概述

该策略是一个基于简单移动平均线(SMA)和平均真实波动率(ATR)设置动态跟踪止损的长线交易策略。它结合了趋势跟踪和风险管理的优点,旨在控制回撤并让利润最大化。

策略原理

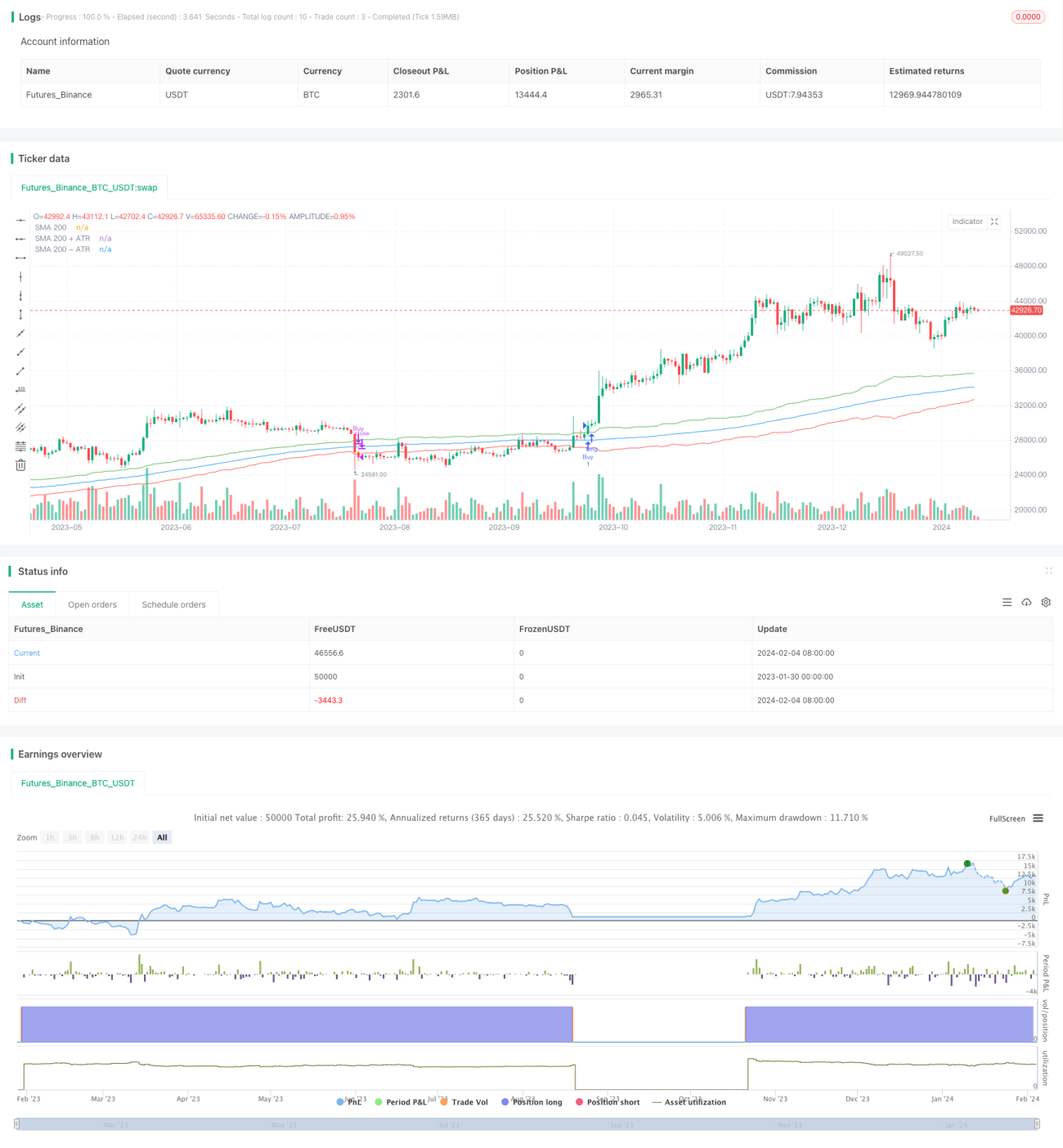

当收盘价上穿SMA 200天加ATR 14天时,做多入场。当收盘价下穿SMA 200天减ATR 14天时,平仓止损。该策略使用SMA 200判断大趋势方向,使用ATR设置止损线,实现动态跟踪止损。具体来说,买入信号是收盘价突破SMA 200加ATR 14天,这个突破表示当前处于上升趋势中。止损信号是收盘价跌破SMA 200减ATR 14天,这个突破表示上升趋势被打破。

优势分析

该策略结合了SMA和ATR两个指标的优势。SMA 200可过滤市场噪音,锁定长线主方向;而ATR 14天可以根据最近两周的波动率设定止损线,达到动态跟踪止损的效果。这实现了在趋势中的持续盈利,同时也可有效控制回撤。总体来说,该策略的优势有:

-

盈亏比高。跟随趋势运行,止损控制风险,从而取得较高盈亏比。

-

回撤可控。ATR动态跟踪降低突发事件的影响,有效控制回撤。

-

参数简单。只使用两个参数,实现风险与收益的平衡,避免过度优化。

风险分析

该策略也存在一些风险需要关注。主要风险如下:

-

趋势反转风险。策略本身无法判断趋势反转,如果出现突然调头可能带来较大亏损。

-

SMA延迟风险。SMA有一定滞后性,无法即时反映趋势变化。

-

ATR参数设置风险。ATR参数设置过大或过小,都会影响策略表现。

对应解决方法:

- 结合其他指标判断趋势,如MACD。

- 测试不同参数组合寻找最佳平衡。

优化方向

该策略还可从以下几个方面进行优化:

-

测试不同的SMA和ATR参数组合,寻找最佳参数。

-

增加其他技术指标判断反转,如MACD。

-

优化止损机制,如变化止损、移动止损等方式。

-

结合股票的基本面指标,避免买入上涨无望的个股。

总结

该策略整合了趋势跟踪和动态风险管理的方法,实现了长线持有期间的止损与止盈优化。它具有盈亏比高、回撤可控、风险收益平衡的特点。但也存在一定的趋势反转风险和参数优化难度。总体而言,该策略可为量化交易提供一个简单有效的长线交易思路,值得进一步测试与优化。

- 1