Adaptive Moving Stop Line Trading Strategy

Overview

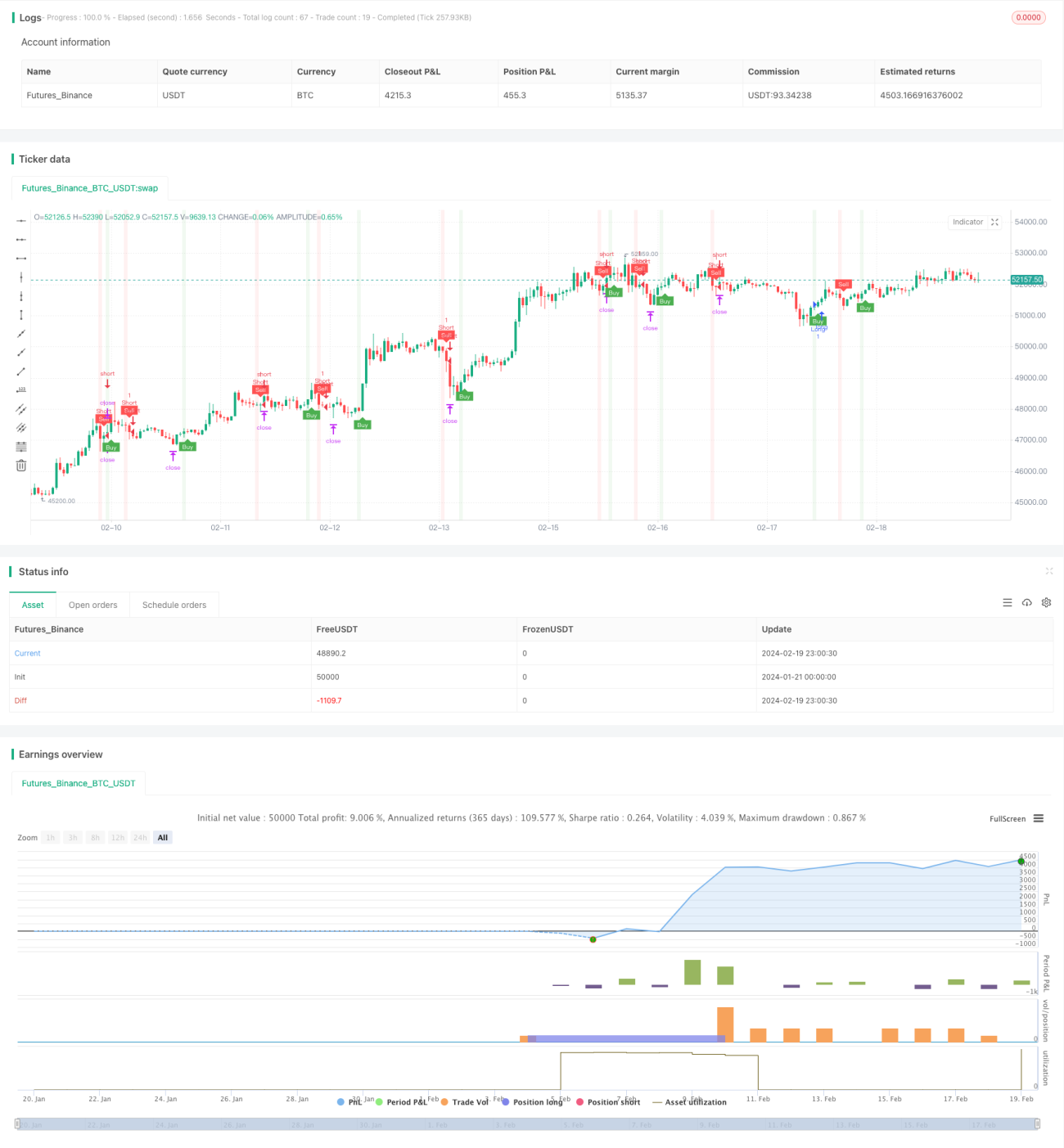

The core idea of this strategy is to use the T3 moving average and ATR adaptive trailing stop to capture entry and exit points along the trend. It belongs to the trend following strategies. Trading signals are generated when price breaks through the T3 line, and stop loss and take profit levels are set using the ATR value at the breakout point to achieve automatic stop loss and take profit.

Strategy Principle

The strategy consists of the T3 indicator, ATR indicator and ATR trailing stop mechanism.

The T3 moving average is a smoothed moving average that can reduce the lag of the curve and make it respond faster to price changes. A buy signal is generated when the price breaks through the moving average from below. A sell signal is generated when the price breaks through from above.

The ATR indicator is used to calculate the degree of market volatility and set stop loss levels. The larger the ATR value, the greater the market volatility, and a wider stop loss should be set. The smaller the ATR value, the smaller the market volatility, and a narrower stop loss can be set.

The ATR trailing stop mechanism adjusts the stop loss line position based on ATR values in real time, so that the stop loss line can follow the price movement and remain within a reasonable range. This prevents the stop loss from being too close and knocked out easily, and also prevents the stop loss from being too wide to effectively control risks.

By utilizing the T3 to determine direction, ATR to calculate volatility and the ATR trailing stop mechanism, this strategy achieves relatively efficient trend catching and risk control.

Advantages

The advantages of this strategy include:

-

The application of the T3 line improves the accuracy of catching trends.

-

The ATR indicator dynamically calculates market volatility, making stop loss and take profit levels more reasonable.

-

The ATR trailing stop mechanism enables the stop loss line to follow the price movement in real time for effective risk control.

-

Integrates indicators and stop loss mechanisms to achieve automated trend tracking trading.

-

Can connect to external trading platforms via webhook for automated order execution.

Risks and Solutions

There are also some risks with this strategy:

-

Improper T3 parameter settings may miss better trend opportunities. Different cycle parameters can be tested to find the optimal values.

-

Inaccurate ATR value calculation may lead to stop loss distance being too large or too small to effectively control risk. The ATR cycle parameter can be adjusted combined with market volatility characteristics.

-

In violent fluctuations, the stop loss line may be broken resulting in excessive losses. A reasonable total loss line can be set to avoid excessive losses per trade.

-

Frequent stop loss triggering may occur in whipsaw markets. Appropriately widening the ATR trailing stop distance can help.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Optimize the T3 parameter to find the most suitable smoothing cycle.

-

Test different ATR cycle parameters to calculate the ATR value that best reflects market volatility.

-

Optimize the flexible range of the ATR trailing stop distance to prevent over-sensitive stops.

-

Add appropriate filters to avoid frequent trading in whipsaw markets.

-

Incorporate trend judging indicators to improve directional profitability accuracy.

-

Use machine learning methods to automatically optimize parameters.

Conclusion

This strategy integrates the use of the T3 line to determine trend direction, ATR indicator to calculate stops/targets and ATR trailing stop mechanism to adjust stop distance. It achieves automated trend tracking and efficient risk control. It is a reliable trend following strategy. In practical applications, continuous testing and optimization is still needed to find the most suitable parameter combinations for current market conditions, thereby obtaining better strategy results.

- 1