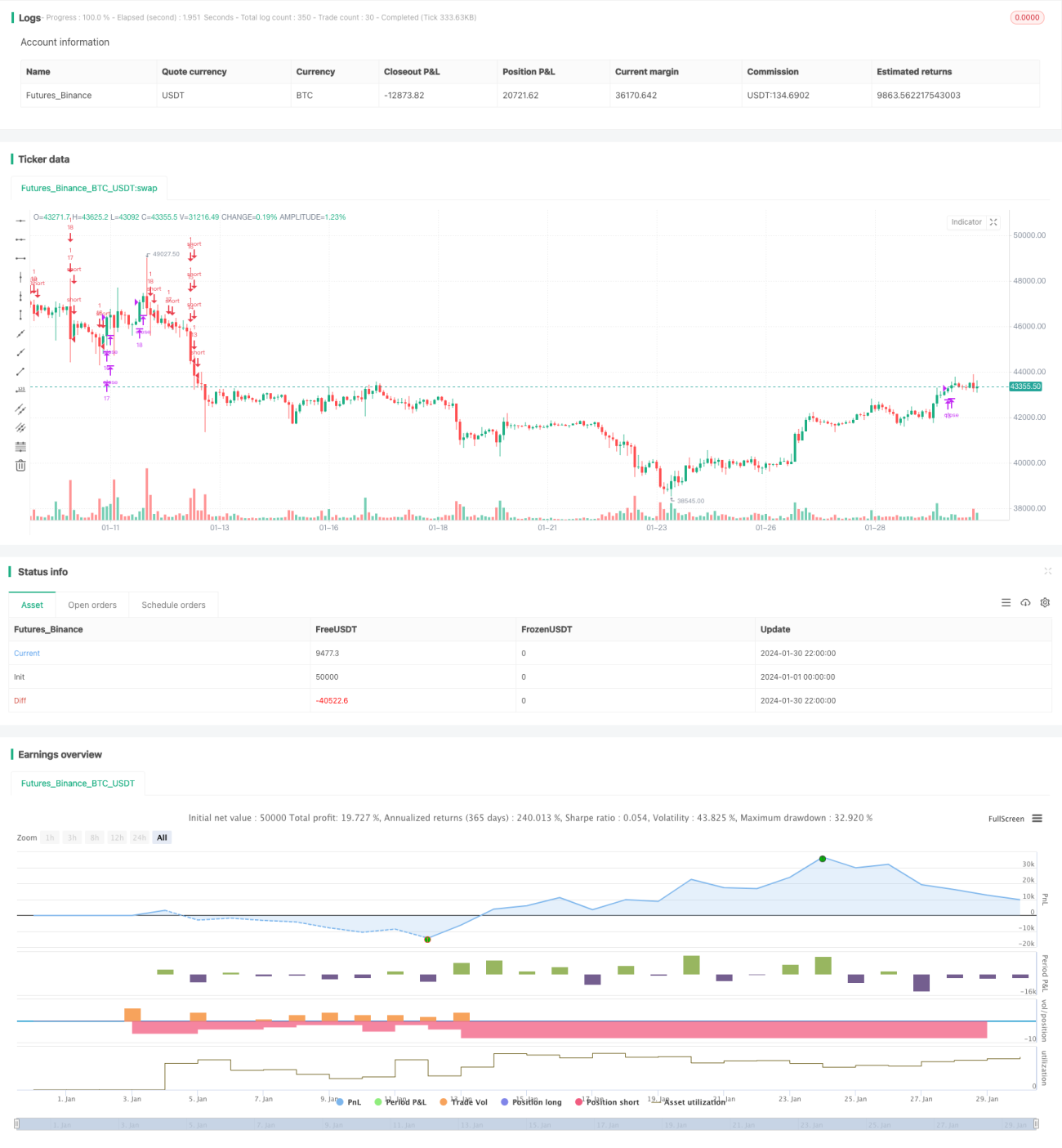

概述

本策略是一个基于K线实时变化的双向追踪网格交易策略。它可以在牛市和熊市中都获得稳定的利润。

策略原理

-

根据用户设置的网格数量,自动计算价格网格区间和每个网格价格。

-

当价格突破网格价格时,按照固定数量开仓做多;当价格跌破网格价格时,平仓做多仓位,做空开仓。

-

这样,价格在网格区间震荡时,可以通过追踪价格变化来获得利润。

优势分析

-

自动计算合理的网格区间,无需人工确定支持阻力。

-

双向交易,可适应行情多变的市场环境。

-

固定开仓数量,有利于风险控制。

-

代码直观简洁,容易理解和修改。

风险分析

-

行情剧烈波动可能导致亏损扩大。

-

交易费用的累积也会影响最终利润。

-

需要合理确定网格数量,太多网格交易次数增多但每次利润有限。

优化方向

-

加入止损策略,避免亏损扩大。

-

增加网格数量动态调整功能。

-

考虑加入杠杆,放大交易量。

总结

本策略整体思路清晰简洁,通过双向追踪网格交易获得稳定收益,同时也存在一定的交易风险。通过不断优化,可望获得更好的效果。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1