Recursive Momentum Trading Strategy

Overview

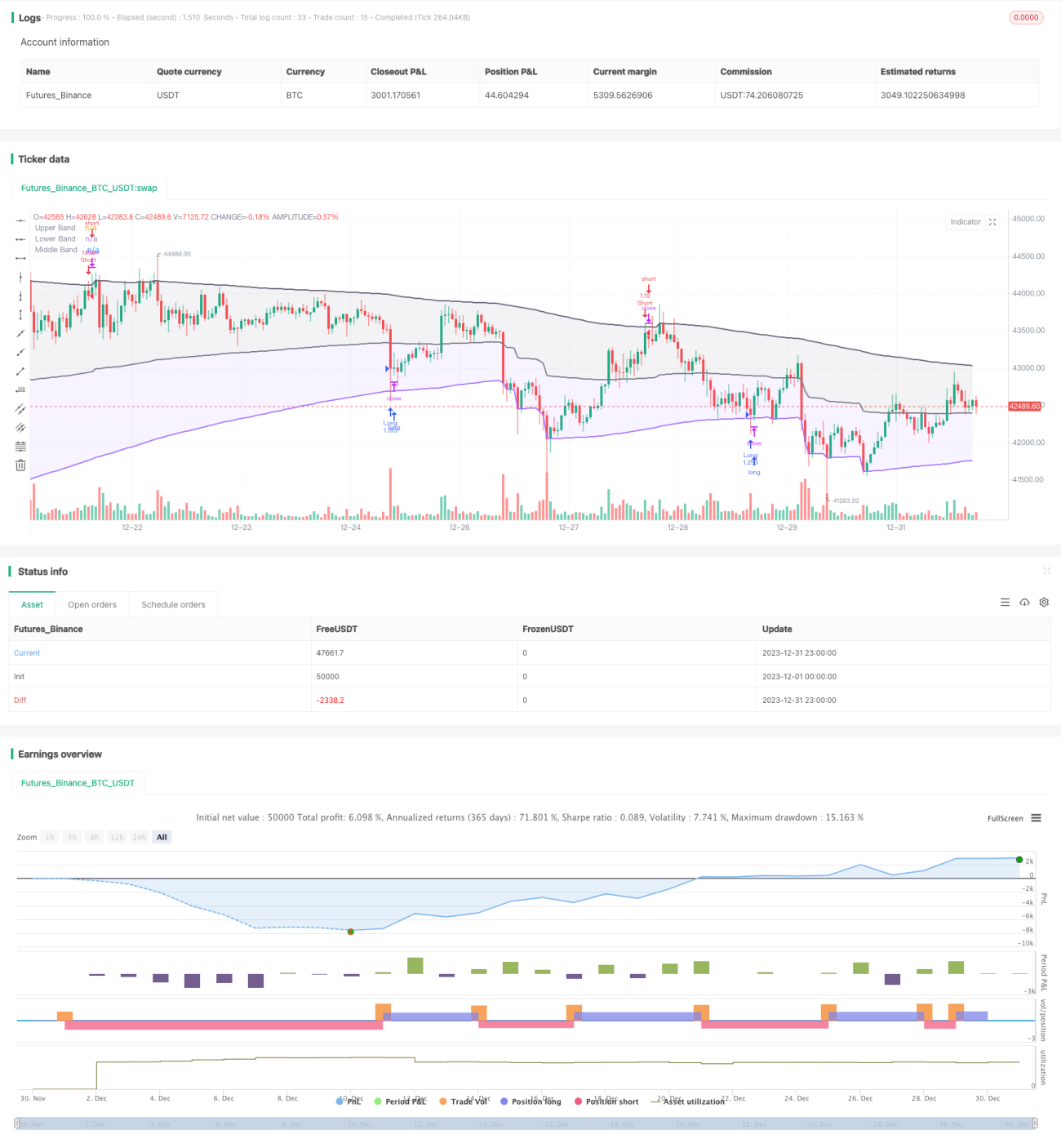

This strategy is a trend-following and breakout strategy based on the Recursive Bands indicator developed by alexgrover. It uses the Recursive Bands indicator to determine price trends and key support/resistance levels, combined with momentum conditions to filter out false breakouts, achieving low-frequency but high-quality entry signals.

Strategy Logic

Recursive Bands Indicator Calculation

The Recursive Bands indicator consists of an upper band, lower band and middle line. The indicator is calculated as:

Upper Band = Max(Previous bar's upper band, Close price + nVolatility)

Lower Band = Min(Previous bar's lower band, Close price - nVolatility)

Middle Line = (Upper Band + Lower Band)/2

Here n is a scaling coefficient, and volatility can be chosen from ATR, standard deviation, average true range or a special RFV method. The length parameter controls the sensitivity, larger values make the indicator trigger less frequently.

Trading Rules

The strategy first checks if the lower band and upper band are trending in the same direction to avoid false breakouts.

When price breaks below the lower band, go long. When price breaks above the upper band, go short.

In addition, stop loss logic is implemented.

Advantage Analysis

The advantages of this strategy are:

- Efficient indicator calculation using recursive framework, avoiding repeated computation

- Flexible parameter tuning to adapt to different market regimes

- Combining trend and breakout, avoiding false breakouts

- Momentum condition filters ensure signal quality

Risk Analysis

There are also some risks with this strategy:

- Improper parameter settings may lead to overtrading or poor signal quality

- May face large losses when major trend changes

- Insufficient slippage control in extreme moves may amplify losses

These risks can be managed by parameter optimization, implementing stop loss, increasing slippage threshold etc.

Optimization Directions

Some directions to optimize the strategy further:

- Incorporate indicators across multiple timeframes for robustness

- Add machine learning module for adaptive parameter optimization

- Conduct quantitative correlation analysis to find optimal parameter combinations

- Use deep learning to forecast price paths and improve signal accuracy

Conclusion

In summary, this is a very practical and efficient trend-following strategy. It combines the recursive framework for computational efficiency, uses trend support/resistance to determine major trends, adds momentum conditions to filter false breakouts and ensure signal quality. With proper parameter tuning and risk control, it can achieve good results. Worthy of further research and optimization to adapt to more complex market regimes.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=5

// Original indicator by alexgrover

strategy('Extended Recursive Bands Strategy', overlay=true, commission_type=strategy.commission.percent,commission_value=0.06,default_qty_type =strategy.percent_of_equity,default_qty_value = 100,initial_capital =1000)

length = input.int(260, step=10, title='Length')- 1