3 Moving Average Swing Interval Reversal Strategy

Overview

This strategy uses a 3-day fast moving average, 10-day slow moving average and 16-day signal smoothing moving average to construct the MACD indicator, supplemented by the RSI indicator and volume characteristics, and sets multidimensional K-line characteristics to determine over-extension of the market trend, forming a range swing trend and reversal long or short entries for profit taking.

The strategy aims to capture quick price reversals from local overbought or oversold levels. It typically performs well for 0DTE SPY Options using 15m timeframe.

Strategy Logic

The strategy mainly uses 3-day fast moving average minus 10-day slow moving average to form the MACD indicator, with 16-day signal line for smoothing, constituting a standard MACD strategy. It also combines volume analysis of buying and selling volumes to determine momentum characteristics. The RSI indicator is introduced to determine overbought or oversold levels. Through the combination of multiple indicators, it judges market characteristics and detects changes in interval swing trends to construct entry signals.

Specifically, by observing the relationship between the MACD line and signal line, as well as the slope changes, it determines the ebb and flow of bullish and bearish forces to spot reversal opportunities. At the same time, changes in buying and selling volumes reflect shifts in bullish and bearish momentum. Combined with the changes in the RSI indicator to determine overbought and oversold conditions, these indicators allow us to ascertain localized market profile features and potential reversal timing.

The strategy sets up 3 entry signals in total:

-

Long when buying volume has no advantage over selling volume, RSI below 41 while rising, MACD signal has no significant deviations;

-

Long when buying volume is stronger than selling volume, RSI in the 45-55 range and rising, MACD and signal line moving up in unison;

-

Short when MACD is above the threshold while rising.

These 3 scenarios all reflect localized ranging swings in a directional over-expansion, judged as opportune reversal timing for counter-direction entries.

Exits are set as Take profit (limit order) and Stop loss, to control drawdowns and realize profits.

Advantage Analysis

The strategy combines multiple indicators to determine ranging and overbought/oversold conditions, with a clear reversal profit-taking logic. It utilizes volume analysis for additional conviction on entries. The stop loss and take profit also helps avoid over-trading in one direction while securing profits early.

Specifically, advantages include:

-

MACD as volume-weighted momentum oscillator, avoids simplistic technical analysis;

-

Volume conditions add to entry conviction;

-

RSI assists in spotting potential reversals;

-

Stop loss and take profit controls excessive drawdowns and locks in some profit.

Risk Analysis

Despite combining indicators to improve win rate, all strategies have risks. Main issues are:

-

Probability of false signals, like continuations after initial reversal;

-

Inadequate stop loss and take profit settings lead to oversized drawdowns and failure to lock in profit;

-

Parameter tuning like MA lengths, RSI periods, take profit ratios may need further optimization.

These risks can be reduced through additional optimization. Specific methods are elaborated in next section.

Optimization Directions

There remains room for further optimization, mainly:

-

Test different MA parameter combinations for best results;

-

Test RSI lookback periods to find optimum overbought/oversold judge;

-

Optimize take profit and stop loss ratios to balance drawdowns and profit capture;

-

Introduce machine learning models, leverage more data to reduce misjudgements and improve win rate.

These can be implemented through more systematic backtests. As parameter spaces expand and sample sizes grow, strategy win rate and profitability will also improve.

Conclusion

This strategy combines MACD, RSI and volume analysis to determine market ranging features, establishing entries at reversal zones to capture retracement moves. The logic is clear, balancing trend and reversals. With further optimization, it has strong profit potential as a robust quant strategy. Parameter tuning and model introduction can enhance it into a highly efficient algorithm.

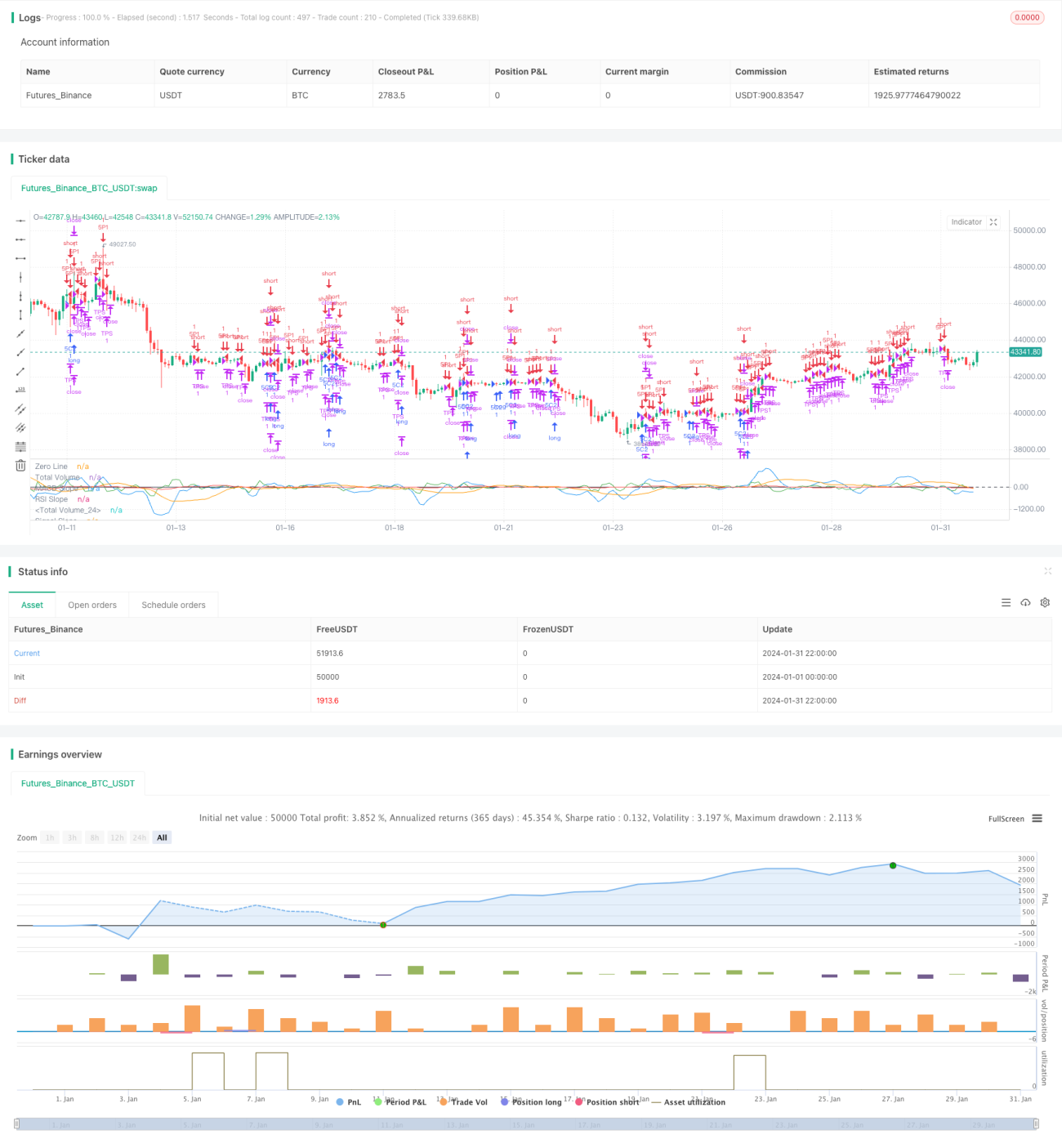

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("3 1 Oscillator Profile Flagging", shorttitle="3 1 Oscillator Profile Flagging", overlay=false)

signalBiasValue = input(title="Signal Bias", defval=0.26)- 1