Double Momentum Index and Reversal Hybrid Strategy

Overview

The Double Momentum Index and Reversal Hybrid Strategy is a composite strategy combining reversal and momentum strategies. It integrates the 123 Reversal Strategy and the Commodity Selection Index (CSI) as sub-strategies to determine entry signals based on dual confirmation. The strategy aims to improve the accuracy of trading signals.

Strategy Logic

The strategy consists of two sub-strategies:

-

123 Reversal Strategy. It goes long when the closing price rises for two consecutive days and Stoch is below 50; it goes short when the closing price falls for two consecutive days and Stoch is above 50. It’s a reversal-type strategy.

-

Commodity Selection Index (CSI) Strategy. It combines the Average True Range (ATR) and the Average Directional Movement Index (ADX). ATR reflects market volatility and ADX reflects trend strength. The higher the CSI value, the stronger the market trend and volatility. It’s a momentum tracking strategy.

The whole strategy takes the 123 Reversal strategy as the main body and CSI as an assistant confirmation. Trading signals are generated only when the signals of both strategies are consistent. It goes long when the closing price rises for two consecutive days and Stoch is below 50, and at the same time when CSI crosses above its moving average; it goes short when the closing price falls for two consecutive days and Stoch is above 50, and at the same time when CSI crosses below its moving average.

This ensures the reversal attribute of trading signals, while adding CSI to filter can reduce false signals.

Advantages

The strategy has the following advantages:

-

Combining reversal and momentum improves signal accuracy. The 123 Reversal as the main signal can capture sudden and violent reversals. CSI as confirmation can filter out some noise.

-

Adopting composite filtering can greatly reduce net positions. Even if the sub-strategies themselves have some false signals, the final signal must be double confirmed, which can filter out most false signals and minimize unnecessary opening and closing of positions.

-

The parameters of sub-strategies can be optimized separately without interference with each other. This facilitates finding the optimal parameter combination.

-

Sub-strategies can be enabled separately. The strategy supports using only 123 Reversal or CSI for trading alone. This provides flexibility.

Risk Analysis

Although the strategy significantly reduces false signals through composite filtering, there are still the following main risks:

-

The frequency of strategy signal generation is relatively low. By adopting double confirmation, a certain proportion of trading opportunities will inevitably be filtered out. This is the inevitable cost to achieve high win rate.

-

If the parameters of the two sub-strategies are improper, it may result in rare or even no signals. Strict testing and optimization of the parameters are needed to find the optimal parameter combination.

-

123 Reversal belongs to counter-trend operations. In case of consecutive and violent one-way price breakthroughs, the strategy will face greater risks. It’s advisable to add in stop loss to control risk.

Optimization Direction

The main optimization possibilities of this strategy are in the following areas:

-

Optimize the intrinsic parameters of each sub-strategy to find the optimal parameter combinations, including the parameters of Stoch, CSI, etc.

-

Test adding in different market condition filters, like using CSI only when trend prevails, using 123 Reversal only in range-bound markets, etc. This can overcome the disadvantages of sub-strategies to some extent.

-

Develop parameter self-adaptation and dynamic optimization modules, allowing the strategy to automatically adjust parameters and track optimal parameter combinations according to market conditions and statistics in real time.

-

Test different stop loss mechanisms. Proper stop loss can both effectively control risks and reduce unnecessary opening and closing of positions.

Summary

The Double Momentum Index and Reversal Hybrid Strategy utilizes the ideas of multi-signal confirmation and combination, making good use of the respective strengths of reversal and momentum strategies, while overcoming their shortcomings by mutual filtering, to achieve high efficiency and stability. It serves as a typical quantitative strategy to be considered for adoption.

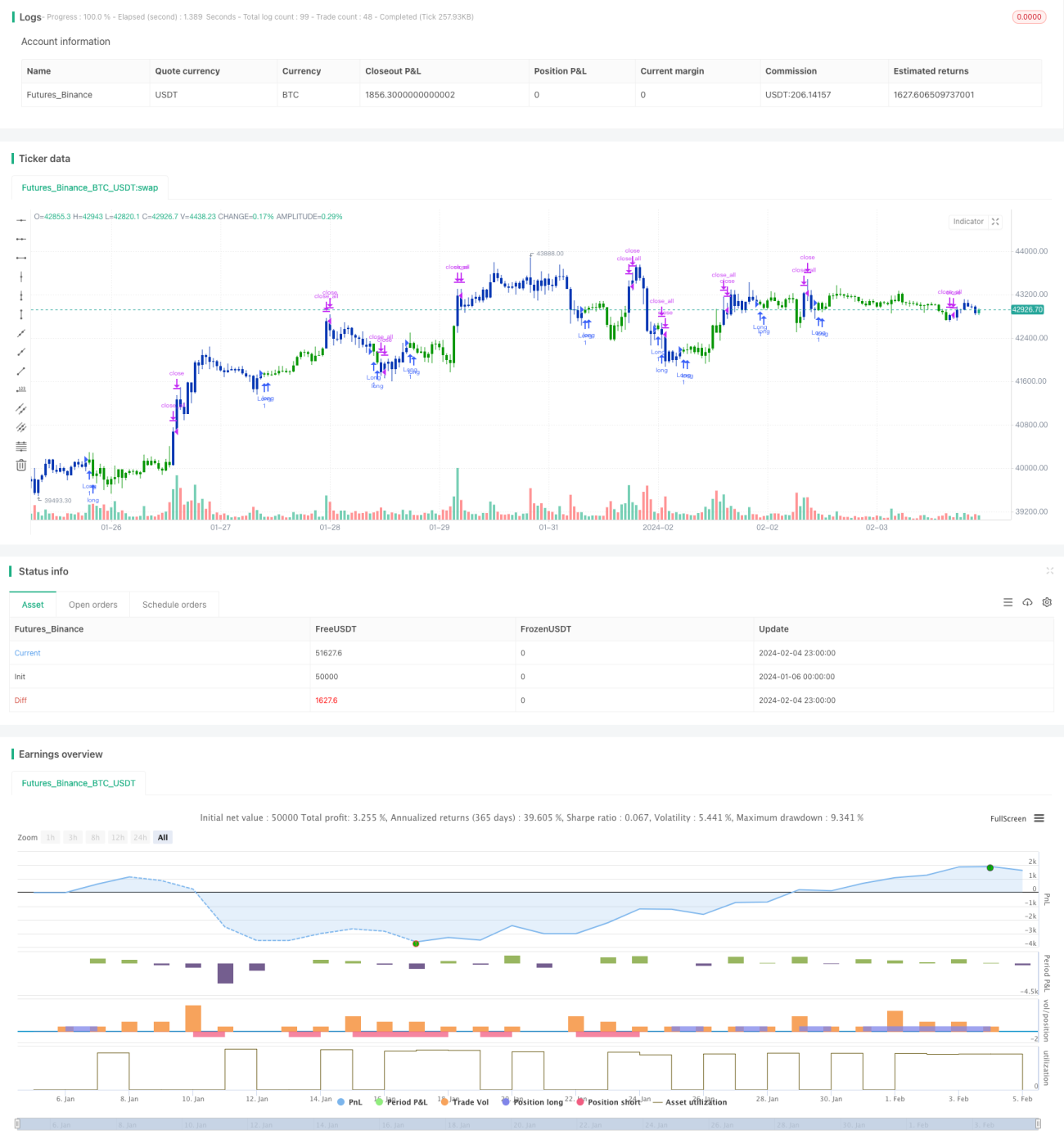

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/10/2019

// This is combo strategies for get a cumulative signal. - 1