Dynamic Slope Trend Line Trading Strategy

Overview

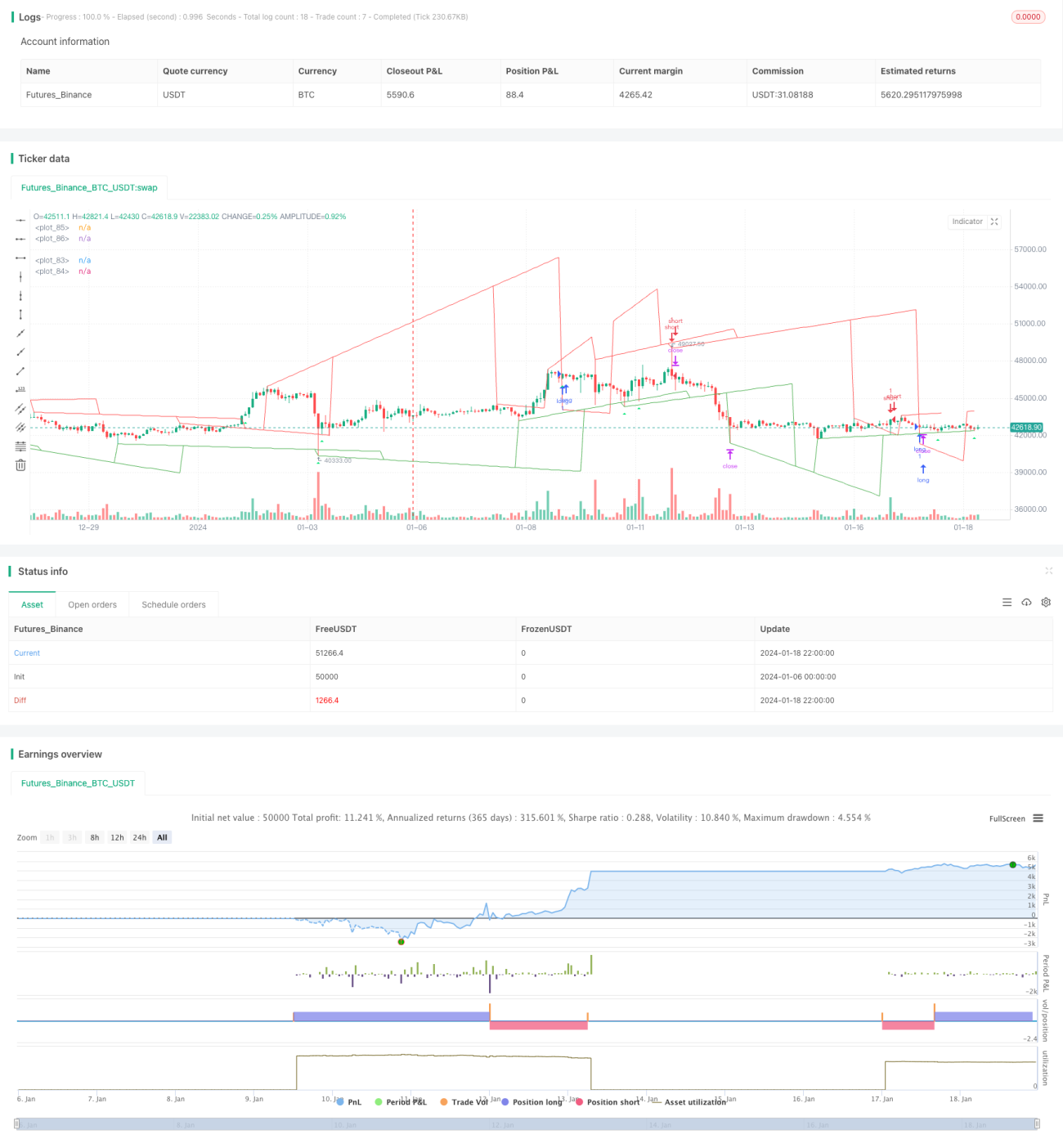

The core idea of this strategy is to use dynamic slope to determine the price trend direction and generate trading signals in combination with breakout judgment. Specifically, it tracks price highs and lows in real time based on price changes over different time periods to calculate the dynamic slope, and then determines long and short signals according to the breakout of price against trend lines.

Strategy Principle

The main steps of this strategy are:

-

Judge highest and lowest price: Track the highest and lowest prices over a certain cycle (e.g. 20 bars) to determine whether a new high or low has been reached.

-

Calculate dynamic slope: Record the bar number when a new high or low is reached, and calculate the dynamic slope from the new high/low point to the high/low point after a certain cycle (e.g. 9 bars).

-

Plot trend lines: Plot ascending and descending trend lines based on dynamic slopes.

-

Extend and update trend lines: When price breaks through trend lines, extend and update trend lines.

-

Trading signals: Determine long and short signals based on price breakouts against trend lines.

Advantages of the Strategy

The advantages of this strategy include:

-

Dynamically determine the trend direction for flexibility in response to market changes.

-

Reasonably control stops and minimize drawdowns.

-

Clear breakthrough trading signals that are easy to implement.

-

Customizable parameters for strong adaptability.

-

Clean code structure that is easy to understand and develop further.

Risks and Solutions

There are also some risks with this strategy:

-

Frequent longs and shorts when trend is range-bound. Add filter conditions.

-

Potentially more false signals on breakouts. Adjust parameters or add filters.

-

Stop loss risks when market moves violently. Expand stop loss range.

-

Limited optimization space and profit potential, suitable for short-term trading.

Optimization Directions

Areas for optimizing the strategy include:

-

Add more technical indicators as filter signals.

-

Optimize parameter combinations for the best parameters.

-

Try to improve stop loss strategies to lower risks.

-

Add functionality to automatically adjust entry price range.

-

Try combining with other strategies to discover more opportunities.

Summary

Overall this is an efficient short-term strategy based on using dynamic slope to determine trends and trading breakouts. It has accurate judgments, controllable risks, and is suitable for capturing short-term opportunities in the market. Further optimizations on parameters and adding filters can improve the win rate and profitability.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1