Extreme version of Noro's Trend Moving Averages Strategy

Overview

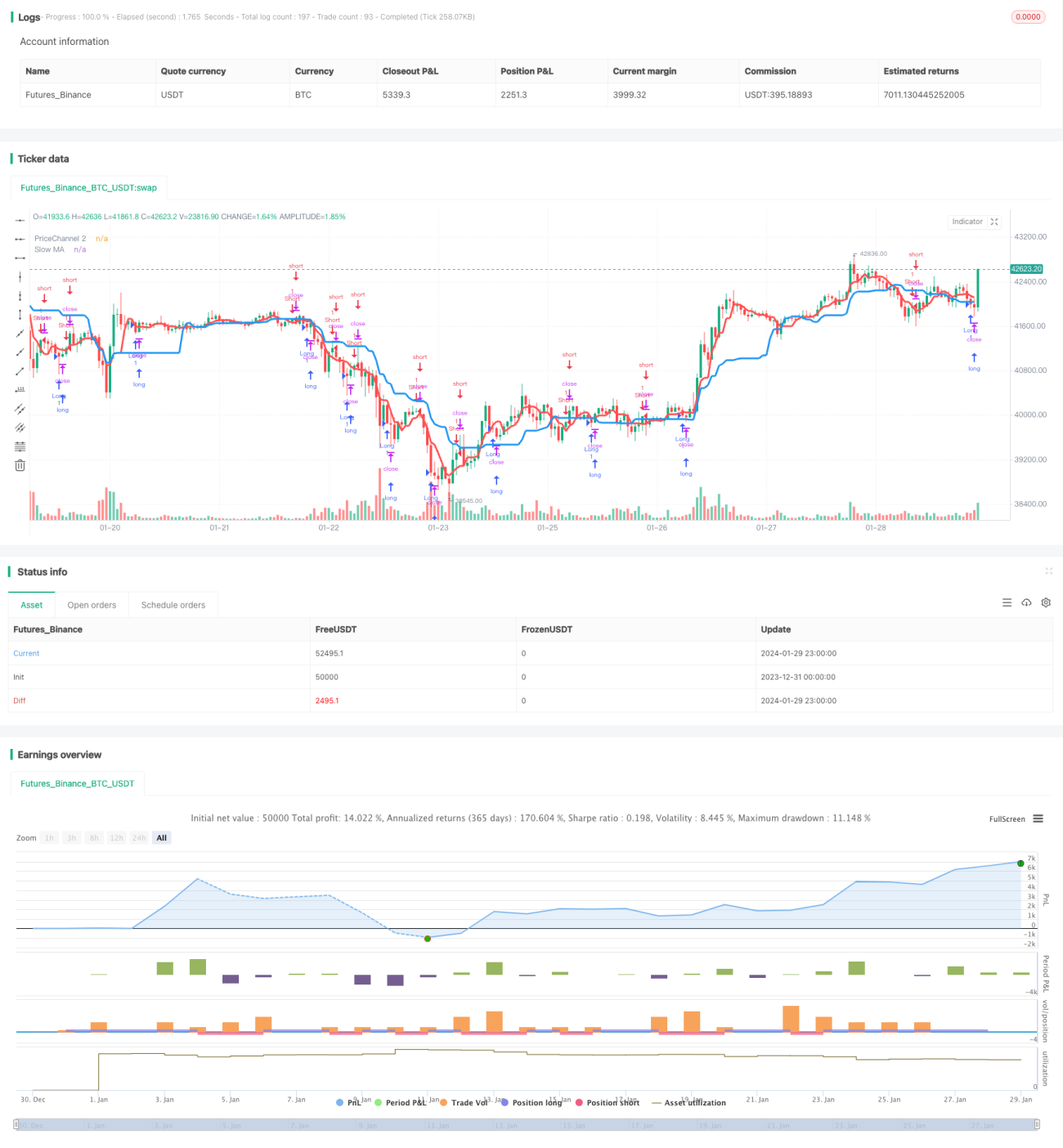

This strategy uses two moving average indicators to identify trend direction and long/short opportunities. The slower moving average (blue line) is used to determine the overall trend direction, while the faster moving average (red line) combined with the price channel is used to discover trading opportunities.

Strategy Logic

-

Calculate two moving averages - a slower MA with period 21 to determine the overall trend, and a faster MA with period 5 that combines with price channel to find trading opportunities.

-

Check if the current price breaks through the price channel formed in the previous period. A breakout signals a potential trading opportunity.

-

Count the number and direction of recent candlesticks. For example, several consecutive bearish candlesticks may signal a long opportunity, while consecutive bullish candlesticks may signal a short opportunity. The number of candlesticks is configurable via the Bars parameter.

-

Combine all the above factors to generate long/short signals. A signal is triggered when price move aligns with slower MA trend direction, fast MA or price channel produces signal, and candlestick move matches condition.

Advantages

-

The dual moving average system effectively tracks trend direction.

-

Faster MA and price channel combined detects early breakout points to catch trading opportunities.

-

Also considers candlestick direction and counts to avoid being trapped by market reversals.

-

Customizable MA parameters work for different products and timeframes.

Risks and Mitigations

-

Dual MAs can produce false signals during sideways markets. Can add oscillators or ATR to avoid trading choppy markets.

-

Still risks getting trapped in exceptional market moves. Can set proper stop loss to limit downside.

-

Impossible to fully avoid reversals. Will keep improving logic and parameters to make strategy more robust.

Enhancement Opportunities

-

Add supporting indicators like ADX, MACD to avoid wrong trades in choppy markets.

-

Dynamic stop loss calculation, e.g. based on ATR and risk preference.

-

Parameter optimization via machine learning for adaptive capability.

-

Fine tune parameters based on instrument characteristics, e.g. shorter periods for crypto.

Conclusion

Overall this strategy works very well in tracking trending markets, with additional breakout opportunities. With proper enhancements it can be made into a commercially viable high quality quant strategy. We will continue improving it to trade more markets stably.

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title = "Noro's Trend MAs Strategy v1.9 Extreme", shorttitle = "Trend MAs str 1.9 extreme", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

//Settings- 1