechanism

This strategy combines the 123 Reversal strategy and D_DSP index signals. If both signals agree (both long or short), trades will be generated. If signals disagree, positions will be closed.

This dual confirmation filters out noise and locks in trend profits.

Advantages

The biggest advantage of this strategy is the two levels of stop loss it implements. Firstly, the fast and slow Stochastics form a time-staggered stop loss. Secondly, the reversal strategy itself contains a stop loss feature.

The two stop losses maximize profit locking and prevent crossover losses from a single stop loss strategy. Also, the dual confirmation avoids wrong signals from non-mainstream price changes.

Risks

The biggest risk comes from inflexible parameter settings. For example, wrong cycle lengths may cause missing mainstream trends, losing profits or increasing losses. Overly rigid dual confirmation may also cause missed timely stop losses.

Also, when combining reversal and trend strategies, clearing positions when signals disagree may miss opportunities when the trend continues in one mainstream direction.

Optimization

This strategy can be optimized in several ways:

-

Optimize cycle parameters using more backtesting data to find optimal values.

-

Add more stop loss strategies like breakout or trailing stop loss to set more dynamic and reasonable stop loss points.

-

Fine tune the dual confirmation rules to prevent over-clearing positions.

-

Add filters like volatility filters to avoid misjudgments from late-stage trend volatility.

Conclusion

The Dual-Mechanism Dynamic Trend Tracking Strategy implements effective trend tracking and risk control through dual stop losses of fast and slow Stochastics and dual confirmation of reversal and trend signals. It considers both the time dimension of price action as well as the direction itself to form a multidimensional decision basis.

Continuous optimization of rules and parameters is expected to yield good results. But strategy optimization requires large amounts of historical data. Stock selection filters and stop loss mechanisms also need continuous refinement. Real-time tracking for some period is recommended to further validate the strategy.

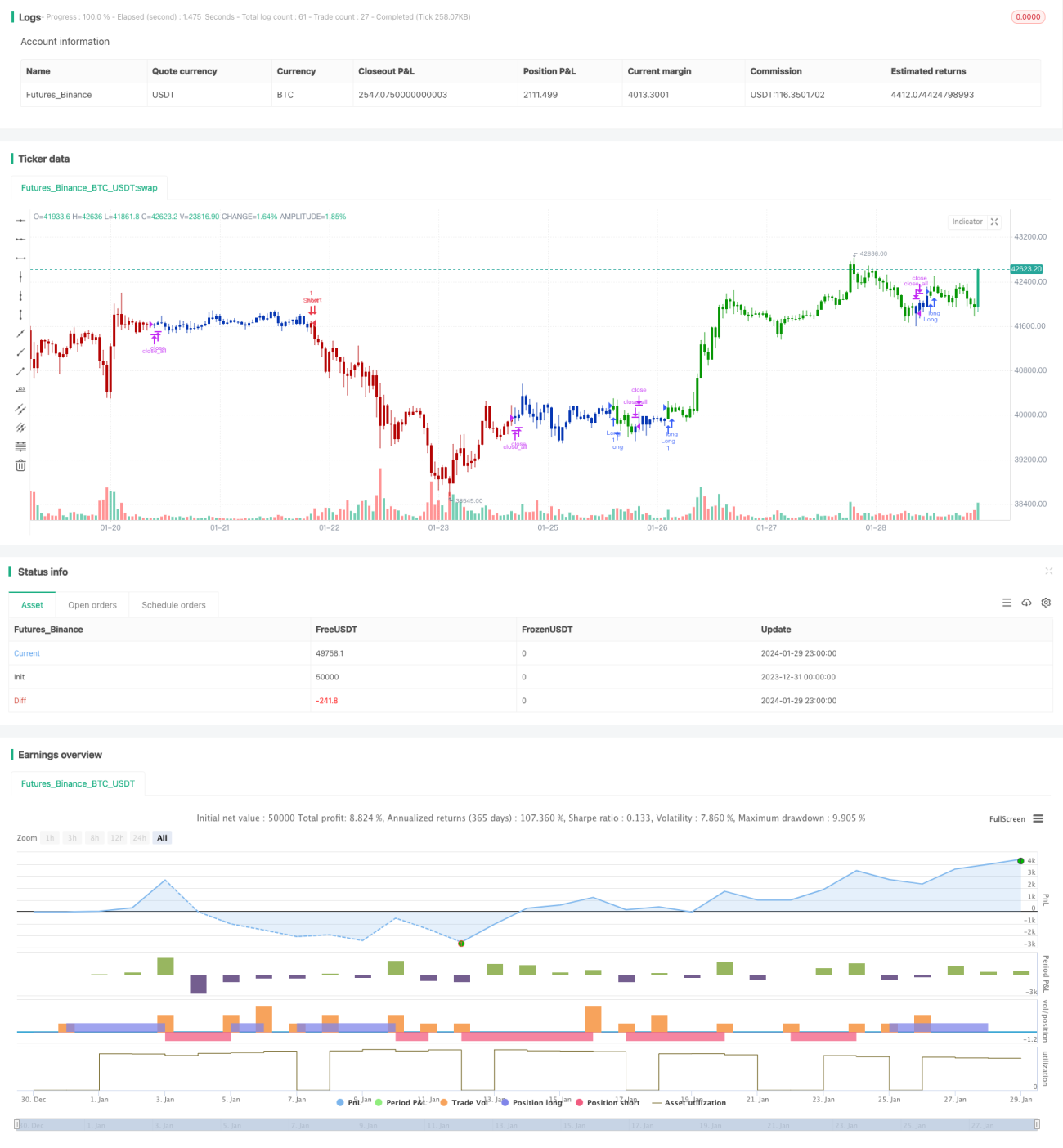

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/11/2019

// This is combo strategies for get a cumulative signal. - 1