概述

本策略将RSI指标与价格突破结合,在一定趋势下形成的盘整范围内寻找轮动机会,进而进行短线交易,追求高效率的短线获利。

策略原理

- RSI指标判断:当RSI指标小于超卖线30时产生买入信号,作为潜在的反转买点;当RSI指标大于超买线60时产生卖出信号,锁定利润;

- 窗口限制:只在指定的回测时间窗口内生效,从而限制策略效力,防止全局套利;

- 突破判断:结合价格走势,寻找突破的机会,增强策略的实际效果,防止不必要的空转。

所以,该策略综合多个维度的判断逻辑,在一定的趋势和突破机会下,利用RSI指标产生的买卖信号进行短线获利的轮动操作。可以有效抓住市场短期的超跌反弹和超买回落的机会。

优势分析

- 结合多重逻辑判断,相较于简单的RSI策略,更加严谨,可以有效避免双向空转带来的不必要损失;

- 利用RSI指标判断局部极值区域,寻找反转机会,从而获利;

- 设置回测时间窗口,可针对特定市场行情进行验证和优化,提高策略实际可用性;

- 追求短线获利,不需要预测趋势转向,更加容易把握,降低风险。

风险与解决方法

- 无法直接判断整体趋势方向,需要人工分析大局;

- RSI指标滞后反应价格变化,可能错过最佳买卖点;

- 需要充分了解策略适用的大行情环境;

- 可引入更多技术指标判断大趋势,优化策略参数,提高策略灵活性。

优化方向

- 增加对大趋势的判断,避免长期滞留亏损的单子;

- 调整RSI参数,优化超买超卖线,提高效果;

- 增加止损逻辑;

- 优化回测窗口范围,让策略更契合实际行情。

总结

本策略利用RSI指标判断超买超卖的短期反转机会,同时结合价格突破进行短线获利的轮动操作。特点是追求短期效率,操作简单,风险有限,非常适合短线交易者在特定行情下使用。需要注意判断整体大趋势,并优化参数等,从而获得更好的效果。

策略源码

Pine

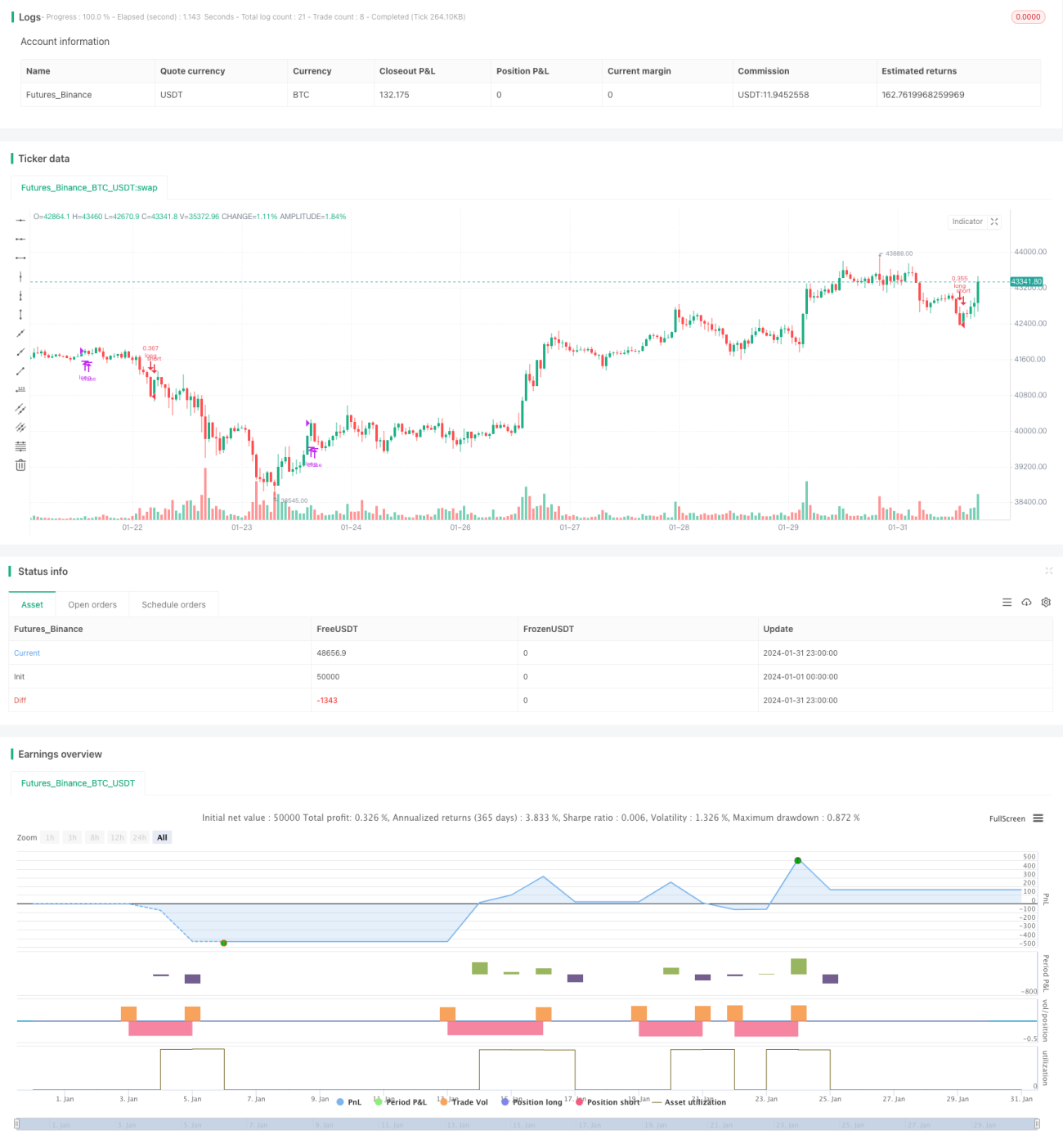

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © relevantLeader16058

//@version=4策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1