Squeeze Momentum Trading Strategy Based on LazyBear Indicator

Overview

This strategy is based on LazyBear's Squeeze Momentum Indicator, with added momentum filters, changed data source, and enhanced risk management system and customizable backtesting timeframe, aiming to catch price outbreaks after volatility squeeze.

Strategy Logic

The strategy uses Bollinger Bands and Keltner Channels to calculate price channels. Breakouts signal increased volatility. It incorporates LazyBear's Squeeze Momentum Indicator which uses linear regression to determine price momentum direction.

The strategy adds momentum filters, only trading when absolute momentum exceeds a threshold. On volatility squeeze (channel tightening) with momentum filter passed, it judges trend direction for long/short. It also sets stop loss, take profit and trailing stop to control risks.

Advantage Analysis

The strategy integrates multiple indicators for comprehensive judgment. It limits per trade loss with risk management mechanisms. It can timely judge post-squeeze price trends. Customizable parameters make it adaptable.

Risk Analysis

Main risks include: false breakouts causing wrong judgements; failure to reverse in time with improper parameter settings; stop loss breaches enlarging losses. These can be mitigated by optimizing parameters, adjusting risk management settings, selecting suitable products and trading sessions.

Optimization Directions

Consider combining other indicator filters like volume; fine-tune momentum threshold for higher precision; add drawdown stop loss for tighter risk control; test effectiveness across more products. These optimizations can make the strategy more robust and generalized.

Summary

The strategy judges price trends and volatility relatively comprehensively with high integration degree and improved risk control measures. It can be further enhanced through the optimization directions for strong adaptiveness in catching post-squeeze price outbreaks.

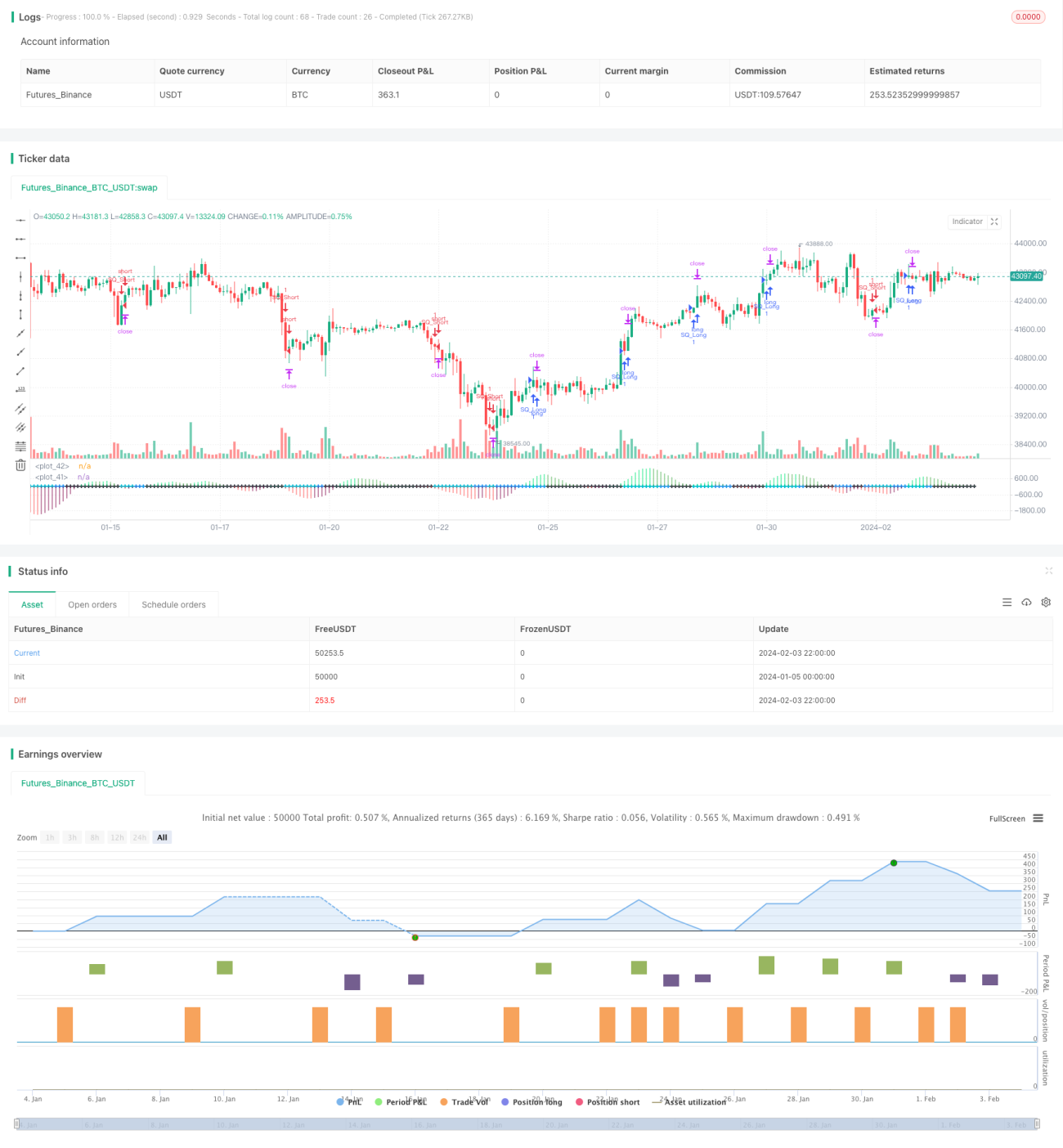

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=4

// Strategy based on LazyBear Squeeze Momentum Indicator

// © Bitduke

// All scripts: https://www.tradingview.com/u/Bitduke/#published-scripts- 1