Lazy Bear Squeeze Momentum Strategy

Overview

The Lazy Bear Squeeze Momentum strategy is a quantitative trading strategy that combines Bollinger Bands, Keltner Channels and a momentum indicator. It utilizes Bollinger Bands and Keltner Channels to determine if the market is currently in a squeeze, then uses a momentum indicator to generate trading signals.

The main advantage of this strategy is being able to automatically identify the start of trending moves and determine entry timing with the momentum indicator. However, there are also certain risks that need to be addressed through optimization across different products.

Strategy Logic

The Lazy Bear Squeeze Momentum strategy makes judgements based on the following three indicators:

- Bollinger Bands: Includes middle band, upper band and lower band

- Keltner Channels: Includes middle line, upper line and lower line

- Momentum Indicator: Current price minus price n days ago

When the Bollinger upper band is below the Keltner upper line and the Bollinger lower band is above the Keltner lower line, we determine the market is in a squeeze. This usually implies a trending move is about to start.

To pinpoint entry timing, we use the momentum indicator to gauge the speed of price changes. A buy signal is generated when momentum crosses above its moving average, and a sell signal when momentum crosses below its moving average.

Advantage Analysis

The main advantages of the Lazy Bear Squeeze Momentum strategy:

- Automatically identify early entries into new trends

- Combination of indicators prevents false signals

- Captures both trend and mean-reversion

- Customizable parameters for optimization

- Robust across different products

Risk Analysis

There are also certain risks to the Lazy Bear Squeeze Momentum strategy:

- Probability of false signals from Bollinger & Keltner

- Momentum instability, missing best entries

- Poor performance without optimization

- High correlation to product selection

To mitigate risks, recommendations include: optimizing lengths for Bollinger & Keltner, adjusting stop loss, selecting liquid products, verifying signals with other indicators.

Optimization Directions

The main directions to further enhance performance:

- Test combinations of parameters across products and timeframes

- Optimize lengths for Bollinger Bands and Keltner Channels

- Optimize length of momentum indicator

- Different stop loss/take profit for longs and shorts

- Additional indicators for signal verification

Through rigorous testing and optimization, the strategy's edge and profitability can be greatly improved.

Conclusion

The Lazy Bear Squeeze Momentum strategy has strong signal generation through a multi-indicator approach, and can effectively identify new trend starts. But it also carries risks that necessitate optimization across trading instruments. With continual testing and enhancement, it can become a robust algorithmic trading system.

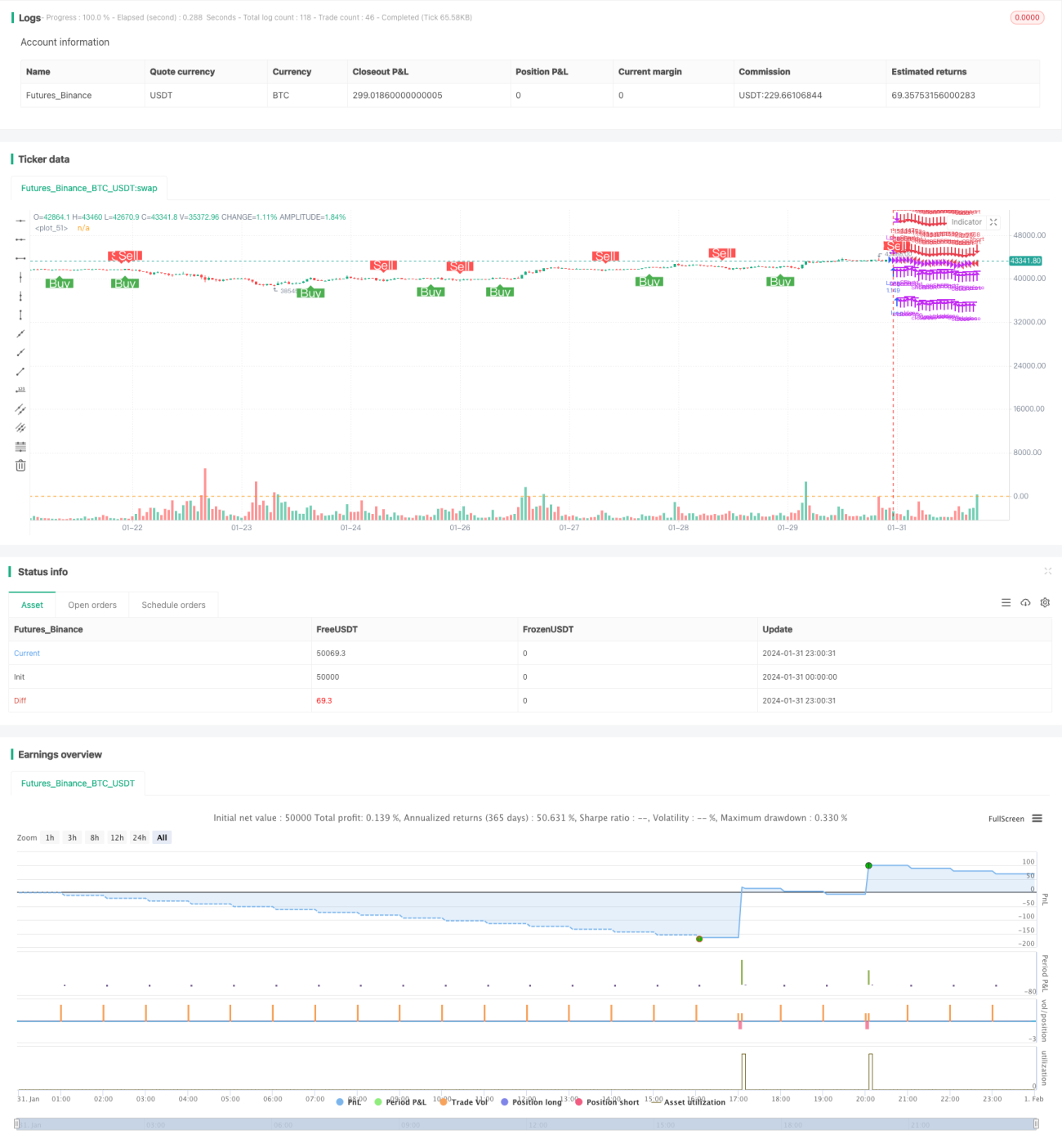

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1