RSI and MA Crossover Trend Tracking Strategy

Overview

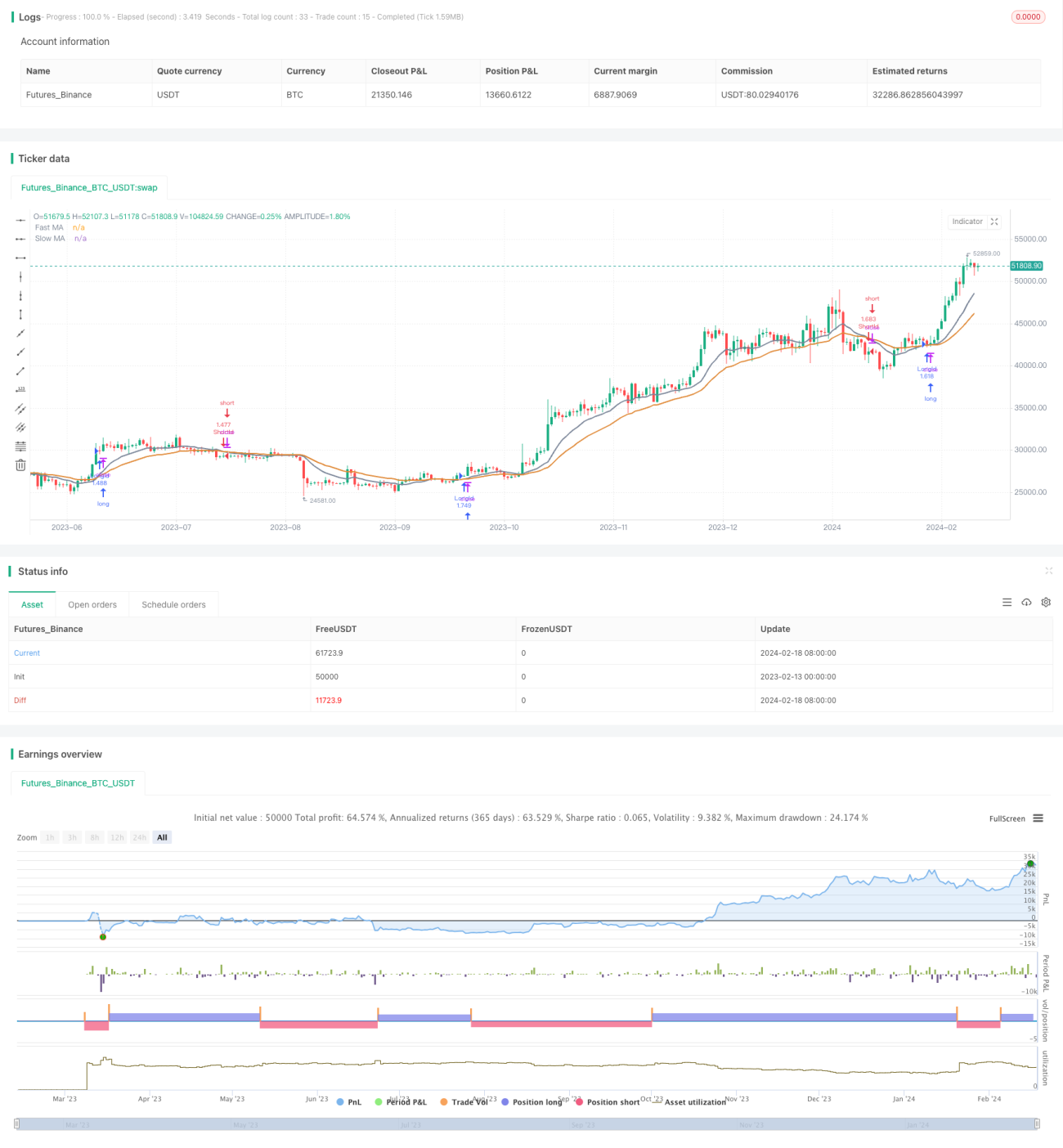

This strategy determines market trends and entry signals by the crossover of the RSI indicator and two moving averages (MAs) of different periods. It only goes long when RSI is above its 26-period MA and goes short when RSI is below to control risks.

Strategy Logic

The strategy employs two MAs of 12- and 26-period. When the 12-period fast MA crosses above the 26-period slow MA, it signals an upward trend, and vice versa. The strategy goes long on golden crossover and goes short on death crossover of the two MAs.

The RSI indicator is also used to determine overbought/oversold zones. Only when RSI is higher than its 26-period MA will the strategy open long positions on golden crossover. And only when RSI is lower will it open short positions on death crossover. This avoids forced entries against overbought/oversold situations and hence controls risks.

Advantage Analysis

By combining MAs and RSI for trend and timing analysis, this strategy can effectively track trends. The RSI filter reduces trade frequencies and avoids whipsaws in ranging markets. Not using a stop loss allows full trend following for higher returns.

Risk Analysis

Without a stop loss, losses may amplify on wrong signals. Large gap moves may also lead to heavy losses. Also, improperly set RSI filters may cause missing good entry signals.

Consider using a stop loss to control maximum losses. Fine tune RSI parameters for better filters. For volatile markets, use slower MAs to judge the trend.

Optimization Directions

The strategy can be improved in the following aspects:

-

Test MA combos of different periods to find parameters best fitting current market conditions.

-

Optimize RSI periods and filter logics for better entry timing.

-

Add other indicators like volume for better system stability.

-

Optimize stop loss strategies to balance trend following and risk control, e.g., trailing stop, percentage stop, dynamic stop etc.

Conclusion

The strategy is relatively simple and straightforward, using MA crossovers to determine trends and RSI to avoid forced entries, thus tracking trends for good returns. Further improvements can be made through parameter tuning and adding other filters to suit complex market environments.

/*backtest

start: 2023-02-13 00:00:00

end: 2024-02-19 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title = "EMA Cross Strategy", shorttitle = "EMA Cross",calc_on_order_fills=true,calc_on_every_tick =true, initial_capital=21000,commission_value=.25,overlay = true,default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

StartYear = input(2018, "Backtest Start Year")- 1