Super Trend Following Strategy Based on Moving Averages

Overview

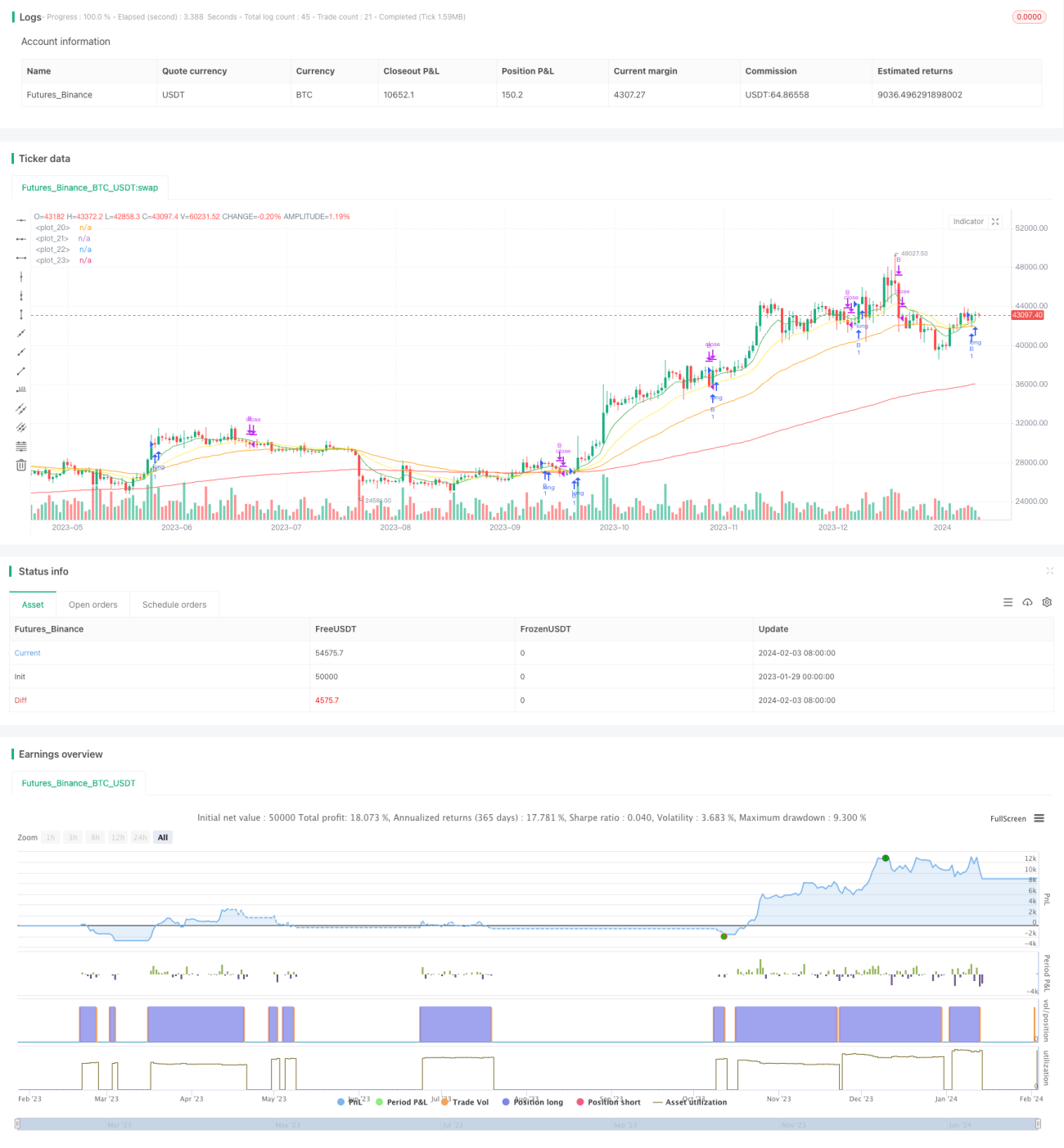

This strategy is a typical trend following strategy. It uses multiple sets of moving averages with different periods to determine the market trend. It enters the market when the trend is established and exits when the short-term trend reverses.

Strategy Principle

The strategy employs 4 groups of moving averages: 9-day, 21-day, 50-day and 200-day lines. They represent different timeframes respectively.

When the short-term moving average crosses over the long-term one upwards, it is determined that the market enters an uptrend. When it crosses downwards, the market is seen to be in a downtrend.

The strategy takes the 9-day MA as a reference to observe the alignment of the other MAs, thereby judging the overall trend direction. Specifically, the logic is:

Long entry conditions: Close > 9-day MA and 9-day MA > 21-day MA and 21-day MA > 50-day MA and 50-day MA > 200-day MA.

Short entry conditions: Close < 9-day MA and 9-day MA < 21-day MA and 21-day MA < 50-day MA and 50-day MA < 200-day MA.

Here the relationship between close price and 9-day MA determines the shortest-term trend, while that between 9-day and 21-day MA judges short-term trend, 21-day and 50-day medium-term trend, 50-day and 200-day long-term trend. Only when the relationships of all the four MA pairs conform can a valid trend be established to generate trading signals.

Exit conditions: close price crosses below 21-day MA, flatten all long positions; crosses above 21-day MA, flatten all short positions.

Advantages of the Strategy

-

Adopting multiple MAs to determine the trend can filter out market noises from non-mainstream moves and capture medium-to-long term trends.

-

Strict entry conditions require valid judgments across different timeframes, avoiding being trapped by short-term corrections.

-

Timely stop loss helps effectively control risks.

Risks and Solutions

-

In long-term rangebound markets, excessive false signals may occur and increase trading risks. This can be avoided by optimizing parameters and adjusting MA periods to filter out some noises.

-

During violent trends, MA crosses happen frequently. Other factors are needed then to determine real trend, e.g. combining indicators like RSI and MACD for confirmation, in case strong moves are missed.

Optimization Directions

-

Parameter optimization. Test different parameter combinations to find out the optimum. Such as adjusting MA periods, adding or modifying stop loss criteria etc.

-

Improve quality filter. For instance, check if volume surges on entry to avoid insufficient momentum, or examine volatility to avoid oscillations.

-

Introduce confirmation from more technical indicators to avoid wrong signals amid fierce market moves. Consider applying tools like RSI and MACD for multi-factor decision-making.

Summary

Overall this is a typical and practical trend following strategy. It adopts multiple MAs to determine trends, has strict entry rules to lock in medium-to-long term trends. Together with timely stop loss, it helps control risks. Further improvements on stability and profitability can be achieved through ways like parameter optimization and adding confirmation indicators. It suits investors who prefer following the trend for long-term trading.

- 1