Reversal Trading Strategy with Bollinger Bands, RSI, ADX and ATR

Overview

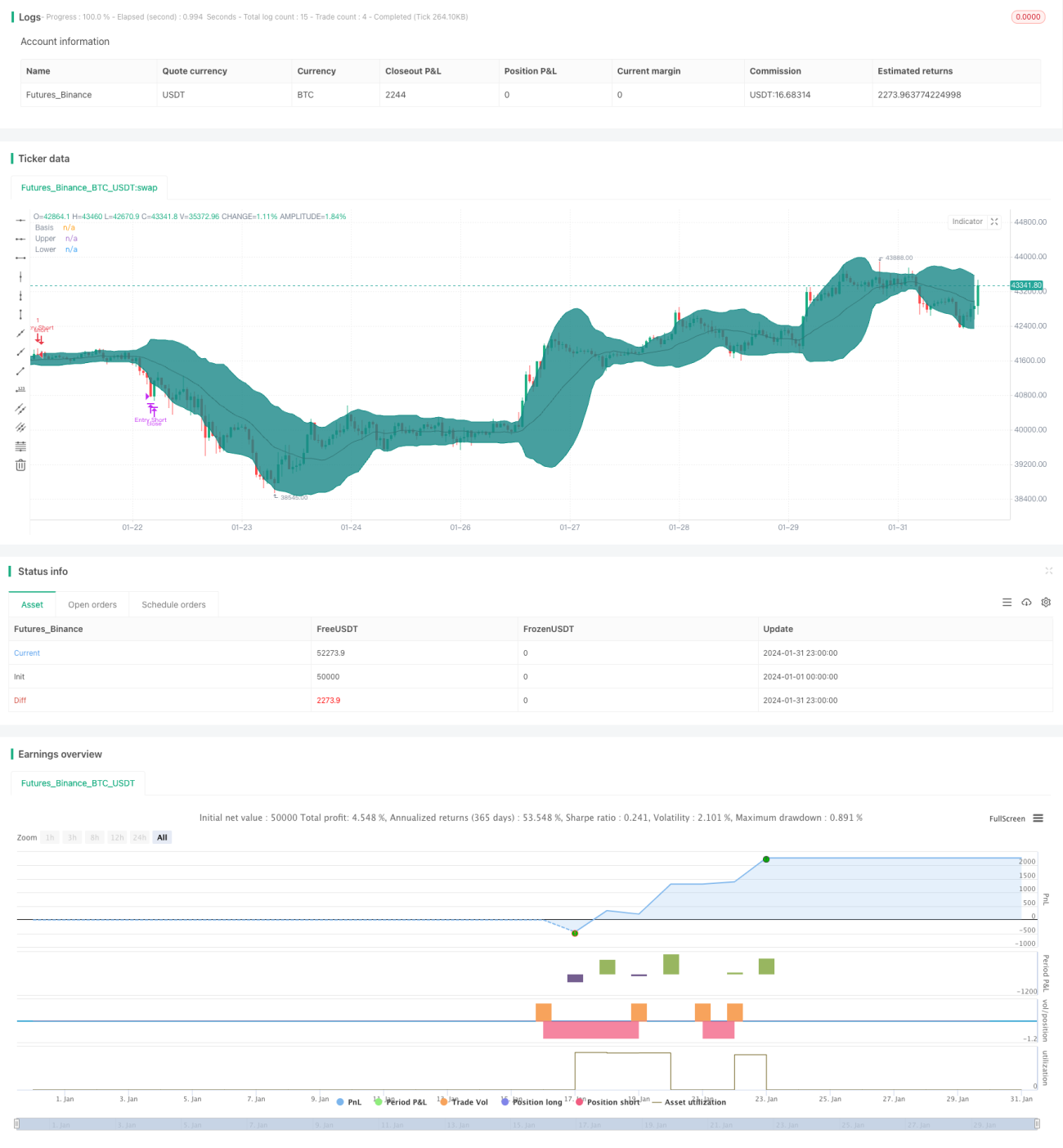

This strategy integrates multiple technical indicators. It looks for high probability reversal trading opportunities when the Bollinger Bands indicator generates price reversal signals, combined with judgments on market structure from RSI, ADX and ATR indicators.

Strategy Logic

-

Use 20-period Bollinger Bands and wait for reversal candlestick patterns when price reaches band highs or lows.

-

RSI indicator judges if the market is in ranging mode, with RSI above 60 indicating bullish range and below 40 bearish range.

-

ADX below 20 suggests ranging market, while above 20 suggests trending conditions.

-

ATR sets stop loss and trailing stop loss.

-

Additional filter from EMA lines.

Advantage Analysis

-

Multiple indicators combined provide high-probability trading signals.

-

Configurable parameters adapt to different market environments.

-

Strict stop loss rules effectively control risks.

Risk Analysis

-

Improper parameter settings may cause over-frequent trading.

-

Probability of reversal failure still exists.

-

Trailing stop loss may fail in certain markets.

Optimization Directions

-

Test more indicator combinations to find better parameter configurations.

-

Timely identify continuation reversal opportunities after initial failure.

-

Test different stop loss methods to make stops more intelligent.

Conclusion

This strategy uses Bollinger Bands for core trading signals, and multiple auxiliary indicators form a high-probability filtering system. The stop loss rules are also quite complete. Further performance improvement can be achieved through parameter tuning and indicator optimization. Overall, this strategy forms a reliable reversal trading system.

- 1