Multi Timeframe RSI-SRSI Trading Strategy

Overview

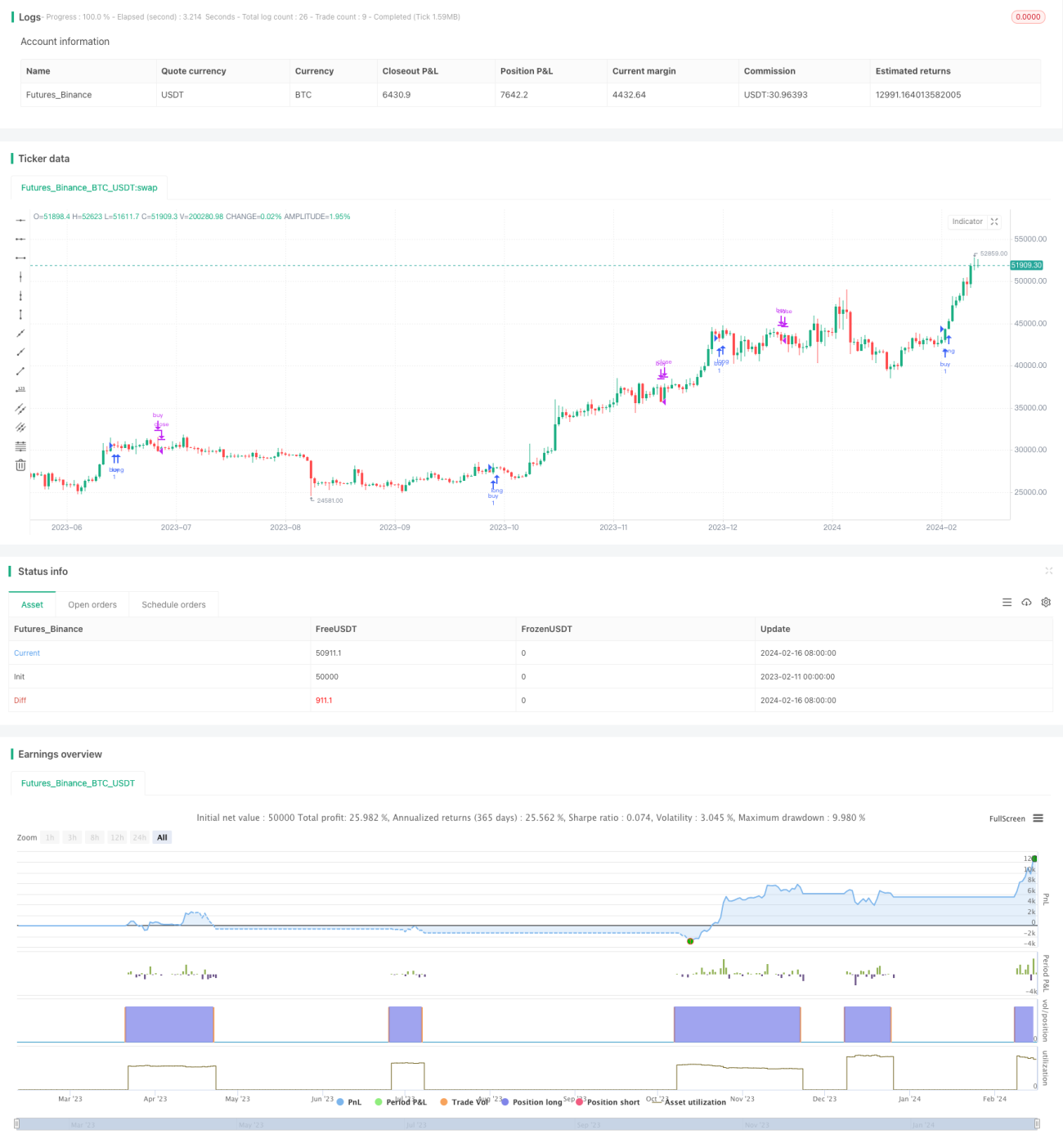

This trading strategy combines the Relative Strength Index (RSI) and Stochastic Relative Strength Index (Stochastic RSI) technical indicators to generate trading signals. Additionally, it utilizes the price trend of cryptocurrencies in higher timeframes to confirm the trend and increase signal reliability.

Strategy Name

Multi Timeframe RSI-SRSI Trading Strategy

Strategy Logic

The strategy judges overbought and oversold conditions based on RSI values. RSI below 30 is considered oversold signal and RSI above 70 is considered overbought signal. The Stochastic RSI indicator observes the fluctuation of RSI values. Stochastic RSI below 5 is oversold and Stochastic RSI above 50 is overbought.

The strategy also incorporates the price trend of cryptocurrency in higher timeframes (e.g. weekly). Only when higher timeframe RSI is above a threshold (e.g. 45), long signals are triggered. This filters out non-persistent oversold signals when the overall trend is down.

The buy and sell signals need to be confirmed for a number of periods (e.g. 8 bars) before an actual trading signal is generated to avoid fake signals.

Advantages

- Classic technical analysis method using RSI to identify overbought/oversold levels

- Incorporates Stochastic RSI to catch reversals of RSI

- Applies multi-timeframe techniques to filter fake signals and improve quality

Risks & Solutions

- RSI prone to generating false signals

- Combine other indicators to filter fake signals

- Apply trend confirmation techniques

- Improper threshold settings can produce too many signals

- Optimize parameters to find best combination

- Signals need confirmation time

- Balance confirmation periods - filter fake signals without missing opportunities

Enhancement Areas

- Test more indicator combinations for stronger signals

- e.g. incorporate MACD indicator

- Utilize machine learning methods to find optimal parameters

- e.g. genetic algorithms/evolutionary algorithms for automated optimization

- Add stop loss strategies to control single trade risks

- Set stop loss when price breaks support level

Conclusion

The strategy mainly relies on the two classic technical indicators, RSI and Stochastic RSI, to generate trading signals. Additionally, the introduction of trend confirmation from higher timeframes helps filter fake signals effectively and improves signal quality. Further performance improvement can be achieved by optimizing parameters, adding stop loss and other means. The logic is simple and easy to understand. It serves a good starting point for quant trading.

- 1