Moving Average Crossover Trend Following Strategy

Overview

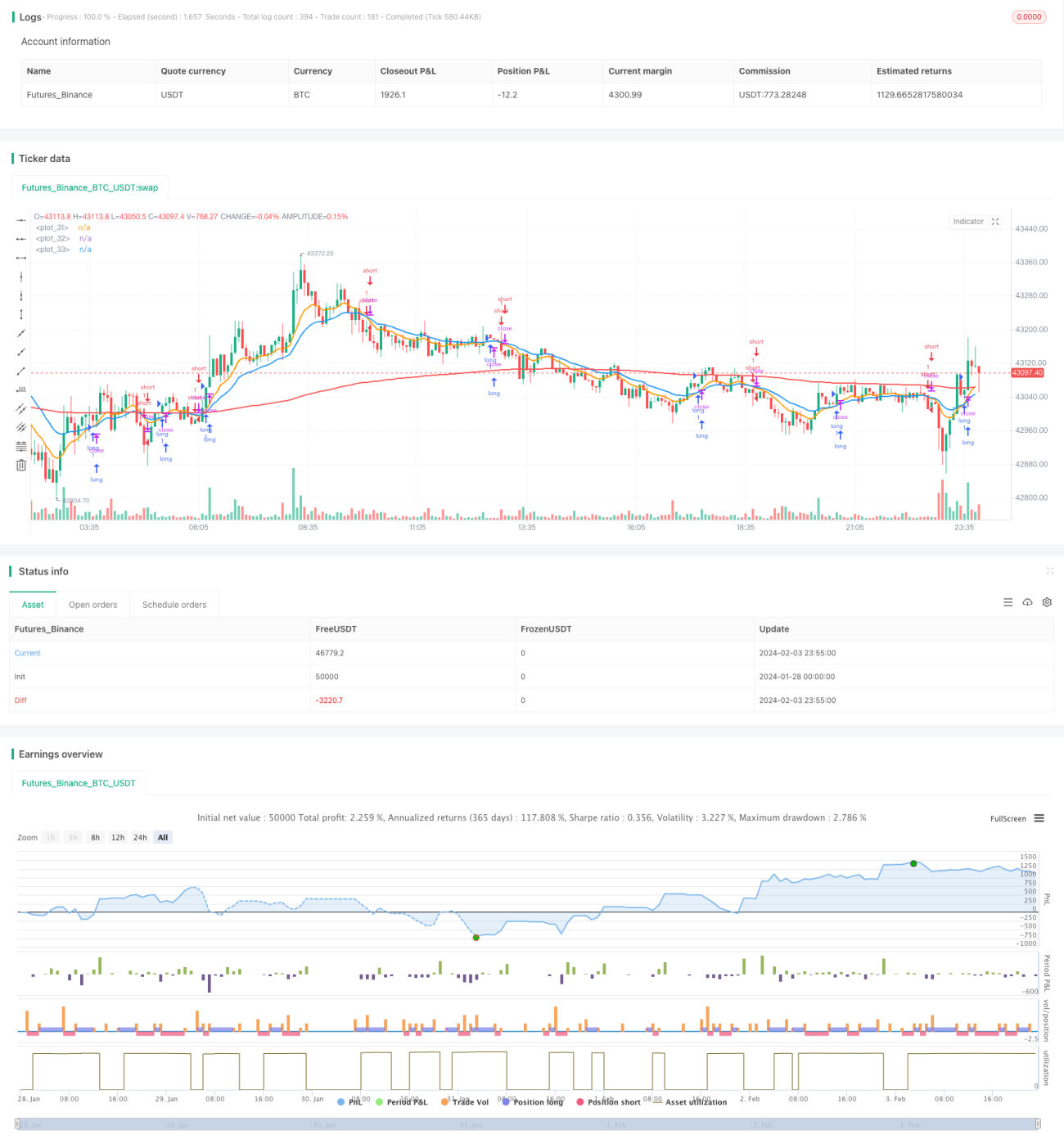

The Moving Average Crossover Trend Following strategy is a quantitative trading strategy that tracks market trends. The strategy generates trading signals by calculating fast and slow moving averages and catching turning points in market trends when crossovers occur.

Strategy Logic

The core principle of this strategy is to judge market trends using exponential moving averages (EMAs) with different parameters. The strategy defines a fast EMA and a slow EMA. When the fast EMA crosses above the slow EMA, it indicates a bullish trend reversal in the market. When the fast EMA crosses below the slow EMA, it indicates a bearish trend reversal.

On upward crosses, the strategy will open long positions. On downward crosses, the strategy will open short positions. The strategy will hold its position until take profit or stop loss is triggered, or a crossover in the opposite direction occurs again.

Advantage Analysis

The strategy has the following advantages:

- The strategy logic is simple and clear, easy to understand and implement, suitable for beginners;

- Using EMAs to smooth prices can effectively filter out market noise and identify trends;

- Parameters can be flexibly adjusted to adapt to markets with different cycles;

- The strategy can be extended to multi-timeframe versions to improve stability.

Risk Analysis

The strategy also has some risks:

- In ranging markets, multiple stop losses may occur, impacting profitability;

- It cannot effectively identify trend types (bullish or bearish), which may lead to severe losses;

- Improper EMA parameter settings may lead to over-trading or detection delays.

To mitigate risks, consider combining other indicators to determine trend types, or set wider stop loss ratios.

Optimization Directions

The strategy can also be optimized in the following aspects:

- Increase judgment of trend types to avoid opening positions against the trend;

- Add multi-timeframe judgments to improve signal quality;

- Dynamically adjust stop loss and take profit ratios to optimize exit points;

- Combine other indicators to filter out erroneous trades.

Conclusion

In summary, the Moving Average Crossover Trend Following Strategy is a simple and practical trend trading strategy. The core ideas of the strategy are clear and easy to implement, and there is also room for optimization. By adjusting parameters, adding multi-timeframe analysis, dynamic stops etc, the stability and profitability of the strategy can be continuously improved.

- 1