Recursive Moving Trend Average Combined with 123 Reversal Pattern Strategy

Overview

This strategy combines the Recursive Moving Trend Average and the 123 Reversal Pattern into a composite signal to improve the stability and profitability.

Principle

123 Reversal Pattern

This part is inspired by the book "How I Tripled My Money in the Futures Market" by Ulf Jensen. It buys when the close price rises for two consecutive days and the 9-day STO SLOWK is below 50. It sells when the close price falls for two consecutive days and the 9-day STO FASTK is above 50.

Recursive Moving Trend Average

This technique is called "recursive polynomial fitting". It uses the prices of the past few days and today's price to predict tomorrow's price. It goes short when the predicted price is higher than yesterday's actual price, and goes long otherwise.

Advantages

The combined strategy exploits the strengths of both strategies to avoid the limitations of a single one. The 123 Reversal Pattern can catch major trends when price reversal happens. The Recursive Moving Trend Average can judge the price movement direction more accurately. Together they form stronger composite signals.

Risks and Solutions

- The 123 Reversal Pattern may generate false signals due to short-term price fluctuations. Fine tuning the parameters helps filter out noise.

- The Recursive Moving Trend Average may respond slowly to sudden events. Considering other indicators for local trends is helpful.

- The two strategies may give inconsistent signals sometimes. One solution is to open positions only when double signals emerge, or follow just one signal based on market conditions.

Directions for Enhancement

- Test different combination of period parameters to find the optimal pair.

- Introduce auto stop-loss mechanisms.

- Adjust parameters based on different products and market environments.

- Consider combining with other strategies or indicators to form more robust systems.

Conclusion

This strategy combines two different types of strategies and generates composite signals to improve stability. It exploits both their advantages to catch price reversal points and judge future price trends. Further optimizations may lead to even better performance.

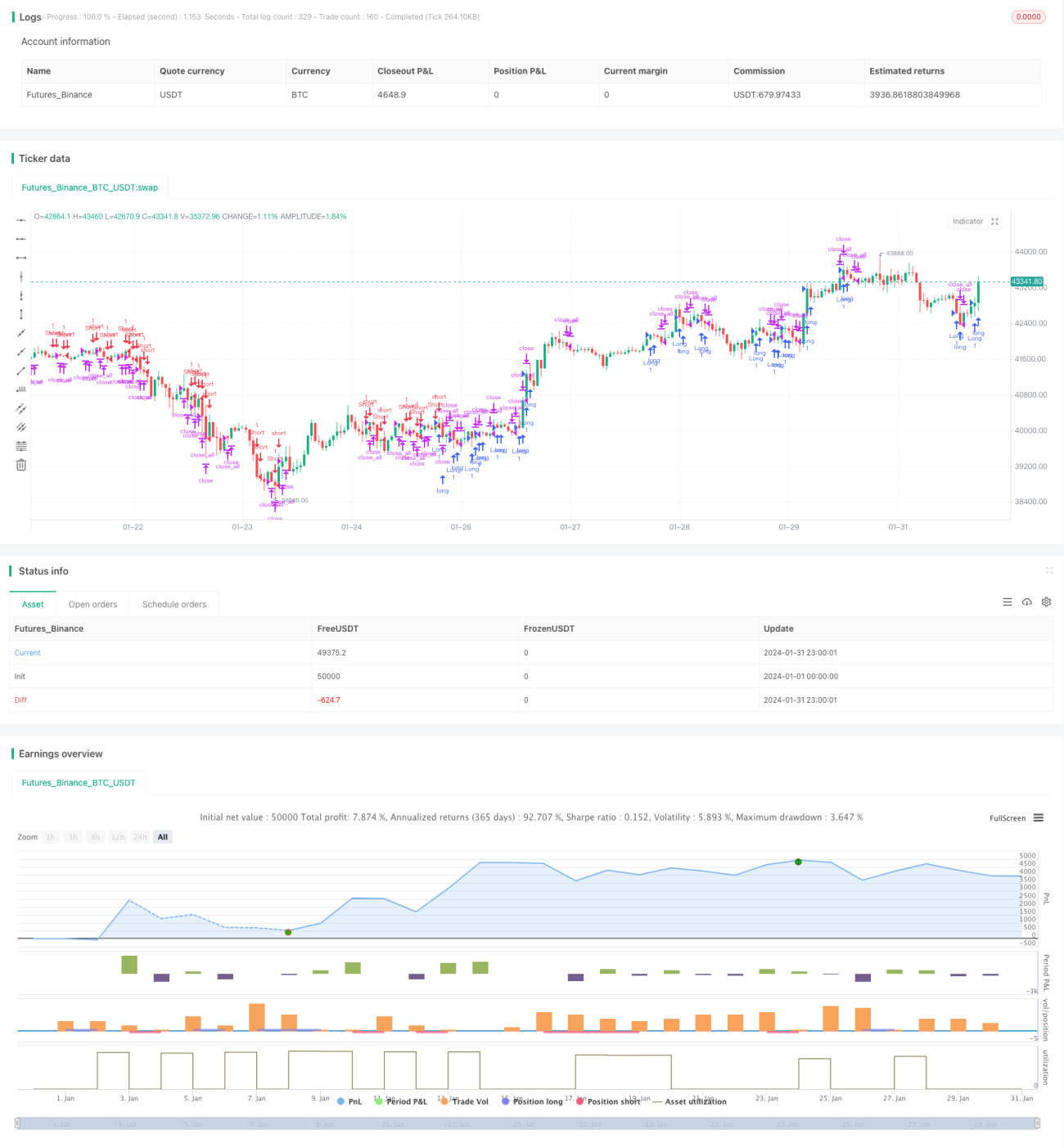

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 01/06/2021

// This is combo strategies for get a cumulative signal. - 1