DYNAMIC MOMENTUM OSCILLATOR TRAILING STOP STRATEGY

Overview

This strategy combines Bollinger Bands and Stochastic oscillator to identify overbought and oversold opportunities in the market. It aims to capitalize on price rebounds from the extremes defined by Bollinger Bands, with confirmation from Stochastic to maximize the probability of successful operations. DYNAMIC TRAILING STOP adopts dynamic stop loss methodology to flexibly adjust stop loss position based on market volatility, ensuring stop loss effect while avoiding being stopped out too easily.

Strategy Logic

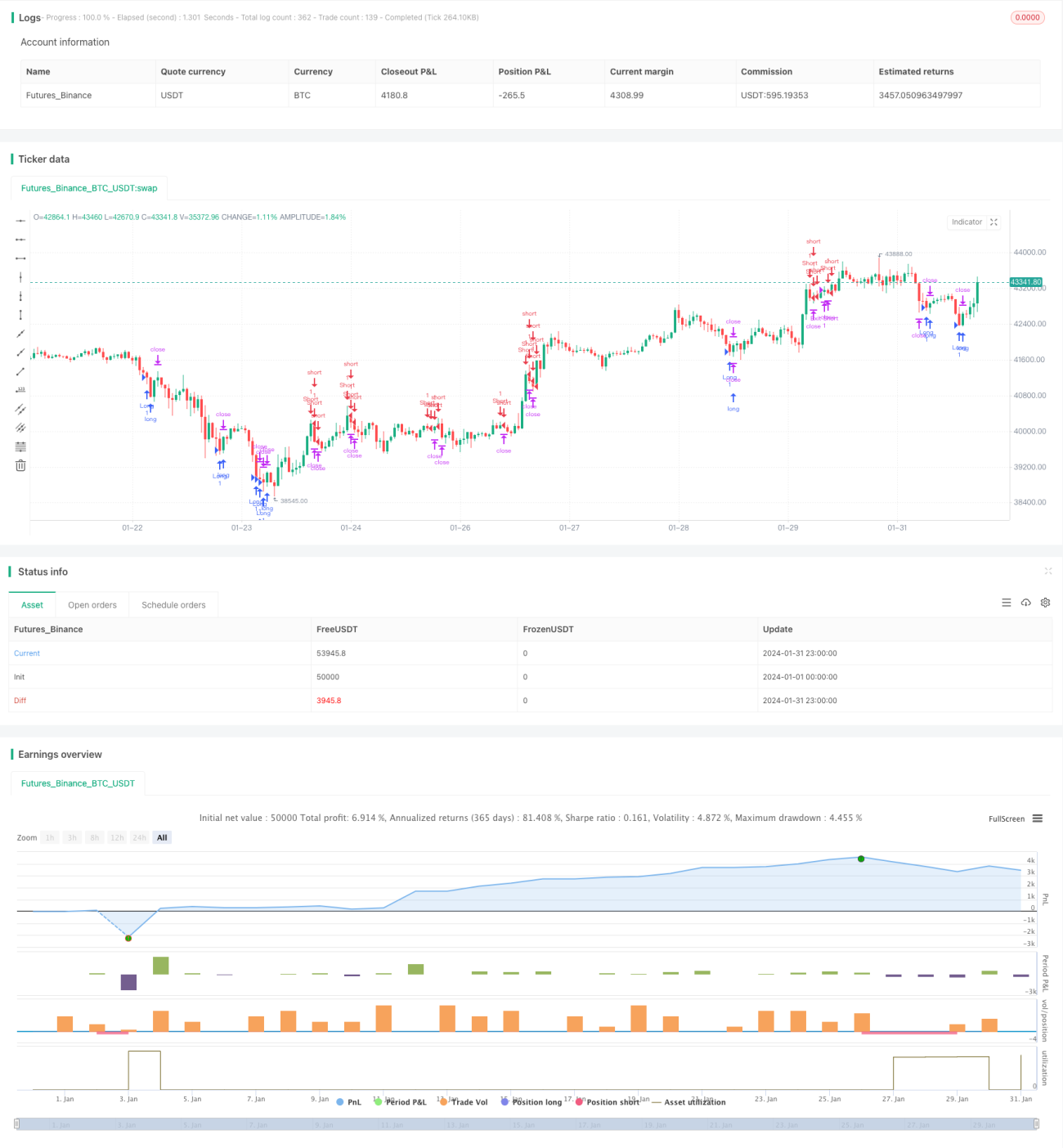

The strategy uses 20-period, 2 standard deviation Bollinger Bands to identify if price touches or breaks through the upper or lower band. Touching the lower band indicates a possible oversold condition while breaking through the upper band overbought. In addition, a Stochastic oscillator with K line cycle of 14 and D value smoothing cycle of 3 determines overbought and oversold. When close price is below the Bollinger lower band and Stochastic K value is below 20, it signals oversold for long entry. When close goes above the Bollinger upper band and Stochastic K is above 80, it signals overbought for short entry.

After entry, the strategy uses Average True Range indicator for trailing stop loss. The stop loss point is set at 1.5 times of ATR, which could define stop loss range based on market volatility, avoiding too tight or too loose stop loss.

Advantage Analysis

The strategy has the following advantages:

-

Combining Bollinger Bands and Stochastic oscillator to determine overbought/oversold provides higher accuracy in capturing trading opportunities.

-

Dynamic adjustment of stop loss points based on market volatility results in reasonable stop distance.

-

Trailing stop loss mechanism prevents stop distance from being too close to avoid premature stop out.

-

Simple and clear strategy rules make it easy to understand and execute.

Risk Analysis

There are some risks in this strategy:

-

Bollinger Bands upper/lower band cannot guarantee price reversal, there could be breakout continuation.

-

Improper parameter tuning of Stochastic may generate inaccurate signals.

-

Stop trailing might lead to too wide stop loss exceeding reasonable market fluctuation.

-

A dynamic trailing stop may work better with micro-adjustments of stop distance based on market volatility.

Optimization Directions

The strategy can be further optimized in the following aspects:

-

Test impact of different Bollinger parameters to find optimal parameter combination.

-

Test different Stochastic parameters to improve indicator performance.

-

Dynamically adjust stop distance based on stop loss trigger times and profitability.

-

Add other indicators to filter entry signals and improve success rate.

-

Add stop loss re-entry mechanism to fully capture market trends.

Conclusion

The strategy identifies overbought/oversold based on Bollinger Bands, with confirmation from the Stochastic indicator. It has the advantage of clear rules and flexible trailing stop loss. It also has risks like inaccurate judgement criteria and improper stop distance configuration. Performance can be further improved through parameter optimization, additional signal filtering, dynamic adjustment of stop loss etc.

- 1