Reversal Trend Catching and Dynamic Stop Loss Combo Strategy

Overview

This strategy combines a reversal trend catching strategy and dynamic stop loss strategy to capture reversal trends while controlling risks with dynamic stops.

Strategy Logic

Reversal Trend Catching Strategy

This strategy is based on K and D values of Stochastic Oscillator. It generates buy signals when price falls for two consecutive days while K rises above D. It generates sell signals when price rises for two days while K falls below D. This catches price reversal trends.

Dynamic Stop Loss Strategy

This strategy sets dynamic stop loss based on price volatility and skew. It calculates fluctuation of highest high and lowest low recently and judges if it is in a upper or down channel based on skew, then set dynamic stop price accordingly. This adjusts stop position based on market condition.

The two strategies work together to catch reversal signals and set dynamic stops to control risks.

Advantage Analysis

- Catch price reversal points, good for reversal trading

- Dynamic stops adjust with market environment

- Dual signal confirmation avoids false signals

- Control risks and ensure profits

Risk Analysis

- Reversal failure risk. Reversal signals may fail.

- Parameter risk. Wrong parameters may affect performance.

- Liquidity risk. Some products have poor liquidity to stop loss.

Risks can be controlled by parameter optimization, strict stop loss, choosing products with good liquidity.

Optimization Directions

- Optimize stochastic parameters for best combination

- Optimize stop parameters for best stop position

- Add filters to avoid opening on range markets

- Add position sizing to limit maximum loss

Comprehensive optimizations enable the strategy to catch reversals while controlling risks.

Summary

The strategy combines reversal trend catching and dynamic stops for stable short-term trading. With continuous optimization and monitoring, it has the potential for steady profits.

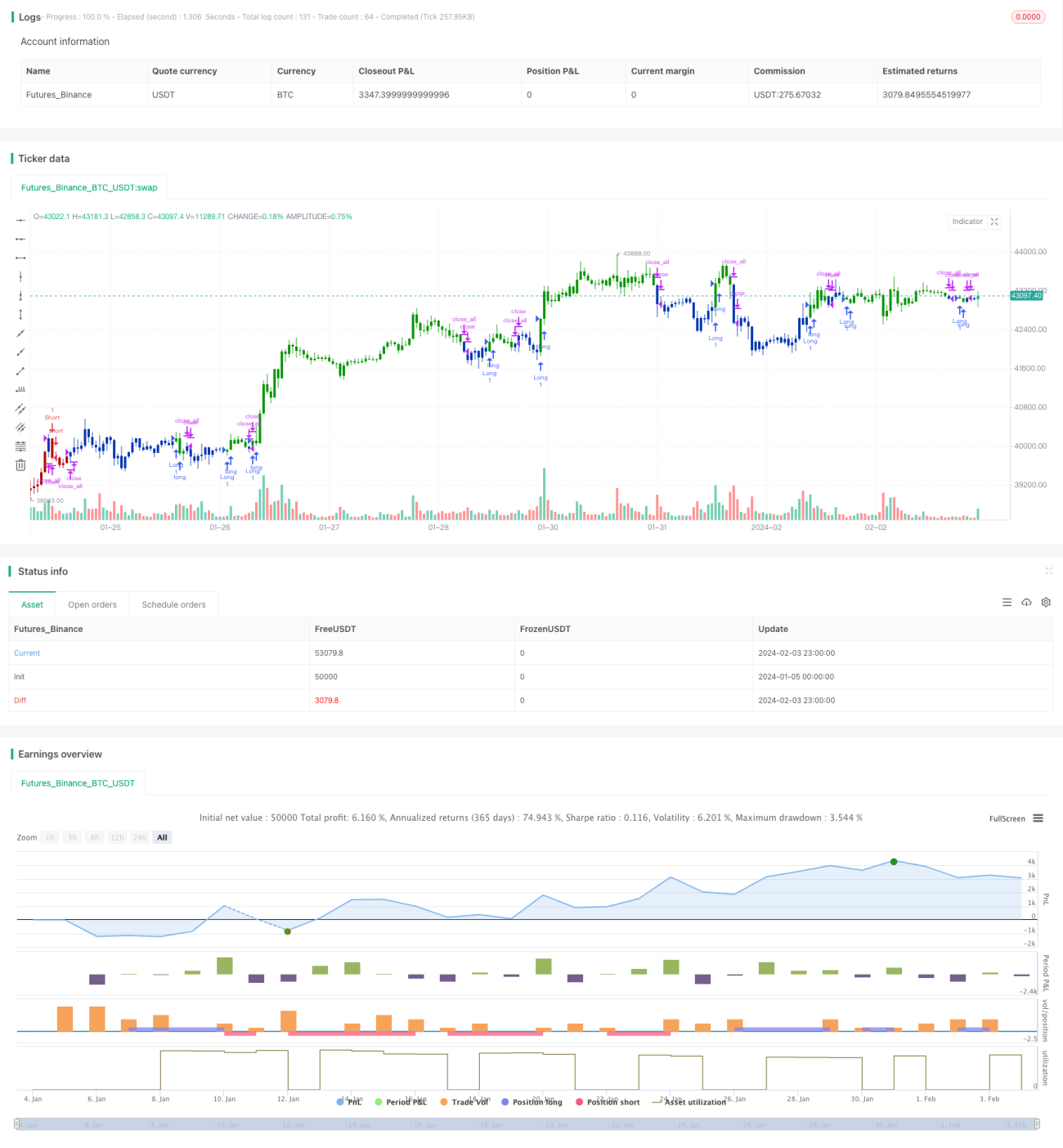

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/12/2020

// This is combo strategies for get a cumulative signal. - 1