Major Trend Indicator Long

Overview

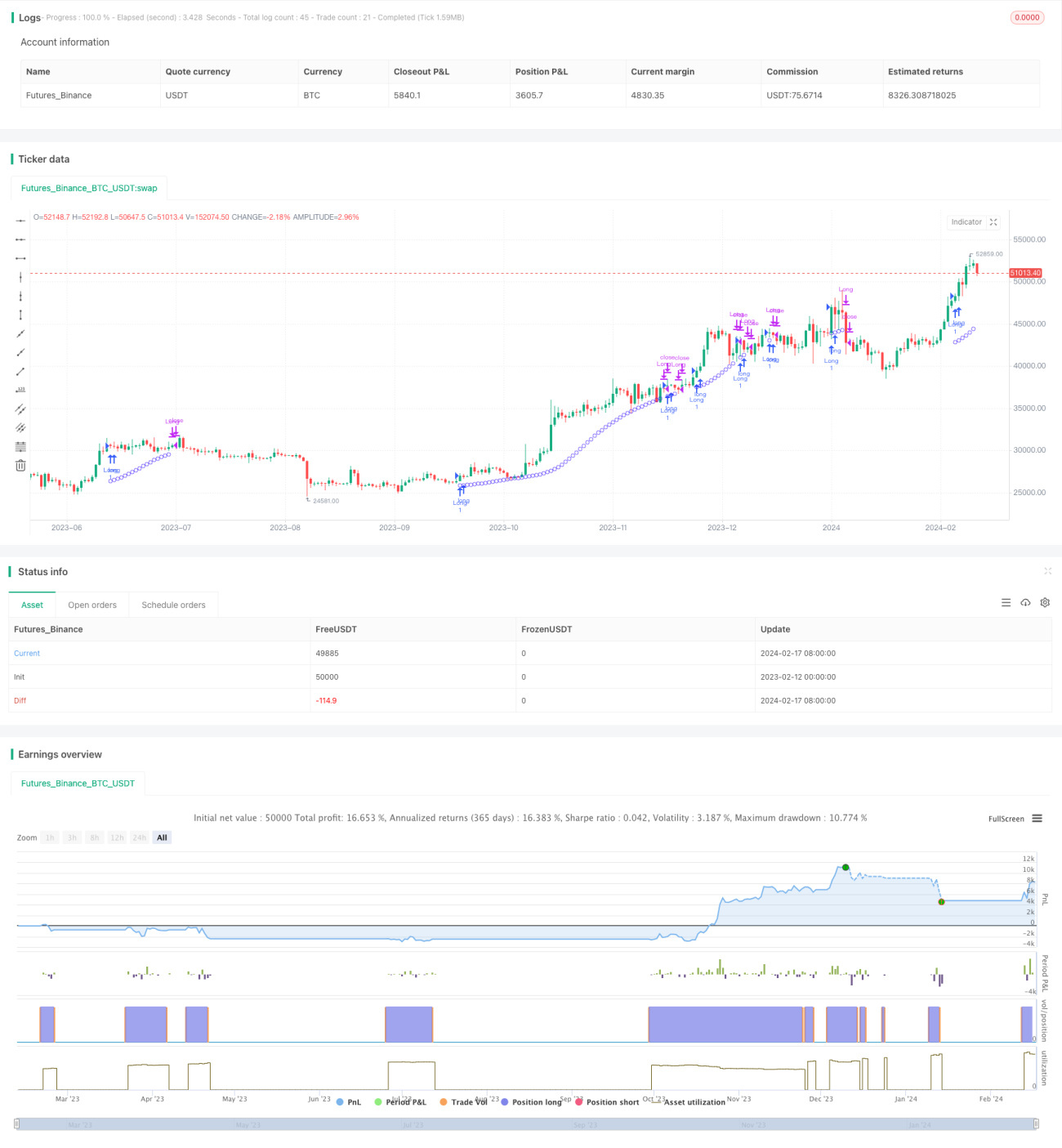

The Major Trend Indicator Long (MTIL) strategy is designed for use across various financial instruments including cryptocurrencies like BTCUSD and ETHUSD as well as traditional stocks such as AAPL. It aims to identify potential bullish trends for entering long positions.

Strategy Logic

The MTIL strategy utilizes optimized parameters to calculate the highest and lowest prices within defined lookback periods. It then applies linear regression to smooth the price data, spotting potential uptrends to signal long entries.

Specifically, it first derives the highest and lowest prices over given periods. These are then smoothed using linear regression with differing coefficients. This results in the creation of upper and lower bounds. When the smoothed highest prices breach the upper band, the smoothed lowest prices breach the lower band, and the short term linear regression of closing prices is above that of the long term - a bullish signal is generated.

Advantage Analysis

The MTIL strategy has the following advantages:

- Utilizes dual-smoothing techniques for trend identification with higher accuracy

- Customizable backtest start date for testing historical performance

- Customizable parameters catering to individual trading preferences

- Can be combined with short strategy for multi-timeframe analysis

Risk Analysis

The MTIL strategy also carries the following risks:

- Trend trading risks with possibility of magnified losses

- Inappropriate parameter tuning leading to missed opportunities or wrong signals

- Need to account for trading costs to avoid overly frequent trades

Some risks can be mitigated via parameter adjustment, stop losses, trade cost control etc.

Optimization Directions

The MTIL strategy can be optimized across the following dimensions:

- Testing combinations of different period parameters to find optimum

- Incorporating price-volume confirmation to avoid false signals

- Adding other indicators to further validate momentum and intraday moves to reinforce signal confirmation

- Establishing stop loss and take profit rules to limit downside vs lock in profits

Conclusion

The MTIL is a long side strategy harnessing linear regression techniques to spot major trends. Through parameter tuning it can be adapted across various market environments. When combined with a short side strategy it offers more comprehensive analysis. Further optimizations can enhance its accuracy and profitability.

- 1