CCI and EMA Based Scalping Strategy

Overview

This is a short-term oscillation trading strategy that combines the EMA indicator and CCI indicator to identify short-term trends and overbought/oversold levels in the market, in order to capture opportunities from short-term price fluctuations.

Strategy Logic

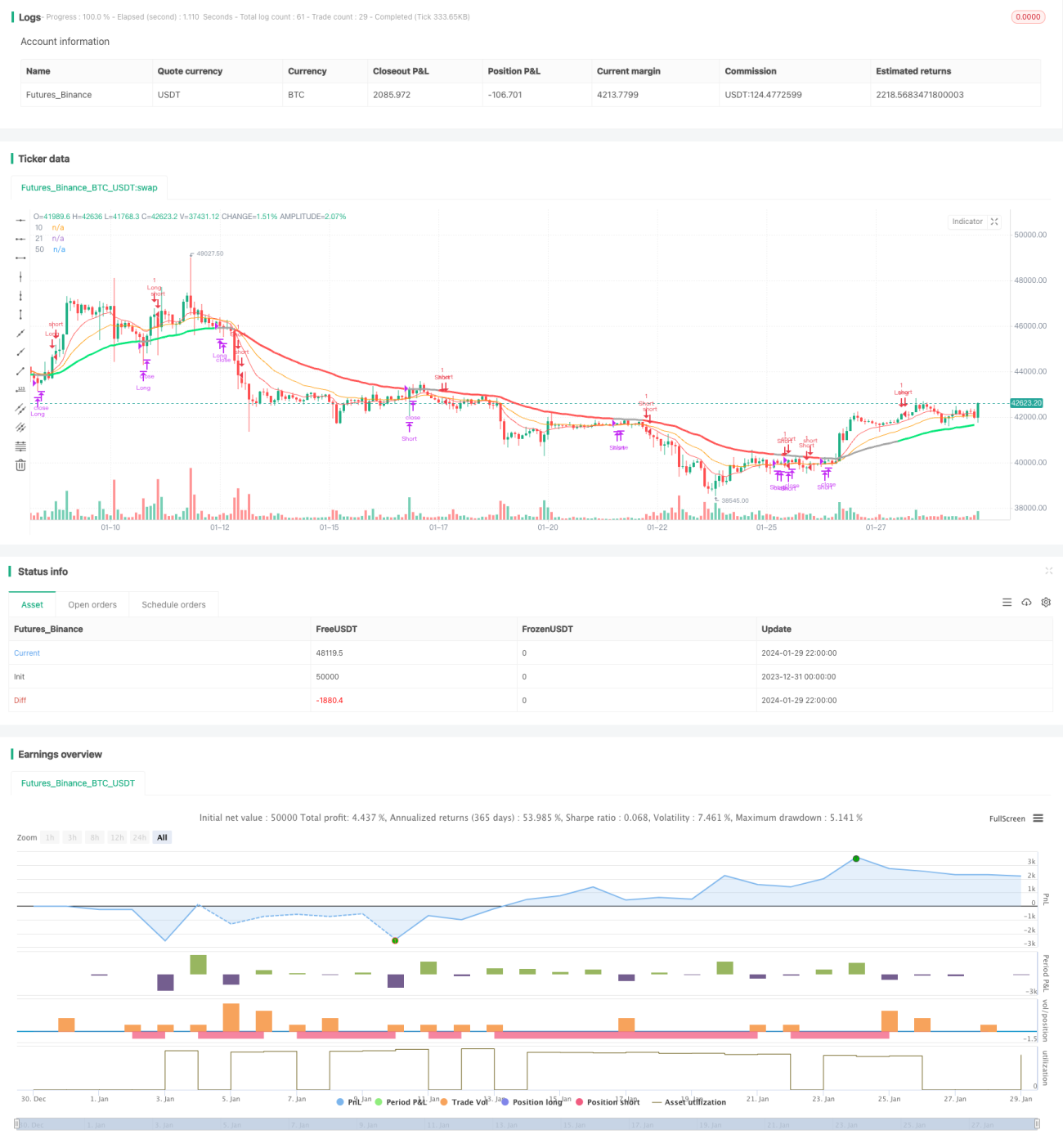

The strategy mainly uses the 10-day EMA, 21-day EMA and 50-day EMA lines and the CCI indicator to determine entry and exit timing.

The specific logic is:

When the short-term moving average (10-day EMA) crosses above the medium-term moving average (21-day EMA) and the short-term moving average is higher than the long-term moving average (50-day EMA), and at the same time the CCI indicator is greater than 0, it is considered a bullish signal to go long. When the short-term moving average crosses below the medium-term moving average and the short-term moving average is lower than the long-term moving average, and at the same time the CCI indicator is less than 0, it is considered a bearish signal to go short.

The exit logic is to close the position when the short-term moving average crosses back over the medium-term moving average.

Advantages

-

Combining moving average system and CCI indicator can effectively identify short-term price trends and overbought/oversold levels.

-

Using moving average crossovers to determine entries and exits is simple and practical.

-

CCI parameter and cycle settings are more reasonable to filter out some false signals.

-

Adopting multiple timeframes of moving averages can get better trading opportunities in oscillating markets.

Risks

-

Large fluctuations in short-term operations may lead to consecutive stop loss.

-

Improper CCI parameter settings may increase false signals.

-

During range-bound and consolidation periods, this strategy may encounter multiple small losses.

-

Only suitable for short-term frequent traders, not suitable for long-term holding.

Corresponding risk mitigation measures include: optimizing CCI parameters, adjusting stop loss position, adding FILTER conditions, etc.

Optimization Directions

-

Different combinations of EMA lengths can be tested to optimize parameters.

-

Other indicators or filter conditions can be added to filter out some false signals, such as MACD, KDJ etc.

-

Use dynamic trailing stop loss to control single loss.

-

Combining higher timeframe trend indicators can avoid trading against the trend.

Conclusion

Overall, this is a typical short-term oscillation strategy that uses the crossover of moving average lines combined with the overbought/oversold status of the CCI indicator to capture short-term reversal opportunities. This strategy is suitable for frequent short-term trading, but needs to withstand certain stop loss pressure. The stability and profitability of the strategy can be further improved through parameter optimization and adding filter conditions.

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-30 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//study(title="Strat CCI EMA scalping", shorttitle="EMA-CCI-strat", overlay=true)

strategy("Strat CCI EMA scalping", shorttitle="EMA-CCI-strat", overlay=true)

- 1