Bollinger Bands Consolidation Strategy

Overview

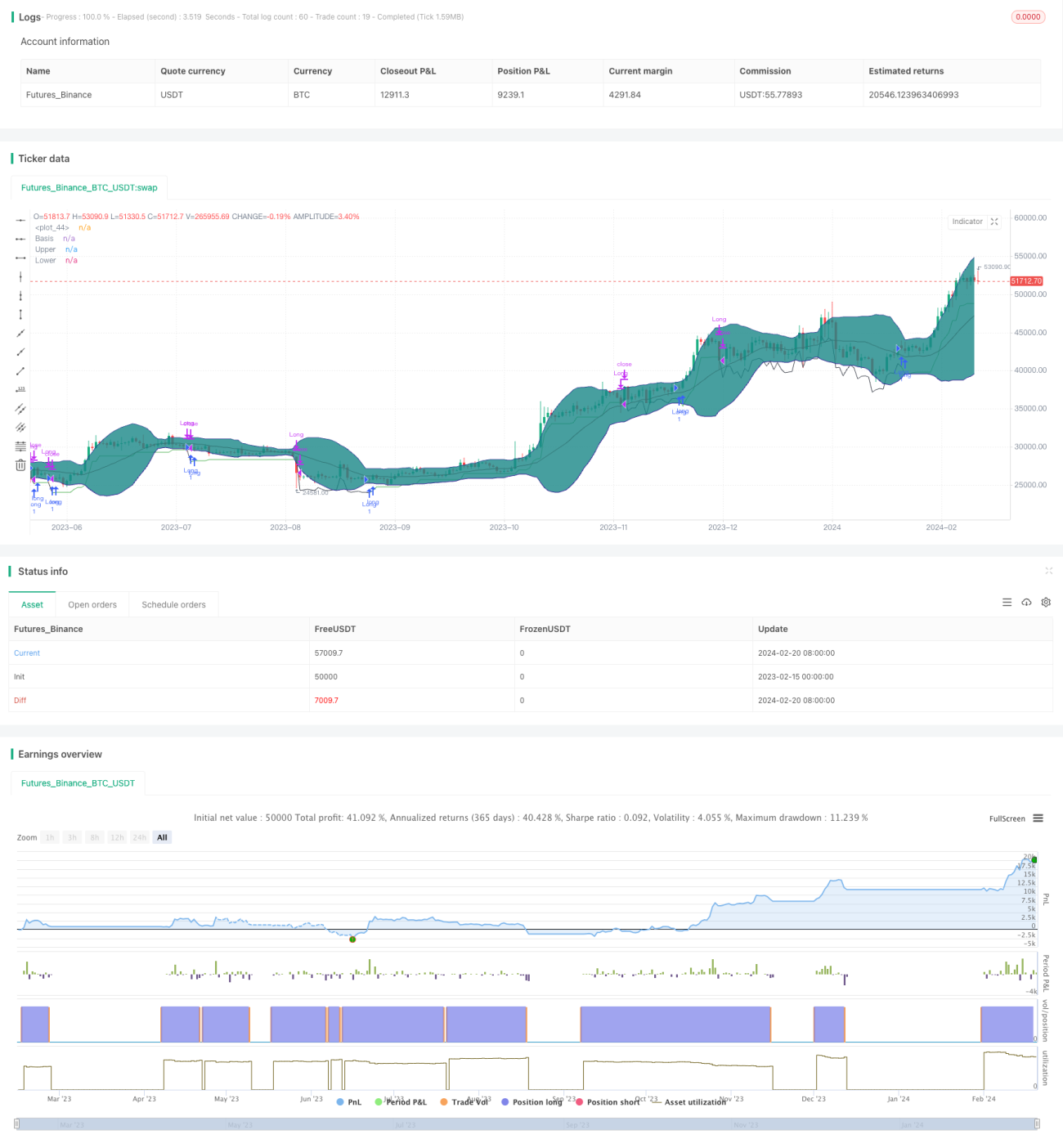

The Bollinger Bands consolidation strategy is a breakthrough strategy that identifies low volatility consolidation phases using Bollinger Bands. When the market enters a ranging period, the Bollinger Bands will converge, signaling an opportunity to enter the market. We also incorporate the Average True Range indicator to confirm the decrease in volatility.

Strategy Logic

The strategy relies primarily on Bollinger Bands to detect when prices enter a low volatility consolidation phase. The middle band of Bollinger Bands is a moving average of closing prices. The upper and lower bands are offset by two standard deviations above and below the middle band. When volatility decreases, the distance between the upper and lower bands narrows noticeably. We first check if the current ATR value is less than the standard deviation between the Bollinger Bands to preliminarily confirm the convergence. This signals prices have just entered into consolidation.

To further prove the decrease in volatility, we check if the moving average of ATR values has a downward trend. The decrease in average ATR also corroborates from the side that volatility is declining. When both conditions are met simultaneously, we determine Bollinger Bands have shown significant convergence, which is an excellent buying opportunity.

After buying in, we enable a moving stop loss strategy with a stop loss distance of twice the ATR value. This effectively controls losses.

Advantage Analysis

The biggest advantage of this strategy is that it can accurately determine when the market enters a low volatility consolidation phase and identify the best buying opportunity. Compared to other long-term strategies, the Bollinger Band consolidation strategy has a higher probability of profit.

In addition, the strategy also uses a moving stop loss to actively control risks. This maximizes loss reduction even when the market sentiment is unfavorable. Many long-term strategies lack this.

Risk Analysis

The main risk of the strategy is that the Bollinger Bands indicator cannot accurately determine changes in price volatility 100% of the time. When Bollinger Bands misjudge that volatility has decreased, our entry timing may be unfavorable. At this point, the moving stop loss plays an important role and can exit the trade as early as possible.

In addition, the setting of various parameters in the strategy will also affect the results. We need to optimize the parameters through extensive backtesting to make the strategy more robust.

Optimization Directions

We can consider adding other indicators to confirm the turning signs on trend indicators when Bollinger Bands converge. For example, when Bollinger Bands converge, we also require that the MACD difference has turned from positive to negative, or RSI has pulled back from the overbought zone. This can further improve the accuracy of the buying signals.

Another direction is to test the impact of different parameter settings on the results, such as the periods of Bollinger Bands, ATR and the multiplier of the moving stop loss. We need to use stepwise optimization to find the optimal parameter combination.

Conclusion

The Bollinger Bands consolidation strategy utilizes Bollinger Bands to determine the timing of decreased price volatility and uses a moving stop loss to effectively control risks. It is a relatively stable long-term breakout strategy. We still need to further optimize parameters and incorporate other indicators to enhance the robustness of the strategy.

- 1