Trading-oriented Ichimoku Cloud Nine Strategy

Overview

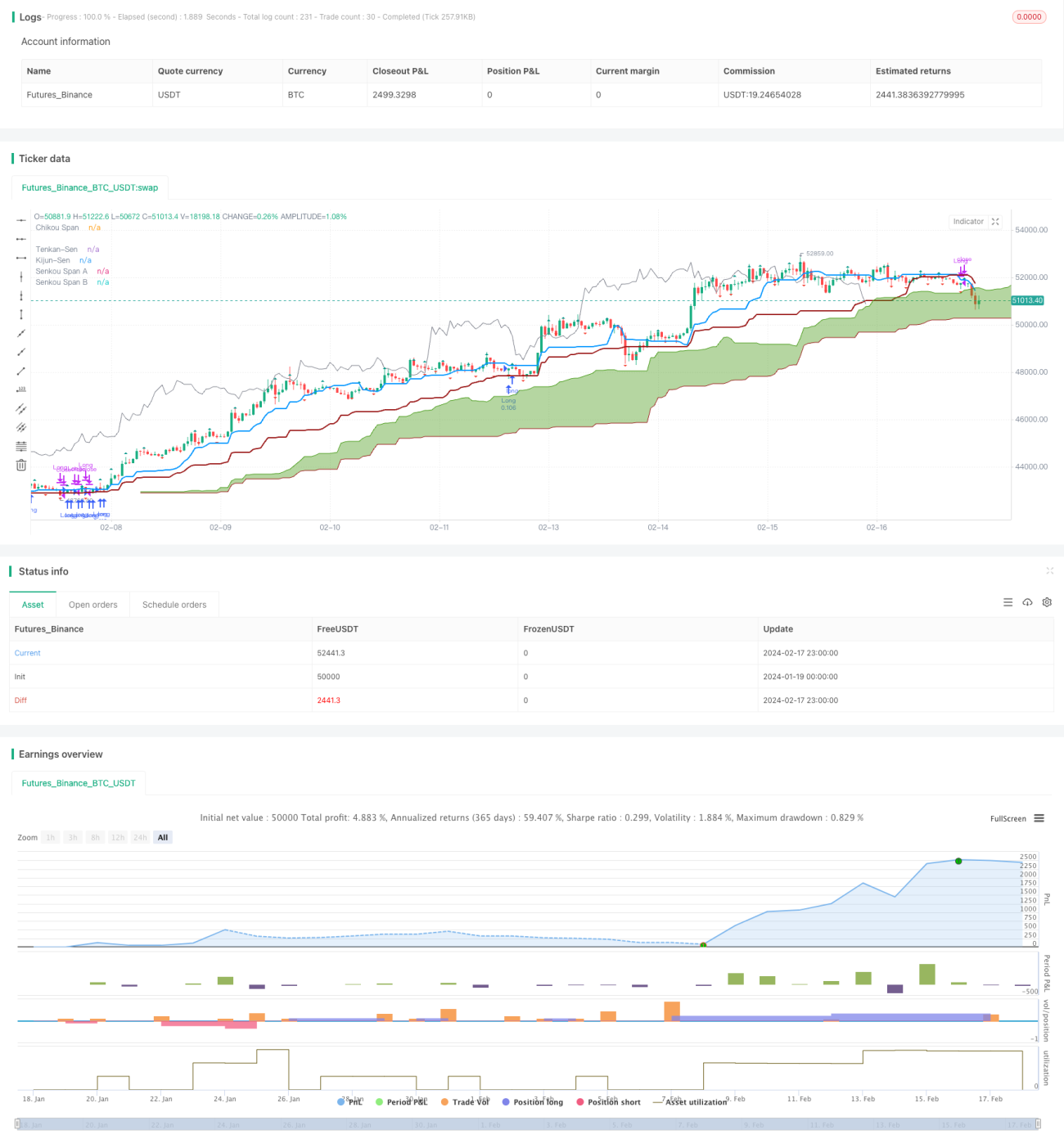

The Ichimoku Cloud Nine strategy is built on top of the Ichimoku Cloud indicator combined with the usage of Williams Fractals. This is a trading-oriented strategy that utilizes multiple trade signals from the Ichimoku Cloud.

Strategy Logic

The strategy mainly uses the following Ichimoku signals to enter trades:

- Kumo Breakout: generates signal when price closes above or below the cloud

- TK Cross: generates signal when Tenkan crosses Kijun

- Kumo Twist: generates signal when Senkou Span A crosses Senkou Span B

- Edge to Edge: generates signal when price enters either side of the Cloud

The strategy will exit trades in the following situations:

- Price closing inside the Cloud

- TK Cross in opposite direction

- Breach of Williams Fractal in opposite direction

The strategy combines multiple Ichimoku signals to increase reliability while utilizing fractals as stop loss to control risk.

Advantages

Compared to single signal strategies, this strategy filters signals through multiple Ichimoku signals, improving accuracy. Strategy parameters are flexible for optimization across products.

Usage of fractals as stop loss actively controls risk and locks in profits.

Risks

Main risks faced:

- Lagging nature of Ichimoku Cloud

- Multiple signals may be too conservative missing opportunities

- Fractal stop loss could be taken out

Mitigations: Adjust parameters or remove some signals. Tune fractal time period or only partial stop loss on fracture.

Enhancement Opportunities

Main areas for optimization:

- Adjust Ichimoku parameters for different products

- Remove some signals, retain core rules

- Tune fractal parameters to use higher timeframes or only partial stop

- Add other indicators like volume

Conclusion

The Ichimoku Cloud Nine strategy improves Ichimoku trading by combining signals to increase accuracy and win rate. Usage of fractals manages risk. Parameters and signals can be optimized for automated trading across different products.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1