Dynamic Moving Average Crossover Strategy

Overview

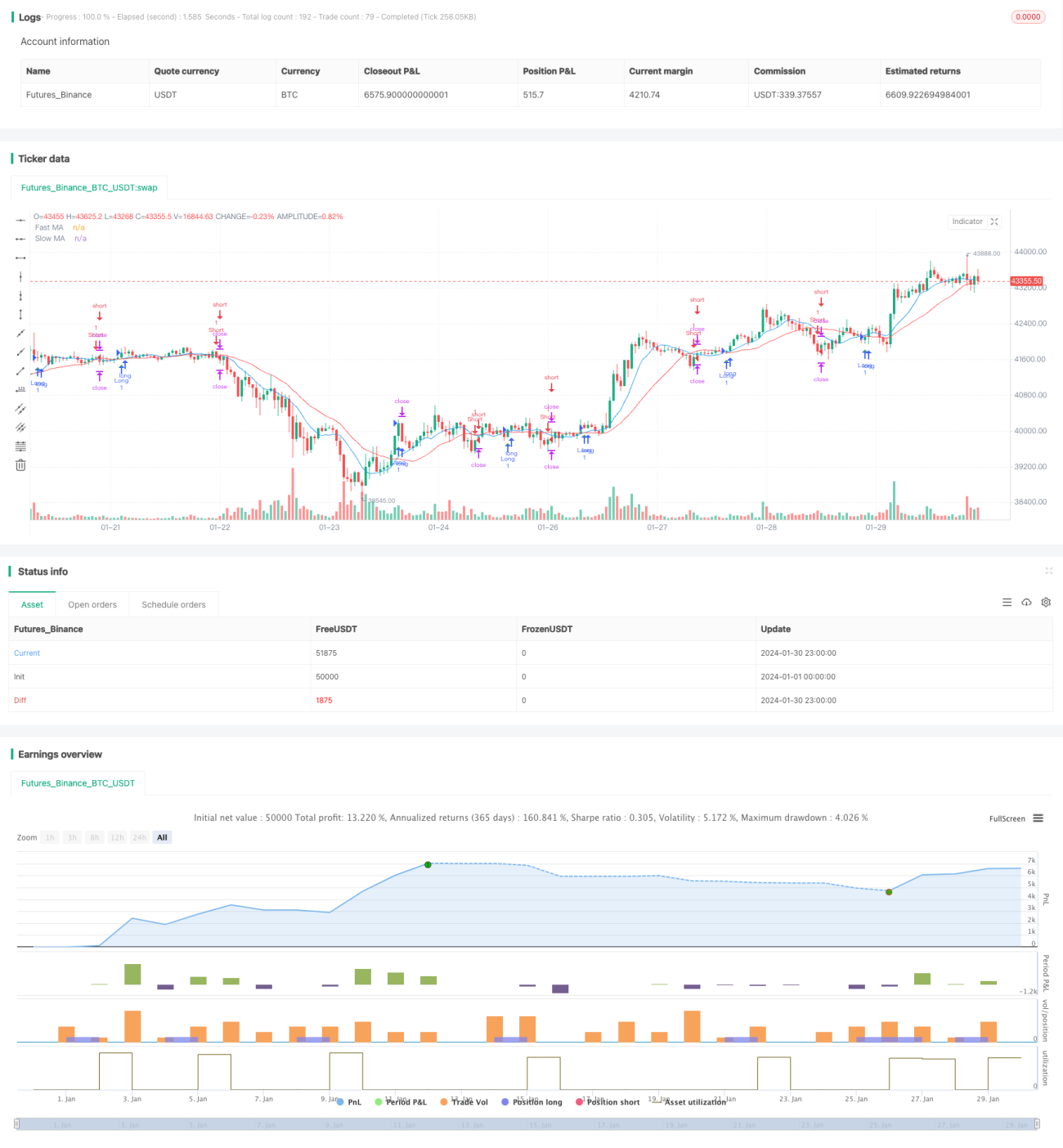

The Dynamic Moving Average Crossover Strategy is a typical trend-following strategy. It generates buy and sell signals by calculating the fast moving average (Fast MA) and slow moving average (Slow MA) and detecting crosses between them to capture trend reversal points in the market.

Strategy Logic

The core logic of this strategy is: when the fast moving average crosses above the slow moving average from below, a buy signal is generated; when the fast moving average crosses below the slow moving average from above, a sell signal is generated.

Moving averages can effectively filter market noise and capture price trends. The fast moving average is more sensitive and can timely capture changes in the trend; the slow moving average is more stable and can effectively filter out the impact of short-term fluctuations. When the fast and slow MAs have a golden cross (moving up from below), it indicates that the market has entered a bullish phase; when they see a death cross (moving down from above), it indicates that the market has entered a bearish phase.

This strategy will immediately issue trading signals when the moving averages cross, adopt a trend-chasing strategy to follow market trends and earn bigger profits. At the same time, the strategy sets stop loss and take profit to strictly control risks.

Advantage Analysis

- Good backtest performance of the strategy, capturing big moves by following trends

- Clear signals generated by moving average crosses, easy to implement

- With stop loss and take profit to strictly control risks

Risk Analysis

- Prone to signal errors and suffering severe losses

- High trading frequency, short holding periods

- Need reasonable parameter settings

Improvements can be made by optimizing parameters, adjusting the moving average periods, adding filter conditions etc.

Optimization Directions

- Adjust moving average parameters to find optimal parameter combinations

- Add momentum indicators etc. as filters to reduce false signals

- Optimize stop loss and take profit settings

- Combine other indicators to determine trend direction

Conclusion

The Dynamic Moving Average Crossover Strategy overall performs quite well. Further improvements can be made by optimizing parameters. The strategy is easy to implement and suitable for beginner's practice. But the risk of false signals should be watched out for, and needs to be used together with other indicators to perform better.

- 1