All About Momentum Trading Strategy with Stop Loss for Gold

Overview

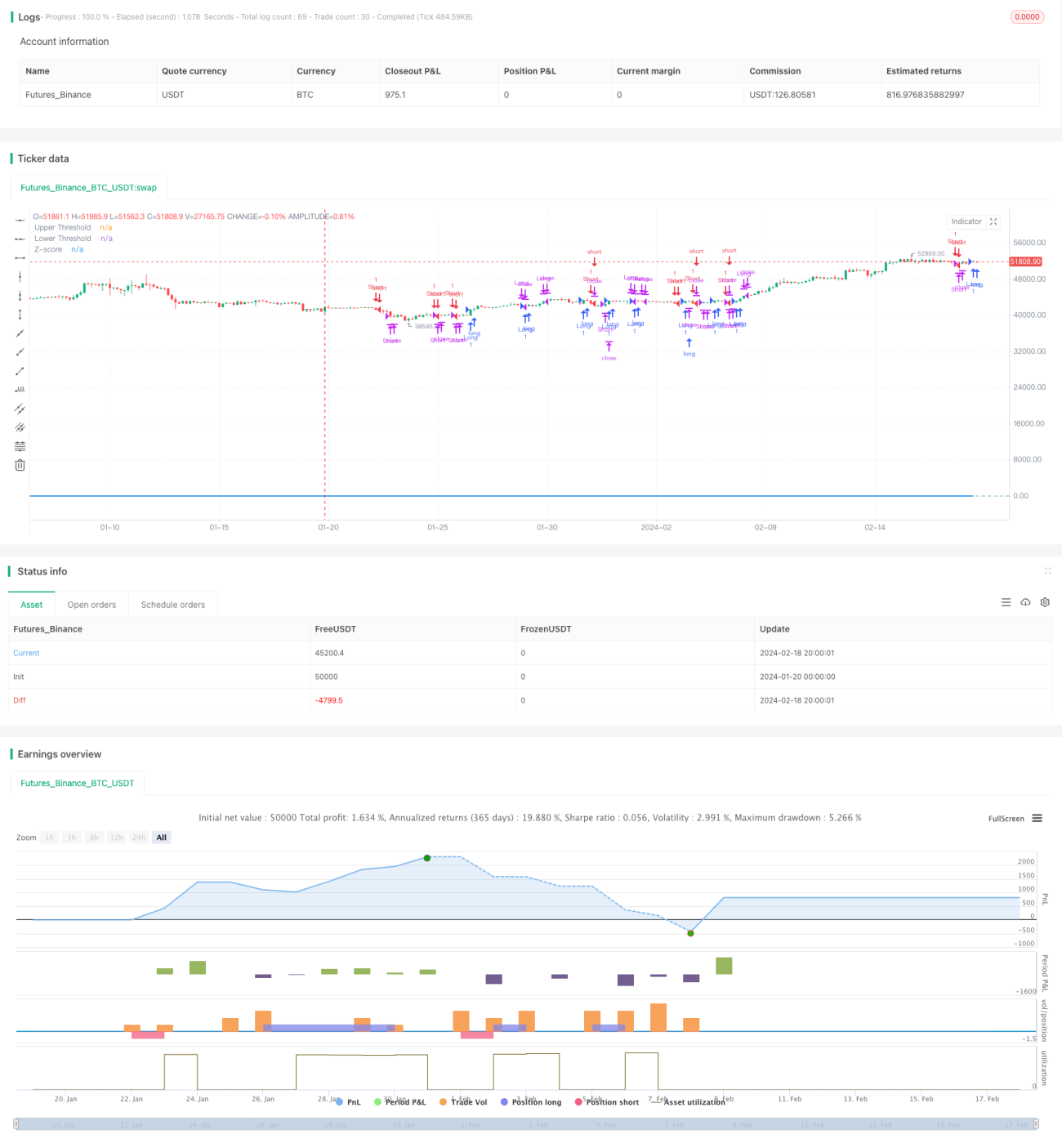

This strategy calculates the deviation of gold price from its 21-day exponential moving average to determine overbought and oversold situations in the market. It adopts a momentum trading approach with stop loss mechanism to control risk when deviation reaches certain thresholds in terms of standard deviation.

Strategy Logic

- Calculate 21-day EMA as the baseline

- Compute deviation of price from EMA

- Standardize deviation into Z-Score

- Go long when Z-Score crosses over 0.5; Go short when Z-Score crosses below -0.5

- Close position when Z-Score falls back to 0.5/-0.5 threshold

- Set stop loss when Z-Score goes over 3 or below -3

Advantage Analysis

The advantages of this strategy are:

- EMA as dynamic support/resistance to capture trends

- Stddev and Z-Score effectively gauge overbought/oversold levels, reducing false signals

- Exponential EMA puts more weight on recent prices, making it more sensitive

- Z-Score standardizes deviation for unified判断 rules

- Stop loss mechanism controls risk and limits losses

Risk Analysis

Some risks to consider:

- EMA can generate wrong signals when price gaps or breaks out

- Stddev/Z-Score thresholds need proper tuning for best performance

- Improper stop loss setting could lead to unnecessary losses

- Black swan events may trigger stop loss and miss trend opportunity

Solutions:

- Optimize EMA parameter to identify major trends

- Backtest to find optimal Stddev/Z-Score thresholds

- Test stop loss rationality with trailing stops

- Reassess market post-event, adjust strategy accordingly

Optimization Directions

Some ways to improve the strategy:

- Use volatility indictors like ATR instead of simple Stddev to gauge risk appetite

- Test different types of moving averages for better baseline

- Optimize EMA parameter to find best period

- Optimize Z-Score thresholds for improved performance

- Add volatility-based stops for more intelligent risk control

Conclusion

Overall this is a solid trend following strategy. It uses EMA to define trend direction and standardized deviation to clearly identify overbought/oversold levels for trade signals. Reasonable stop loss controls risk while letting profits run. Further parameter tuning and adding conditions can make this strategy more robust for practical application.

- 1