Best ABCD Pattern Trading Strategy with Stop Loss and Take Profit Tracking

I. Strategy Overview

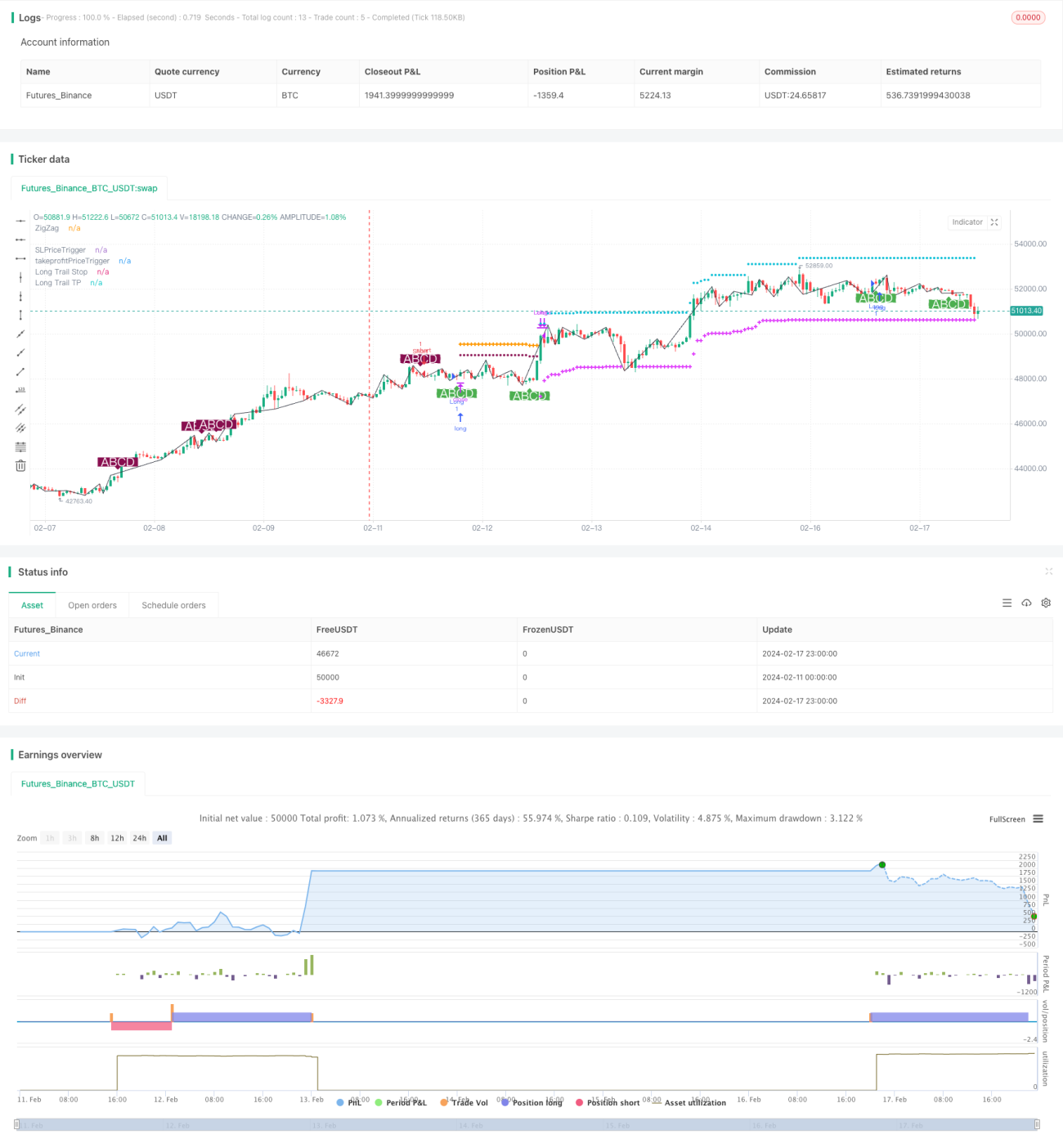

This strategy is named "Best ABCD Pattern Strategy (with Stop Loss and Take Profit Tracking)". It is a quantitative strategy that trades based on a clear ABCD price pattern model. The main idea is to go long or short according to the direction of the ABCD pattern after identifying a complete ABCD model, and set stop loss and take profit tracking to manage positions.

II. Strategy Principle

-

Identify the extremum points of price using Bollinger Bands to get the ZigZag line.

-

Recognize complete ABCD patterns on the ZigZag line. Points A, B, C and D need to meet certain proportional relationships. Go long or go short after identifying eligible ABCD patterns.

-

Set trailing stop loss after opening positions to control risks. Use fixed stop loss first, turn to trailing stop loss to lock in some profits after reaching a certain profit level.

-

Similarly, trailing take profit is also set to secure enough profits in time and avoid losses. Trailing take profit also works in two stages: fixed take profit first and then trailing take profit.

-

Close positions when price hits the trailing stop loss or take profit to finish a trade cycle.

III. Advantage Analysis

-

Using Bollinger Bands to identify ZigZag line avoids repainting problems of traditional ZigZag, making trading signals more reliable.

-

ABCD pattern trading model is mature and stable with adequate trading opportunities. Also it is easy to determine the position direction.

-

The two-stage trailing stop loss and take profit settings help better control risks and secure profits. Trailing features provide flexibility.

-

Reasonable parameter design as percentages of stop loss, take profit and trailing activation are all customizable for flexibility.

-

The strategy can be used for any trading instruments, including forex, crypto currencies, stock indices, etc.

IV. Risk Analysis

-

Trading opportunities for ABCD patterns are still limited compared to other strategies, not ensuring enough frequency.

-

During ranging markets, stop loss and take profit may get triggered frequently. Parameters need adjustments like widening stop loss/profit ranges.

-

Liquidity of the trading instruments needs attention. Slippage needs consideration for illiquid products.

-

The strategy is sensitive to transaction costs. Brokers and accounts with low commission rates are preferred.

-

Some parameters can be further optimized, like the activation levels for trailing stop loss and take profit. More values can be tested to find the optimum.

V. Optimization Directions

-

Combining with other indicators to add more filters avoids some false signals and reduces inefficient trades.

-

Add judgement on the three-section market structure, only taking trades in the third section. This can improve the win rate.

-

Test and optimize the initial capital to find the optimum level. Both too big and too small sizes hurt return rates.

-

Carry out walk-forward analysis with out-of-sample data to examine the robustness of parameters over long term.

-

Continue optimizing activation conditions and slippage sizes of trailing stop loss and take profit to improve efficiency. Optimization of settings never ends.

VI. Strategy Summary

The strategy mainly relies on ABCD pattern for market timing and entries. Two-stage trailing stop loss and take profit settings are used to manage risks and profits. The strategy is relatively mature and stable but trading frequency may be low. We can obtain more efficient trading opportunities by adding filters and conditions. Also further parameter tuning and capital sizing can improve its profit stability. Overall speaking, this is a strategy with clear logic and easy to understand, worth in-depth research and application in actual quantitative trading.

- 1