Ichimoku Cloud, MACD and Stochastic Based Multi-Timeframe Trend Tracking Strategy

Overview

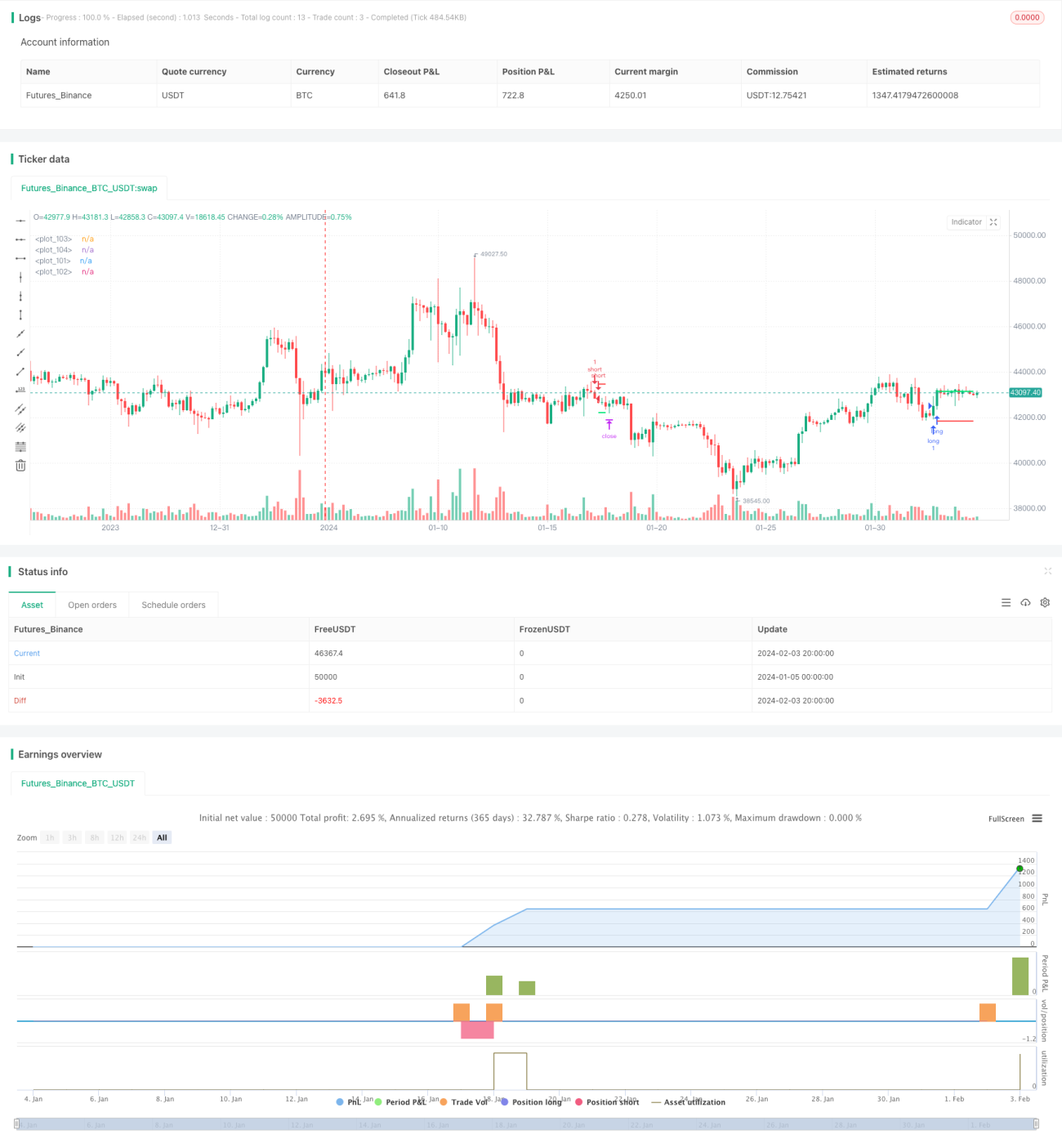

This strategy integrates Ichimoku Cloud, moving average, MACD, Stochastic and ATR indicators to identify and track trends across multiple timeframes. It adopts ATR-based stop loss and take profit methods for risk control after obtaining high probability trend signals.

Strategy Logic

-

Ichimoku Cloud judges medium and long term trend directions. The CLOSE price crossing above Ichimoku's turning line and baseline is a bullish signal, and crossing below them is a bearish signal.

-

MACD judges short-term trends and overbought/oversold situations. MACD histogram crossing above MACD signal line is a bullish signal, and crossing below is a bearish signal.

-

Stochastic KD judges overbought/oversold zones. K line crossing above 20 is a bullish signal, and crossing below 80 is a bearish signal.

-

Moving average judges medium-term trends. Close price crossing above MA is a bullish signal, and crossing below is a bearish signal.

-

Integrate signals from the above indicators to filter out some false signals and form high probability sustainable trend signals.

-

Use ATR to calculate stop loss and take profit price. Use a certain multiple of ATR as stop loss and take profit bits to control risks.

Advantages

-

Identify trends across multiple timeframes to improve signal accuracy.

-

Widely employ indicator combos to effectively filter out false signals.

-

ATR-based stop loss & take profit significantly limits per trade loss.

-

Customizable strictness of entry conditions caters to different risk appetites.

Risks

-

Trend following nature fails to detect reversals caused by black swan events.

-

Idealized ATR stop loss is hard to fully replicate in live trading.

-

Improper parameter settings may lead to overtrading or insufficient signal accuracy.

-

Parameter tweak is needed to fit different products and market environments.

Enhancement Areas

-

Introduce machine learning to aid judging trend reversal points.

-

Optimize ATR multiplier parameter values for different products.

-

Incorporate other factors like volume changes to improve breakthrough signal accuracy.

-

Keep optimizing parameters based on backtest results to find best parameter combinations.

Summary

This strategy leverages Ichimoku Cloud, MACD, Stochastic and more for multi-timeframe trend identification, capturing trends while avoiding being trapped by black swan events. The ATR-based stop loss & take profit effectively limits per trade loss. With more auxiliary judgments and machine learning methods introduced, this strategy has further optimization potential.

- 1