Cross-Timeframe Momentum Tracking Strategy

Overview

This strategy combines the 123 reversal and MACD indicators to achieve cross-timeframe momentum tracking. The 123 reversal determines short-term trend reversal points, and the MACD determines medium- and long-term trends. The combination generates long/short signals that lock in medium- and long-term trends while capturing short-term reversals.

Strategy Logic

The strategy consists of two parts:

-

123 reversal part: it generates buy/sell signals when the last two candlesticks form a peak/trough AND the Stochastics oscillator is below/above 50.

-

MACD part: it generates buy signals when the MACD line crosses above the signal line, and sell signals when it crosses below.

The final signal is triggered when both parts agree on the direction of the trade.

Advantage Analysis

The strategy combines short-term reversals and medium- to long-term trends, allowing it to lock in trended moves. This improves win rates, especially in ranging markets where the 123 reversal helps filter out noise.

Parameters can also be tuned to balance reversal and trend signals for different market conditions.

Risk Analysis

The strategy has some time lag, especially with longer MACD periods, which may cause missing short-term moves. Reversals also have some degree of randomness, leading to whipsaws.

Shortening the MACD period or adding stops can help control risks.

Optimization Directions

Possible ways to optimize the strategy:

-

Tune 123 reversal parameters to improve reversals.

-

Tune MACD parameters to improve trend identification.

-

Add filters with other indicators to improve performance.

-

Add stop loss to control risks.

Conclusion

The strategy combines parameters across timeframes along with multiple technical indicators for cross-timeframe momentum tracking, balancing the pros of reversal and trend-following strategies. Parameter tuning and more indicators or stops can further optimize it. The concept has great potential.

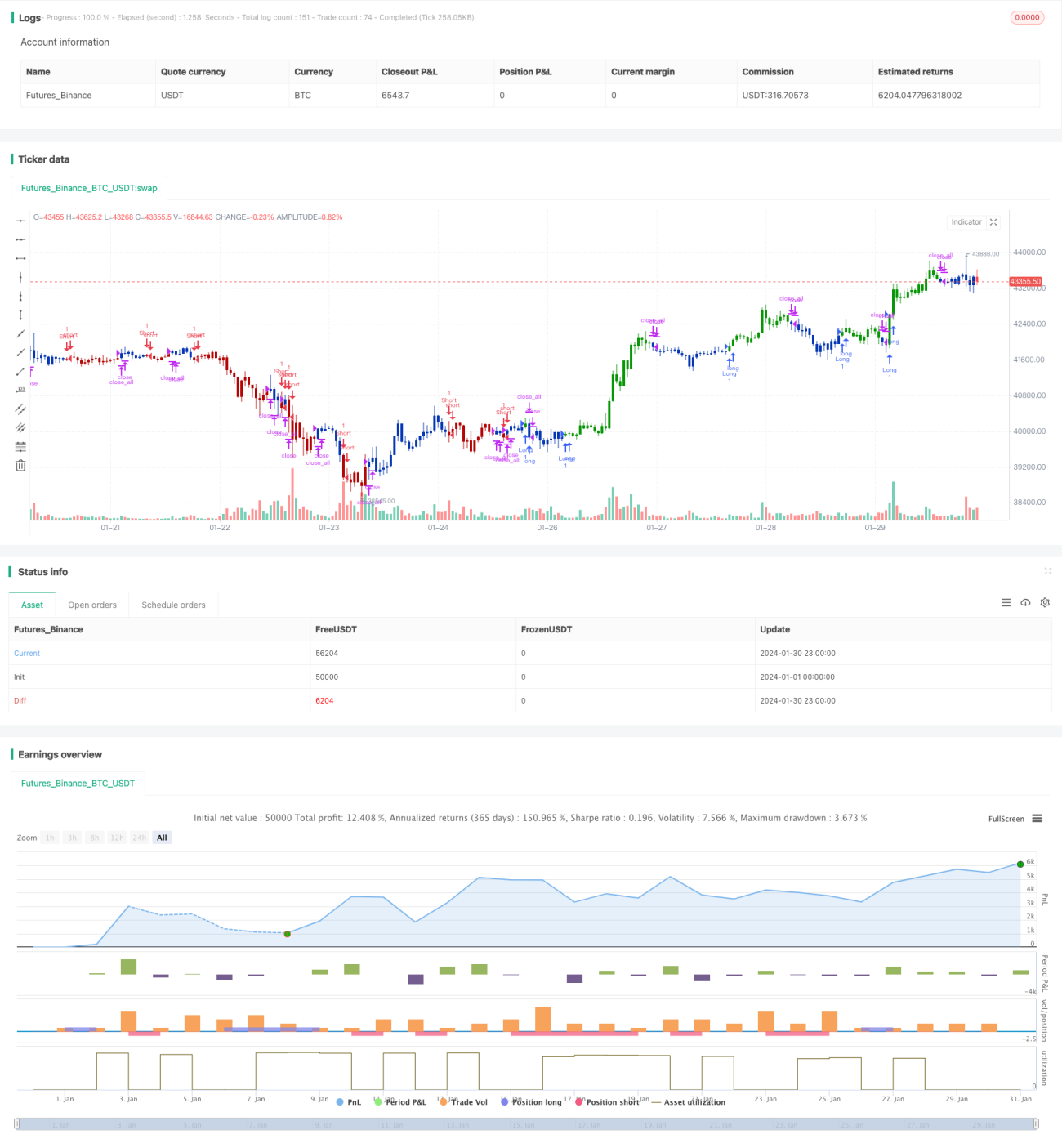

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1