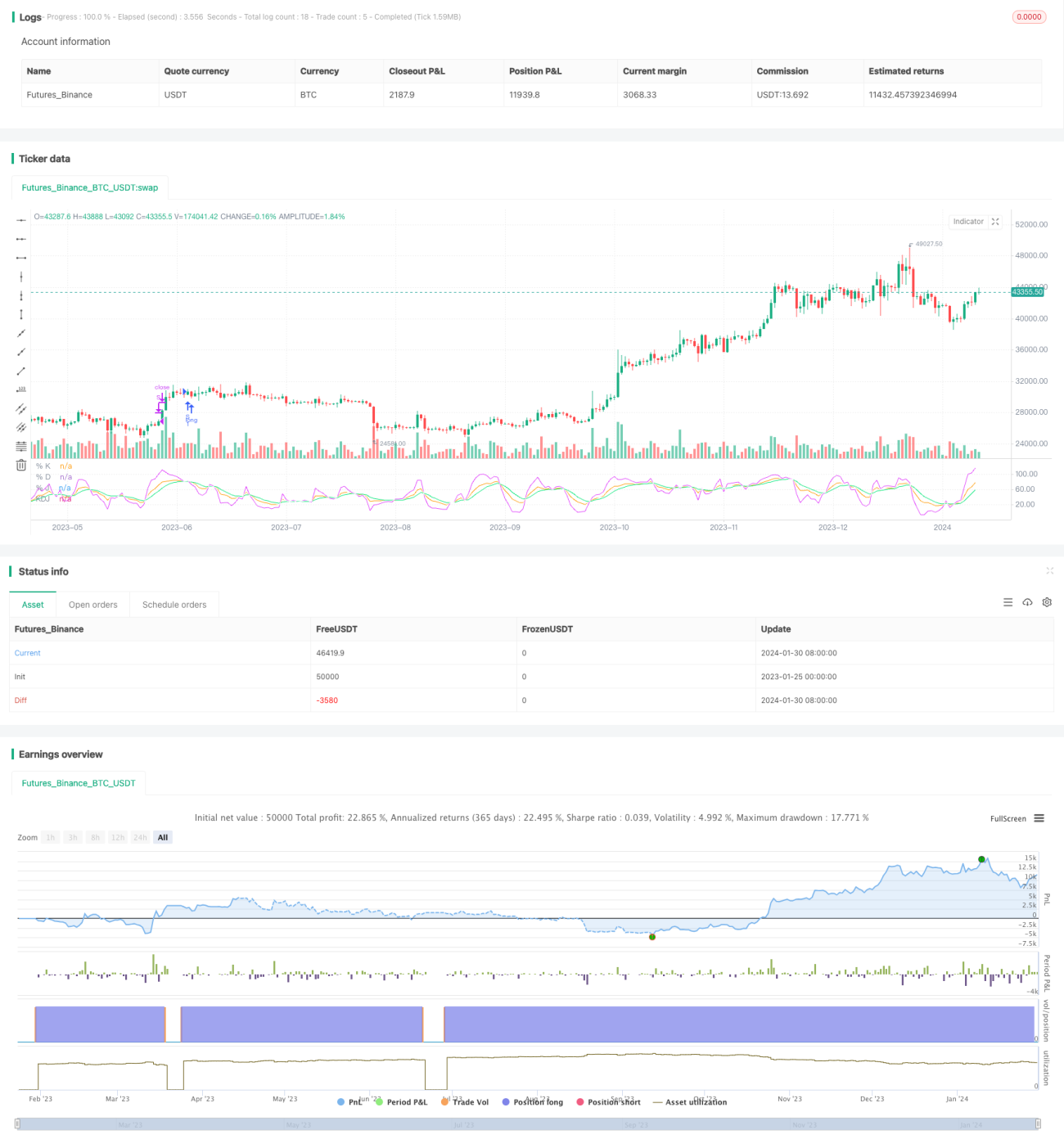

KDJ Golden Cross Long Entry Strategy

Overview

The KDJ Golden Cross Long Entry Strategy is a quantitative trading strategy based on the KDJ indicator. This strategy mainly uses the golden cross of the J line and D line of the KDJ indicator to generate buy signals and goes long when the J line crosses above the D line. The strategy is relatively simple and easy to implement, suitable for beginners of quantitative trading.

Strategy Logic

The main technical indicator used in this strategy is the KDJ indicator. KDJ indicator consists of the K line, D line and J line. Where:

K = (Current Close - Lowest Low over the past N days) ÷ (Highest High over the past N days - Lowest Low over the past N days) x 100;

D = M-day moving average of K;

J = 3K - 2D.

According to the KDJ indicator rules, when J line crosses above D line, it indicates that prices are reversing upward and long positions can be taken; when J line falls below D line, it signals that prices are reversing downward and short positions can be initiated.

This strategy utilizes the above rules and generates buy signals when the J line crosses above the D line, i.e. a golden cross forms, to go long. The exit signal is when J goes above 100 to close long positions.

Advantages

-

Using the KDJ indicator to determine entry timing which incorporates price up and down movements, thus more reliable.

-

The strategy has clear and simple signal rules which are easy to understand and implement, suitable for beginners.

-

Adopted stop profit and stop loss to effectively control risks.

-

Large room for parameter optimization and flexible implementation.

Risks

-

KDJ indicator tends to generate false signals leading to losses.

-

Market short-term adjustments after buying may trigger stop loss exiting and miss major trends.

-

Improper parameter settings may lead to overtrading or unclear signals.

-

Need to consider transaction costs' impact on overall profitability.

Main risk management methods: Optimize parameters properly, track indexes to enhance, appropriately expand stop loss range, etc.

Optimization Directions

-

Optimize parameters of KDJ to find best parameter combinations.

-

Add filtering conditions to avoid false signals. Can combine other indicators or formations for filtration.

-

Can choose different parameter settings based on market types (bull or bear markets).

-

Can appropriately expand stop loss range to reduce the probability of stop loss exits.

-

Can combine trading volume and other indicators for analysis to avoid being trapped.

Summary

The KDJ Golden Cross Long Entry Strategy is relatively simple and practical overall, easy for beginners to get started and implement. The strategy has certain trading advantages but also has some risks. It needs targeted optimization in order to fully realize the strategy value. Overall, the strategy deserves key research and application.

- 1