A Dual Reversal Momentum Index Trading Strategy

Overview

The Dual Reversal Momentum Index strategy combines a 123 Reversal strategy and a Relative Momentum Index (RMI) strategy. It aims to improve the accuracy of trading decisions by utilizing dual signals.

Strategy Principle

The strategy consists of two parts:

-

123 Reversal Strategy

- Long when yesterday's close is lower than the previous day's and today's close is higher than the previous day's, and 9-day Slow K is lower than 50

- Short when yesterday's close is higher than the previous day's and today's close is lower than the previous day's, and 9-day Fast K is higher than 50

-

Relative Momentum Index (RMI) Strategy

- RMI is a variation of RSI with a momentum component added. Its formula is: RMI = (Upward Momentum SMA)/(Downward Momentum SMA)*100

- Long when RMI is lower than the overbought line; Short when RMI is higher than the oversold line

The strategy only generates trading signals when the 123 Reversal and RMI give aligned dual signals. This can effectively reduce the chance of erroneous trades.

Advantage Analysis

The advantages of this strategy include:

- Improved signal accuracy with dual indicators

- Reversal techniques suitable for range-bound markets

- Sensitive RMI to identify turning points of strong trends

Risk Analysis

There are also some risks:

- Dual filters may miss some trading opportunities

- Reversal signals could have misjudgments

- Improper RMI parameter settings may affect efficiency

These risks could be reduced by adjusting parameters, optimizing indicator calculations.

Optimization Directions

The strategy can be further optimized through:

- Testing different parameter combinations to find the optimum

- Trying different reversal indicator combinations e.g. KDJ, MACD

- Adjusting RMI formula to make it more sensitive

- Adding stop loss mechanisms to control single loss

- Combining trading volume to avoid false signals

Conclusion

The Dual Reversal Momentum Index strategy can effectively improve the accuracy of trading decisions and reduce the chance of erroneous signals through dual signal filtering and parameter optimization. It is suitable for range-bound markets to uncover reversal opportunities. The strategy can be further enhanced by adjusting parameters and optimizing indicator calculations to lower risks.

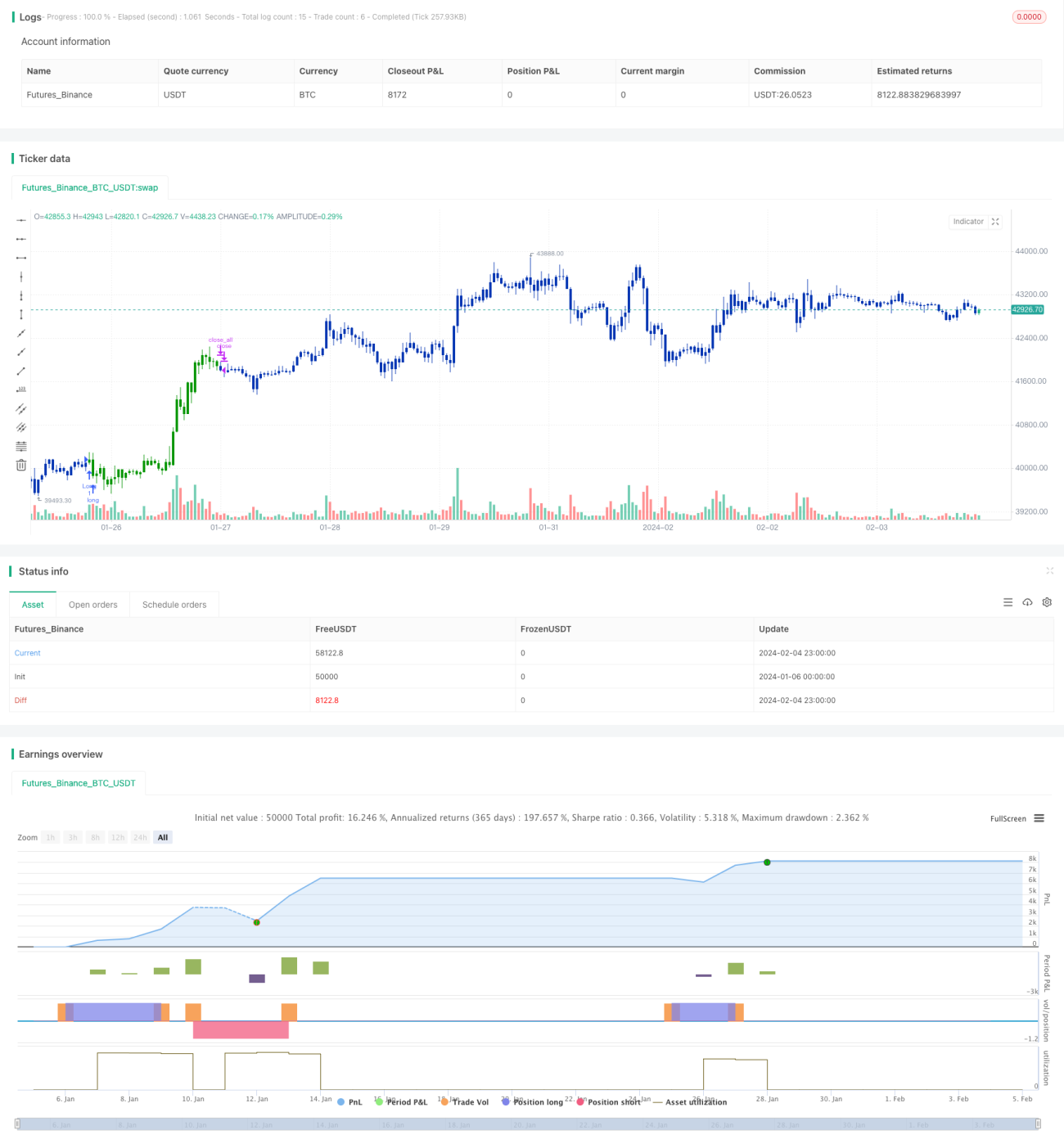

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. - 1