Multi-indicator Quant Trading Strategy

Overview

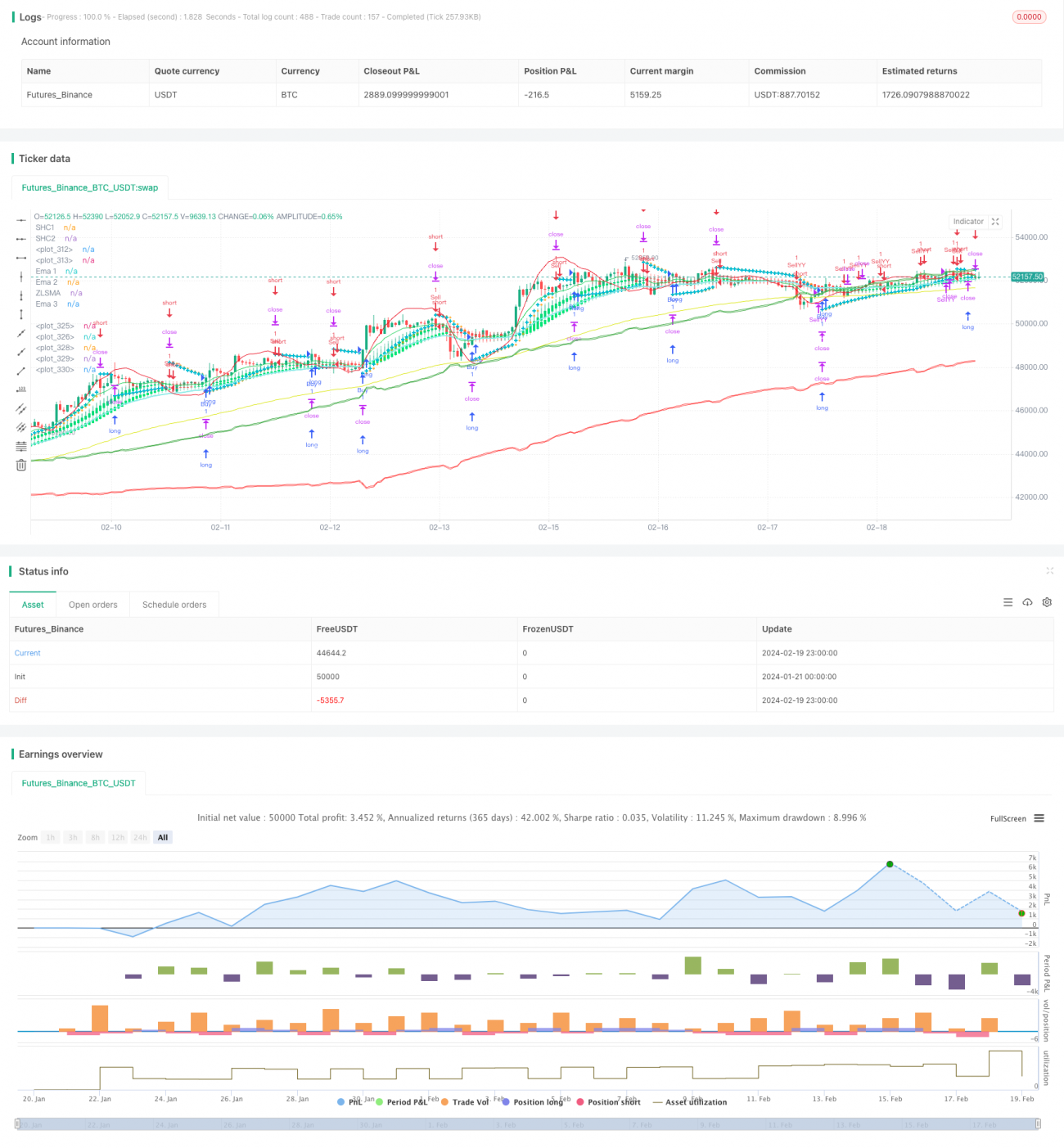

This strategy integrates various technical indicators, including Parabolic SAR, Chandelier Exit, Zero Lag SMA, EMA, and Heikin Ashi, to identify potential buy and sell signals on the chart.

Strategy Logic

Key Indicators

- Parabolic SAR: Used to determine stop loss points and potential entry points

- Chandelier Exit Strategy: Used to determine trend direction

- Zero Lag SMA: Provides low-lag moving average

- EMA: Tracks trends and price fluctuations

- Smoothed Heikin Ashi: Generates smoothed Heikin Ashi candles

Trading Signals

- Long when Parabolic SAR shows uptrend and price is above 99 EMA; Short when downtrend and price is below 99 EMA

- Combine with Chandelier Exit signals to further confirm trend

- Smoothed Heikin Ashi helps avoid false breaks

Risk Management

- Set stop loss and take profit

- Consider reset conditions to flexibly adjust positions

Strengths Analysis

The biggest strength is the comprehensive combination of indicators for effective trend identification. Parabolic SAR detects potential reversals; Chandelier Exit judges the major trend; Moving averages filter false signals. Cross validation improves accuracy.

In addition, stop loss and take profit controls risks. Smoothed lines avoid short-term noise. The strategy is stable.

Risk Analysis

Conflicting signals can cause difficulties. Improper parameter settings may also negatively impact trading.

There are inherent risks in technical trading that can cause losses. Cautious operation is a must. Blind following should be avoided.

Optimization Directions

- Test and optimize parameters to find the best combination

- Introduce machine learning models for higher accuracy

- Incorporate sentiment indicators and news to assess market conditions and dynamically manage positions

- Improve logics of reset conditions for more flexible signal detection

Conclusion

This strategy integrates indicators for signal identification. Strengths include high accuracy, stability and sound risk control. Overall a worthwhile trading scheme. Further improvements can be made through parameter tuning, model training and sentiment indicator integration.

- 1