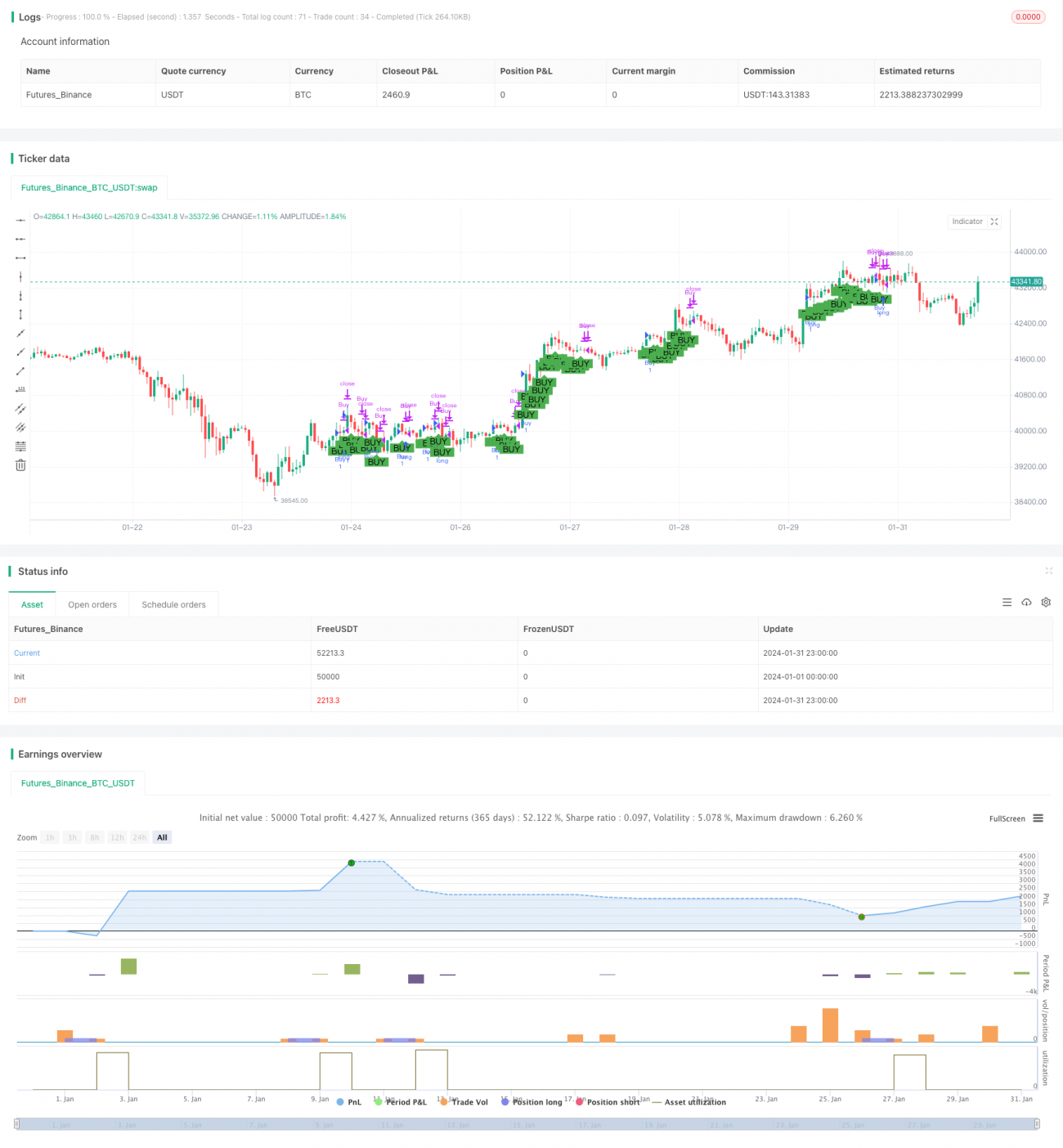

Comprehensive Futures Automated Trading Strategy for Both Long and Short

This strategy is an innovative Comprehensive Futures Automated Trading Strategy for Both Long and Short. It integrates SuperTrend, QQE and Trend Indicator A-V2 to automatically discover trading signals and make long/short trades. This strategy aims to identify main market trends and achieve steady profits with good risk control.

Strategy Principle

The strategy consists of three main parts:

-

SuperTrend indicator determines the main market trend. When price breaks above the up trendline, it indicates an uptrend. When price breaks below the down trendline, it indicates a downtrend.

-

QQE indicator combines RSI to identify overbought/oversold status. Dynamic overbought/oversold levels are calculated based on RSI average and standard deviation. RSI above upper level indicates overbought signal and RSI below lower level indicates oversold signal.

-

Trend Indicator A-V2 judges the trend by comparing fast and slow EMA lines. When fast EMA is higher than slow EMA, it sends a buy signal.

When judging market direction, long signals are triggered when SuperTrend shows uptrend, QQE not oversold and A-V2 buy signal occurs. Short signals are triggered when opposite conditions occur.

Advantages

-

Using multiple indicators improves reliability and reduces false signals.

-

Automated signal discovery without manual interference reduces human errors.

-

Organic combination of indicators provides effective risk control while discovering trading opportunities.

-

Customizable parameters to meet users' needs.

-

Support both long-only and long/short trading for flexibility.

Risks and Solutions

-

Indicators may generate false signals under extreme market conditions. Fine-tune parameters to minimize such cases.

-

Transaction costs and slippage could erode profits. Optimize with stop loss/take profit.

-

Inadequate parameter setup leads to poor performance. Try different values to find optimal configuration.

Optimization Directions

-

Increase machine learning to auto optimize parameters based on historical data.

-

Incorporate more market micro-structure factors like volume to discover better signals.

-

Implement high frequency trading techniques to auto submit orders.

Conclusion

The strategy combines indicators to assess market structure and achieves steady profits under risk control. It considers both trend direction and overbought/oversold status for nuanced trading decisions. Much room remains for parameter optimization, logic improvements and execution enhancements to further lift strategy performance.

- 1