Ichimoku Cloud Trend Following Strategy

I. Strategy Name: Ichimoku Cloud Trend Following Strategy

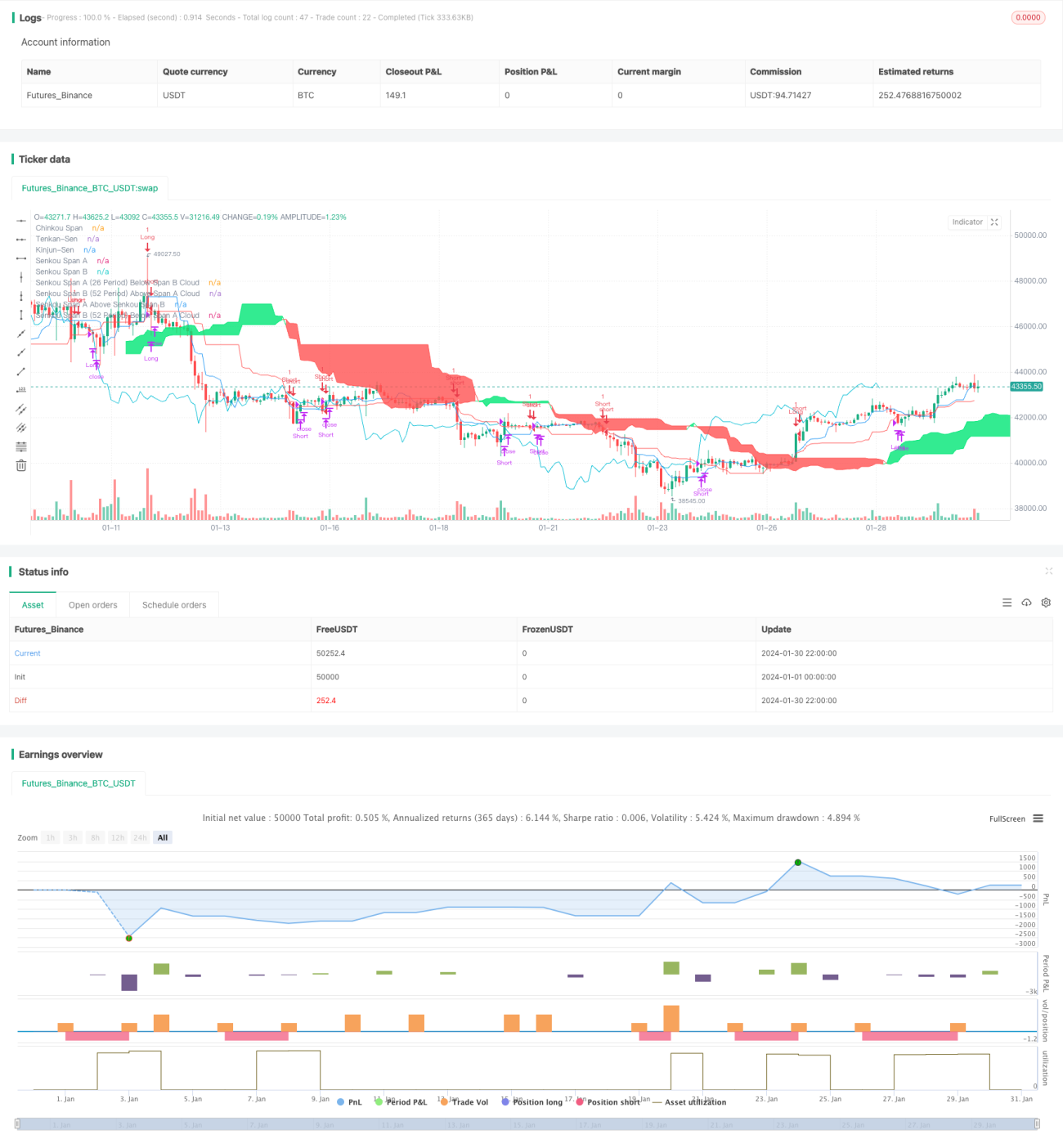

II. Strategy Overview

This strategy utilizes multiple Ichimoku Cloud signals to design a pure trend following strategy that aims to capture mid-to-long term trends, filter out consolidations, and follow strong trend directions.

III. Strategy Principle

This strategy mainly uses Tenkan-sen, Kijun-sen, Chikou Span and other key indicators from the Ichimoku Cloud. For judging long term trends, it focuses on the relationship between leading and lagging Span; for specific entry and exit timings, it looks at Tenkan-sen and Kijun-sen crossovers and price relationship changes with the Cloud.

In summary, the core logic is: confirm mid-long term trend -> wait for strong trend resumption signals -> enter to follow trends -> exit with trailing stop loss.

Specifically, to determine mid-long term trend, it uses the relationship between leading and lagging Span (above leading green Span signaling upward trend and vice versa). After confirming the bigger trend, crossover between Tenkan-sen and Kijun-sen along with price breakout signals are used to identify trend resumption; after entry, Kijun-sen is used as trailing stop loss for exits.

This filters out short-to-mid term consolidations and allows capturing strong trends for consistent outperformance in markets.

IV. Advantages

(1) Using Ichimoku Cloud to determine mid-long term trend direction is beneficial for locating major directional edges.

(2) Tenkan-sen/Kijun-sen crossovers and price relationship changes with the Cloud allow effectively filtering out consolidations and capturing strong trends early.

(3) Trailing stop loss exit mechanism allows riding big trends while also controlling isolated losses effectively.

(4) Combining various Ichimoku signals creates a robust system following trends smoothly.

V. Risks

(1) Systemic risk of misidentifying bigger trend. If the bigger trend is diagnosed wrong, all subsequent actions would carry erroneous directional risk.

(2) Risk from poorly chosen entry timing. Inappropriate entry timing risks adverse price whipsaws.

(3) Risk from stops placed too tightly. Extreme price moves could take out stops that are too tight resulting in unplanned losses.

(4) High trading frequency leading to excessive transaction costs. Bad parameter tuning could lead to excessive trade frequency and costs.

VI. Enhancement Areas

(1) Test different combinations of Ichimoku input periods to find optimum parameters.

(2) Optimize entry filters to ensure high quality entries.

(3) Adjust stop distance to balance risk-reward.

(4) Add profit target levels based on price-key indicator distances to create adaptive profit taking mechanisms.

VII. Conclusion

This Ichimoku Cloud trend following strategy synthesizes multiple Ichimoku signals to diagnose trend, time entries, and trail stops. Practice shows it can effectively capture mid-long term trends, filter out consolidations and achieve consistent outperformance. Future optimization and testing could further improve performance for superior returns.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Ichimoku trendfollowing", overlay=true, initial_capital=1000, commission_type=strategy.commission.cash_per_order, commission_value=0.04, slippage=2)

//***************************- 1