Breakback Storm Strategy in Hidden Opportunities

Overview

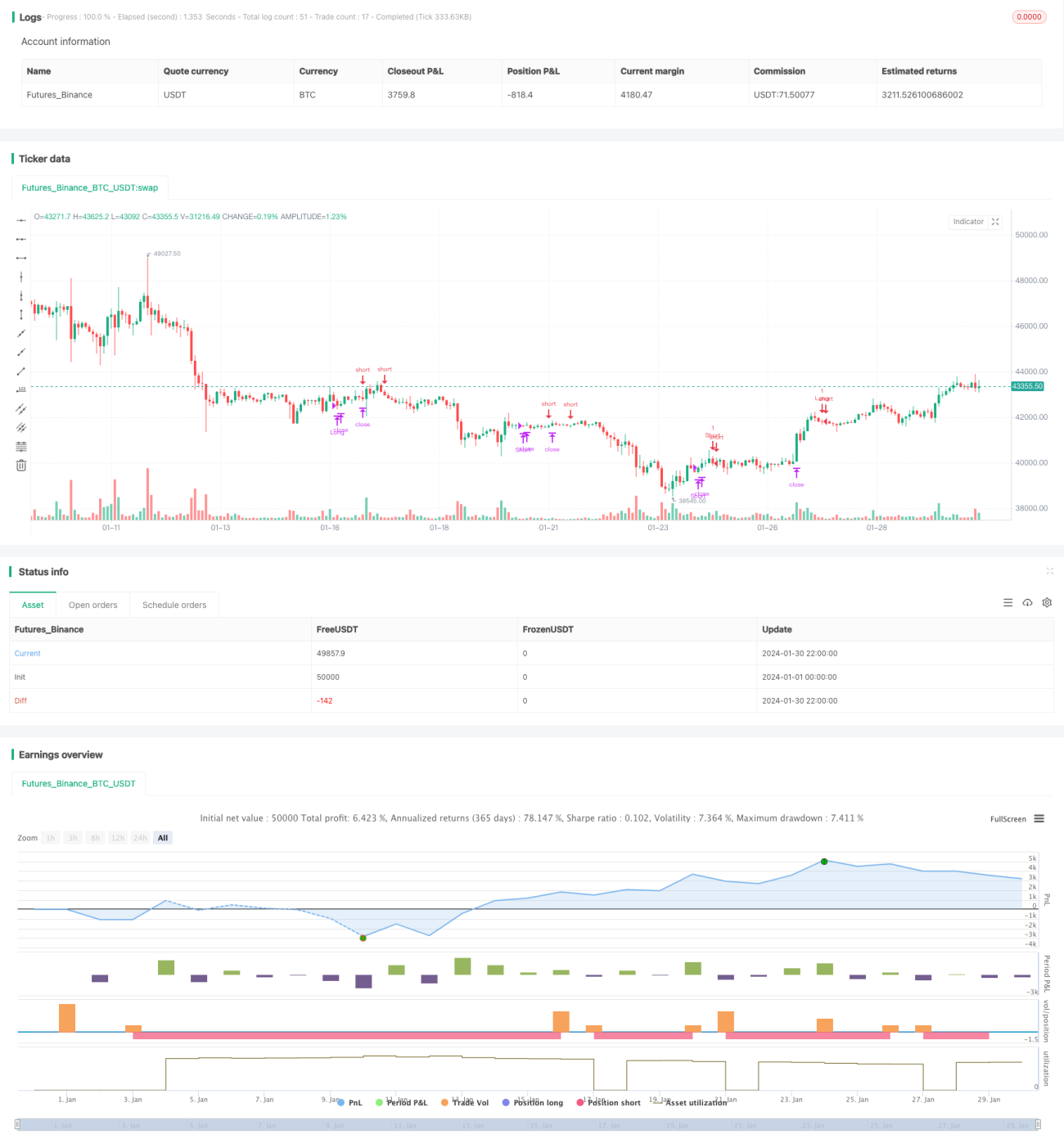

The Breakback Storm strategy specializes in capturing pullback opportunities after price breakouts to seize hidden explosive moves within short-term reversals. It combines trend determinations and reversal signals to go long after upward breakouts when prices pull back to previous support levels, and go short after downward breakouts when prices bounce back to previous resistance levels. The strategy filters out most false breakouts through strict breakout validations, ensuring high quality entries.

Strategy Logic

The strategy is based on two main triggers: recent high/low breakouts on the long-term timeframe and pullback patterns on the short-term. Specifically, it first requires prices to break above the 80-period high to determine an upward trend from the higher timeframe. Secondly, it demands prices to break the previous day's high to confirm a short-term upward breakout. The long signal then triggers when prices close below the previous day's low after the breakout.

The short signal works symmetrically, requiring a recent low breakout plus a bounce back to the previous day's high. This combination ensures the quality of trend direction and timing of entry points, capturing most of the trend while avoiding middles.

Advantage Analysis

This strategy combines dual directional trading and breakout concepts with significant edges:

- Breakout filter ensures directional accuracy

- Pullback entry ensures risk-reward

- Timed exit balances profit and risk

Specifically, the 80-period filter avoids most false breakouts on short-term noise. Breaking the previous day's extreme points reliably catches short-term trend evolutions. Such quality signals ensure directional accuracy of trades.

The pullback entry giving certain stop loss buffer then captures most of the trend middle part afterwards. This guarantees profitable stability of the strategy.

Finally, the timed exit mechanism also balances both profitability and risk control factors by predefining outcome scenarios, minimizing emotional interference.

Risks and Solutions

However, some risks exist in this strategy:

- Concentrated entry timing causes crowding

- Frequent long/short switches increase costs

- Insufficient reversal magnitude to profit

The first risk comes from the pullback entry setting. When concurrent uptrend and downtrend waves appear in the market, entry signals on both sides can crowd, preventing entries on either side.

This can be avoided by adjusting the exit filters and setting minimum breakout ranges to space out signals.

The second risk relates to whipsaws from frequent reversals. Excessive long/short switches increase costs and actual losses.

This can be reduced by tuning the holding period and stop loss parameters to minimize unnecessary exits.

Finally, the ensuing reversal momentum may also lack enough magnitude within consolidation ranges at times. Additional long-term trend metrics can help avoid low quality setups.

Optimization Directions

Based on the analysis, further optimizations include:

- Adding profit taking mechanisms

- Incorporating volatility metrics

- Considering seasonal opportunities

Moving profit stops or break-even stops can first lock in profits and avoid retracements.

Volatility indicators like ATR and RVI can also gauge oscillation regimes to avoid low-opportunity periods.

Finally, cyclic trends around seasonal shifts also provide larger trend spaces to minimize side effects.

Conclusion

Overall, the Breakback Storm strategy aims to capture short-term trend reversal opportunities after trend breakouts. By combining long-term trend filters, short-term reversal signals, breakout validations and pullback entries, it provides a robust framework to trade pullbacks within larger trend moves. When optimized with appropriate profit taking, volatility metrics and seasonal filters, such framework can generate stable profits across various market conditions.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Smash Day Pattern (Type B)", overlay=true, default_qty_type = strategy.fixed, default_qty_value = 1, initial_capital = 10000)

in1 = input(40, "Max Days to Hold") - 1

- 1